Nyheter

How Markets Reacted to New US Credit Rating: What Happened in Crypto Last Week?

Consumer prices in the U.S. rose by 3.2% year-over-year in October, down from 3.7% in September, but still above the Fed’s 2% benchmark. Moody’s Investors Service has cut the US credit outlook from stable to negative. In response, long-term yields soared, which is not only an indication of investor confidence in the U.S. economy but also a proxy used by many to gauge mortgage rates and risk-on assets such as equity and crypto.

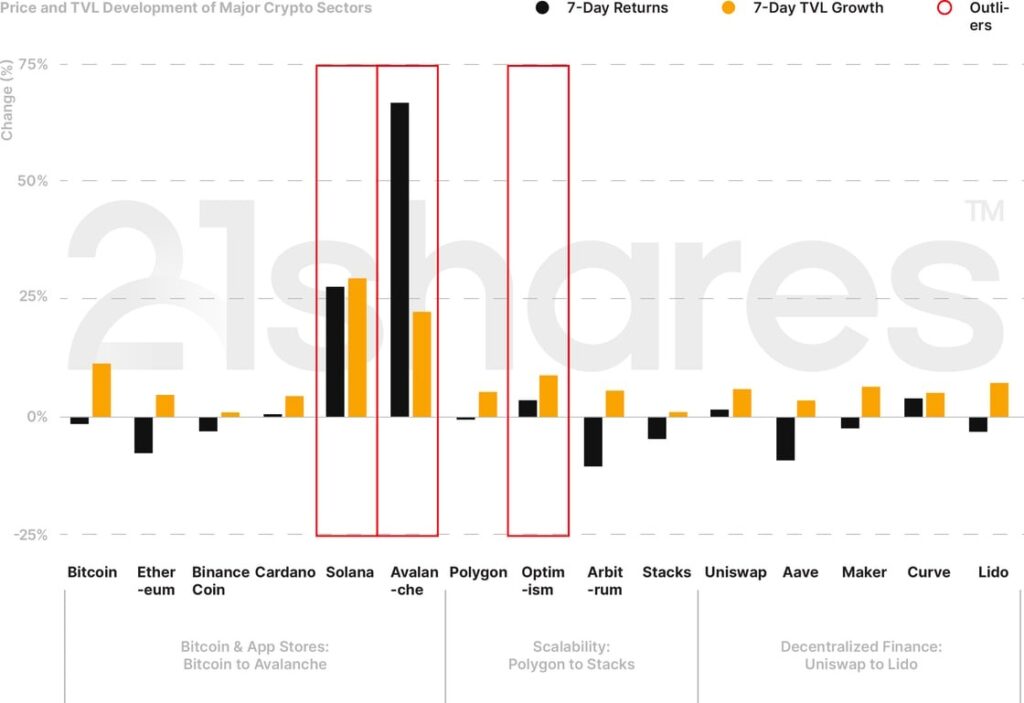

Bitcoin and Ethereum are down by 1.54% and 7.82% over the past week, respectively. Biggest winners of last week were Solana (27.56%), Avalanche (66.56%), and Optimism (3.45%). In this report, we’ll walk you through the top 4 trends to remember in markets this week: what drove Ethereum’s price to break the $2K mark before retracing after a bumpy downhill from August 15? We’ll also break down the new developments on Bitcoin that might bring streaming to the network, Kraken’s new Layer 2 blockchain, and Lido decentralizing its node-infrastructure operations.

Figure 1: Weekly Price and TVL Developments of Cryptoassets in Major Sectors

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of November 16, 2023.

