Nyheter

Mexico’s post-election potential and investment opportunities

Given Mexico’s vast potential and President-elect Claudia Sheinbaum’s track record of progress during her time as mayor of Mexico City, Franklin Templeton’s Dina Ting thinks that investors should be monitoring opportunities to enter this compelling market.

Just how well—or not so well—Mexico’s President-elect Claudia Sheinbaum may be able to tackle the country’s prevailing challenges is still up for debate. Sheinbaum’s commanding margin of victory in the June election discouraged some investors amid fears that her ruling Morena party could potentially push through constitutional reforms that may adversely impact Mexico’s business environment.

Since the outcome of the US presidential election will remain undecided for a month after Sheinbaum takes office in October, we expect Mexico’s equity markets to experience more short-term market volatility. But given Mexico’s ongoing potential to capitalize on nearshoring investments and Sheinbaum’s track record of progress during her time as mayor of Mexico City (beginning in 2018), we think investors should be monitoring opportunities to enter this compelling market. We believe a continuation of US macro drivers are still poised to drive Mexican exports. Although US appetite for Chinese imports was still high even as recently as 2022, the drop-off in trade with China since then has benefited Mexico, which recently eclipsed both China and Canada to become the biggest US trade partner.

Mexico’s first female president

A protégé of outgoing President López Obrador (or AMLO as he is known), Sheinbaum has pledged to continue along the political course of her predecessor. But as a climate scientist with a Ph.D. in environmental engineering, she appears to us to be more attuned to pressing issues, such as Mexico’s water woes and efforts toward the energy transition. She has demonstrated deep, technical expertise and perspective on vital issues—“not simply as stewardship of natural resources, but also as an issue interconnected with education, social justice, health care, housing and infrastructure,” according to the think tank Atlantic Council.

There is hope that the public-private partnerships that Sheinbaum advanced during her time as Mexico City’s mayor could be a model that she adopts and adapts in her new administration to increase the number of strategic projects. These may include opening natural gas production and transportation to private participants, boosting infrastructure and more renewable energy projects that are critical for Mexico to take advantage of nearshoring-related investment opportunities.

Since renewables like solar and wind currently make up only about 12% of the electricity mix in Mexico (significantly lagging the 16% share for the United States), there is great potential for the country’s clean energy buildout. Sheinbaum has pledged to change course from AMLO in her approach to speeding the promotion of renewable energies with a US$13.6 billion investment plan through 2030 that includes pioneering development of smart grids and other green technologies. Experts have praised Sheinbaum’s methodical approach to governance, for example, bringing stability and predictability to regulatory frameworks with her technical background and reliance on seasoned advisors.

Among some of the moderate-to-high risks for Mexico is public security and crime. Here again, Sheinbaum’s approach in working with US counterparts during her tenure in Mexico City has been applauded. Her cabinet picks for key positions thus far present an even gender distribution and draw from academia and her mayoral administration—in a bid to repeat the successes in crime-fighting she achieved during her years as mayor. These include veteran politicians Omar Garcia Harfuch for Security Minister, Marcelo Ebrard for Secretary of Economy and Alicia Barcena for Secretary of Foreign Affairs.

Mexico poised for economic growth

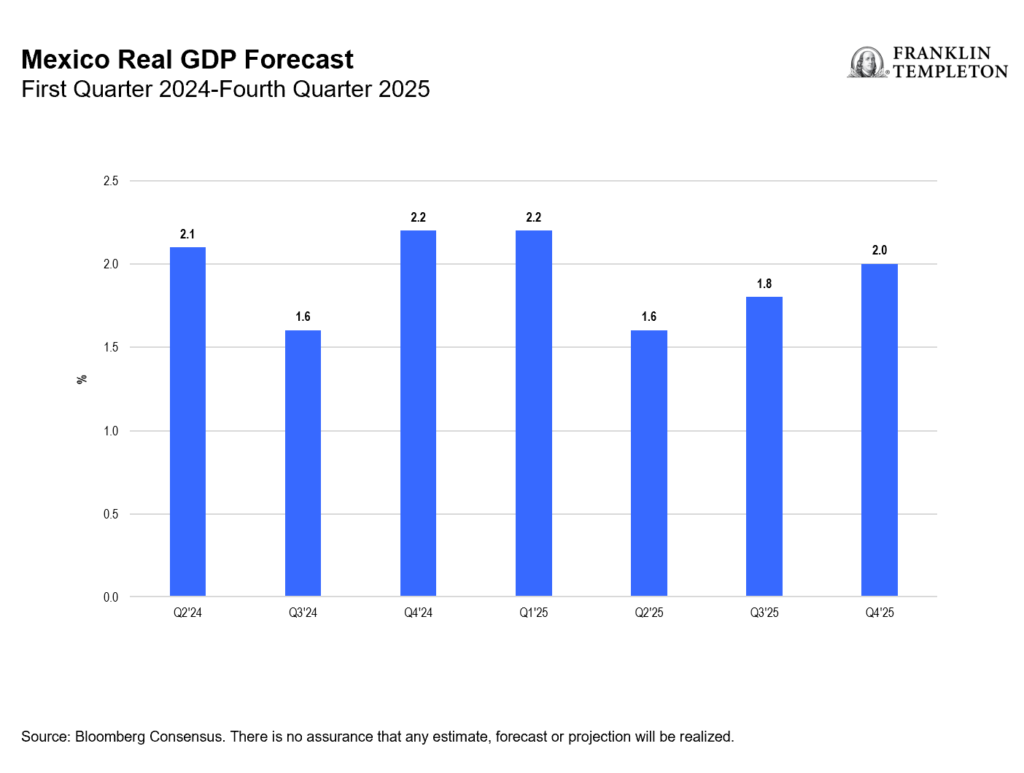

Over the near term, Mexico is expected to achieve a 2% growth rate—higher than its 20-year average.4 Although Mexico’s headline inflation accelerated beyond analyst expectations in June, its strong trend of domestic demand and high consumer confidence should also offer some economic momentum, in our opinion. For example, June auto sales were up 8.3% from a year earlier, according to government data.

It’s also important to recognize that Mexico is the second-highest receiver of remittances—transfers of money from migrants working abroad—in the world, behind only India. For the decade leading up to 2020, the percentage of households in Mexico that received remittances rose to 5.1% from 3.6% in 2010. Last year, remittances to Mexico notched a 7.6% increase, hitting a record US$63 billion, due to a strong US labor market.

Exhibit 1: Mexico Consumer Confidence

Exhibit 2: Mexico Real Gross Domestic Product (GDP) Forecast

Investors seeking exposure to Mexico’s market through broad emerging market indexes, like the MSCI Emerging Market (EM) Index, gain less than a 3% weighting to Mexico. And while China’s dominant share of the benchmark is lower now than in recent years, it still presents a 25% weighting, which may be more than investors want. In our opinion, single-country exchange-traded funds offer a compelling way for investors to layer targeted access to a country’s large- and mid-sized companies at a low cost.

As of the end of June, Mexico’s main benchmark stock index, the IPC, held a 33% weighting in the consumer staples sector. Materials and financial sector stocks make up the next biggest weighting at about 19% each.

As Mexico continues to play a larger role in global supply chains, investors should note corporate nearshoring progress as gauged by the country’s foreign direct investment (FDI) trends. At the end of 2023, Mexico ranked ninth among the world’s largest recipients of FDI, receiving investments of US$36 billion—about 2% more than in the prior year. Longer term, we believe nearshoring efforts, to diversify and improve the security of supply chains, remain a key tailwind for Mexico’s economy and markets.

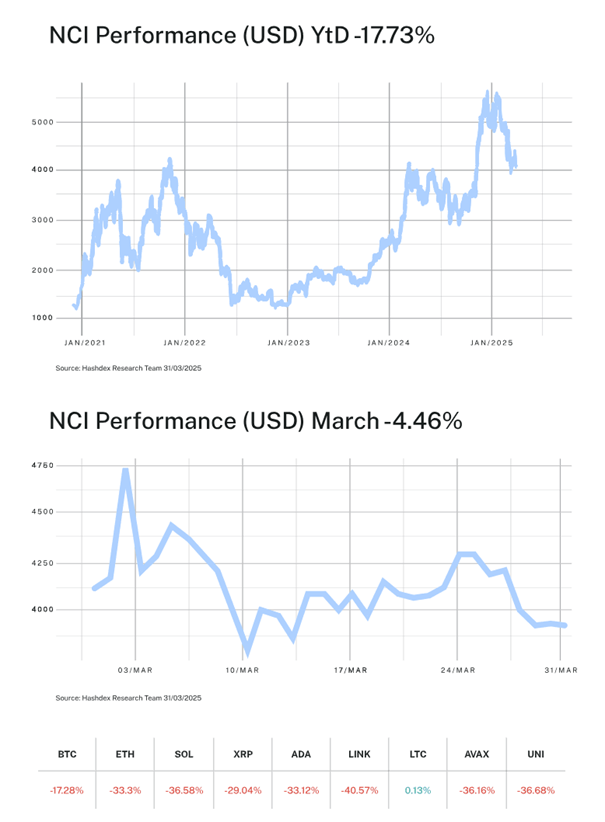

The impact of US tariffs continues to dominate market sentiment and risk assets, including crypto, struggled with this uncertainty throughout the month. The Nasdaq Crypto Index™ (NCI™) fell 4.46% in March as the S&P 500 and Nasdaq 100 dropped 5.63% and 7.61%, respectively.

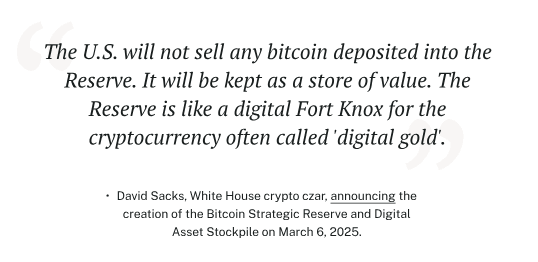

Despite the macro uncertainty from Washington, US policymakers are continuing to embrace crypto in an unprecedented way, including launching a Bitcoin Strategic Reserve, Digital Asset Stockpile, and engaging in expansive work at the regulatory agencies and in Congress.

Our team spent the last week of the month in Washington, meeting with regulators to share our experiences and views on what’s most important for crypto investors in the US. In his latest Notes from the CIO, Samir Kerbage shares what he learned from these meetings and how investors should be thinking about the new regulatory regime in the US.

As always, we are greatly appreciative of your trust in us and are here to answer any questions you may have.

-Your Partners at Hashdex

Market Review

March was marked by the tariff dispute triggered by the Trump administration. Back-and-forth fiscal policies, threats, and retaliations dominated the month’s agenda. The uncertain macroeconomic environment put investors into a defensive stance and negatively impacted crypto assets. The Nasdaq Crypto Index™ (NCI™) closed the month down -4.46% after a period of high volatility. Major market indices, the S&P 500 and Nasdaq-100, also recorded steep declines of -5.63% and -7.61%, respectively. These concurrent drawdowns across equities and crypto underscored March’s broad market caution, as trade war uncertainty prompted investors to flee risk assets.

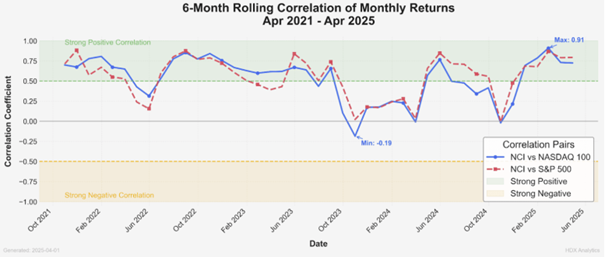

During times of uncertainty, it is common to observe increased correlation among different classes of risk assets. This pattern played out in March: the 6-month rolling correlation of monthly returns between the NCI™ and the Nasdaq-100 surged to roughly 0.91 (see chart below), its highest level since 2021, indicating that crypto assets were moving almost in lockstep with tech stocks. This spike in correlation confirms that crypto was behaving like a high-beta extension of the tech sector—an amplified version of the Nasdaq-100. The lack of clarity in the global landscape leads investors to reduce their risk exposure and seek protection, a movement known in financial markets as “risk-off” allocation.

6-Month Rolling Correlation of Monthly Returns between the Nasdaq Crypto Index and Nasdaq-100 (Apr 2021–Apr 2025).

The chart illustrates how this correlation has been increasing since the American elections in November 2024 and spiked to approximately 0.91 in the most recent period—a multi-year high. This visual evidence reinforces the view that crypto assets have been moving closely in tandem with tech stocks, effectively acting as a high-beta version of the Nasdaq-100 during the March risk-off phase.

Following this trend, risk reduction was evident within the crypto asset class. Among the NCI’s constituents, Bitcoin (BTC) posted a decline of -1.93%, withstanding the downturn far better than other constituents such as Ether (ETH, -17.4%) and Litecoin (LTC, -34.6%). BTC’s relatively mild drop in this sell-off aligns with the idea that it increasingly trades like a high-beta proxy for large-cap tech. It still declined, but less severely, whereas smaller-cap crypto assets behaved more like speculative growth stocks and suffered outsized losses. The only exception to the negative results was Cardano (ADA), which surprised with a positive return of 3.88% despite no significant protocol developments during the month.

Thematic indices also faced a challenging environment. As highlighted in previous letters, smaller capitalization assets tend to suffer more during periods of market stress, mirroring how speculative small-cap stocks are hit hardest in equity sell-offs. The biggest negative highlight was the Digital Culture Index, which dropped -17.45%, followed by the Decentralized Finance (DeFi) and Smart Contract Platform (Web3) indices, which fell -16.73% and -12.07%, respectively. The Vinter Hashdex Risk Parity Momentum Index recorded a negative result of -8.26% but outperformed the three other thematic indices, benefiting from its high allocation in BTC and TRX (which gained 4.68%). The heavy weighting in BTC – the more resilient large-cap crypto – helped cushion this index, underscoring the relevance of the momentum factor in a well-diversified strategy during times of market stress.

The market remains on the lookout for the outcome of the fiscal policy discussions, hoping for a reduction in uncertainties and an end to the tariff war. That would likely mark the moment when investors regain their appetite for risk assets, including crypto assets. The U.S. government has also signaled interest in advancing the crypto agenda, a development that could drive the asset class to a new level of adoption. We remain confident in our positive outlook for the rest of the year and the long term.

Top Stories

US creates Bitcoin Strategic Reserve and Digital Asset Stockpile

The Bitcoin Reserve will be capitalized with BTC owned by the Department of Treasury, which could further increase via new budget-neutral acquisitions. The stockpile will also include assets owned by the Treasury. This marks a major milestone, with the US government starting to integrate major crypto assets and continues the new administration’s work to lead the global crypto economy.

Stablecoins surpass $230 billion in market value

The total stablecoins market capitalization surpassed $230 billion amid institutional demand for dollar-backed digital assets. This showcases one of the most successful applications for crypto technology enhancing traditional financial payments. It could also pave the way for new use cases that require a strong and reliable global payment system.

FDIC eases banks’ ability to engage in crypto activities

The FDIC has rescinded previous guidelines which prevented financial institutions from engaging with crypto activities without prior sign-off. By removing bureaucratic hurdles, banks may more readily over crypto-related services, potentially leading to broader adoption and integration of digital assets into the financial system.

Spotlight on the tariff war

BSE8 ETF ger exponering mot företagsobligationer med förfall under 2028

En vecka för historieböckerna…

VGCF ETF investerar i korta företagsobligationer denominerade i euro

CBUV ETF satsar på Metaverse

Fonder som ger exponering mot försvarsindustrin

WisdomTree lanserar europeisk försvarsfond.

Warren Buffetts råd om vad man ska göra när börsen kraschar

De bästa börshandlade fonderna för tyska utdelningsaktier

Trumps återkomst får europeiska aktier att rusa

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanWisdomTree lanserar europeisk försvarsfond.

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa börshandlade fonderna för tyska utdelningsaktier

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanTrumps återkomst får europeiska aktier att rusa

-

Nyheter5 dagar sedan

Nyheter5 dagar sedanSvenskarna har en ny favorit-ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf lanserar Europa-fokuserad försvars-ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanEn av de mest nedladdade finansapparna i Sverige