4 Things to Remember in Markets this Week:

Ethereum Rejoins the Race

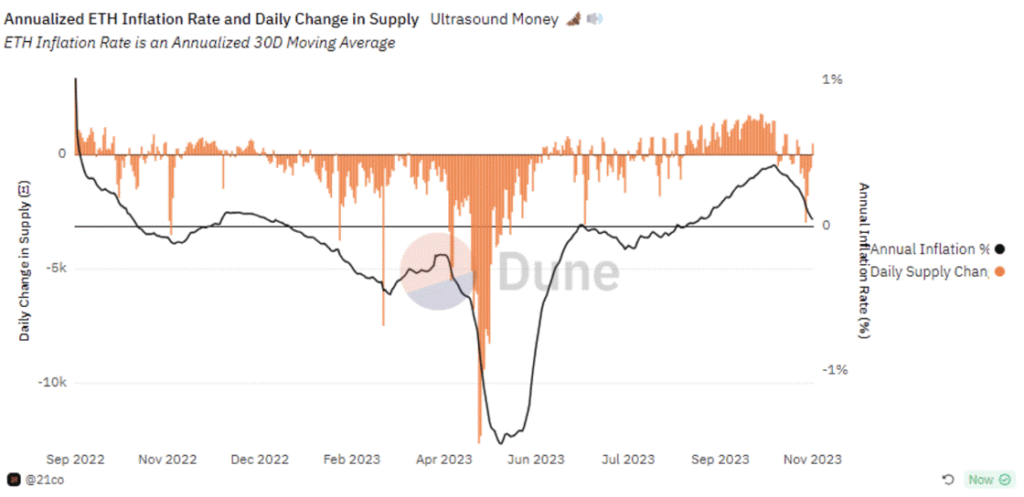

The world’s largest asset manager, BlackRock, officially submitted an application for its iShares Ethereum Trust as a Delaware statutory trust on November 9, joining a handful of firms, including ARK Invest and 21Shares, who were the first to submit their application back in September. With BlackRock’s $8.6 trillion in assets under management, the news spurred optimism in the market, making Ethereum jump by 12.54% overnight, but fundamental developments should also be credited. Increasing base fees and burn rate have returned Ethereum to its June levels, signifying a revival of on-chain activity. As shown in the figure below, Ethereum has become deflationary over the past week, strengthening its worth. However, on November 10, around $41M worth of ETH was lost in over a $100M exploit on a crypto wallet belonging to the crypto exchange Poloniex. Crypto forensics firm Arkham Intelligence showed that the hacker had close to ~$42M on Friday night. In terms of market impact, it would take ETH $8M to move upwards or downwards by 2%. Therefore, the Poloniex hack could yield short-term selling pressure on ETH of about 10%, if the hacker liquidates their looted holdings instantaneously.

Figure 2: Ethereum’s Annualized Inflation Rate and Daily Change in Supply

Source: 21.co on Dune Analytics

Streaming on Bitcoin

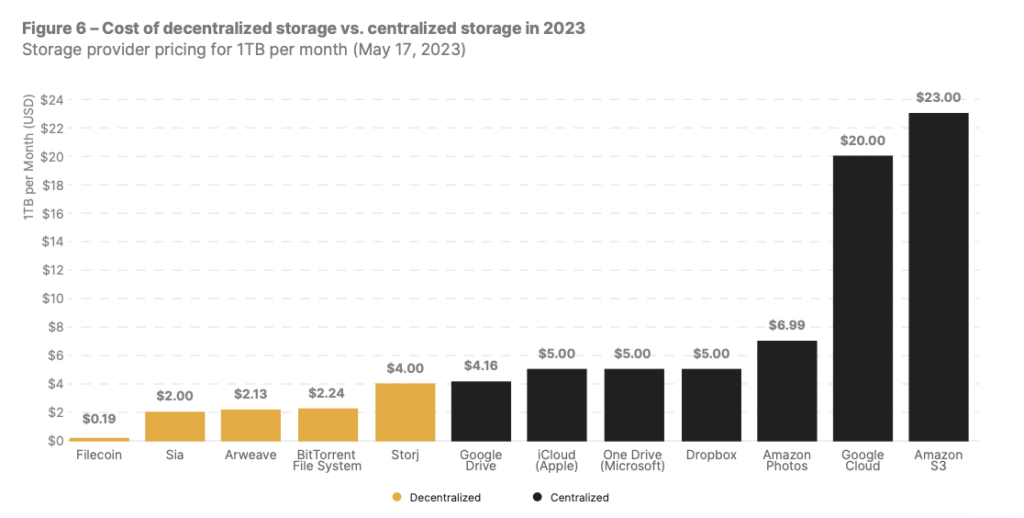

Bitcoin developer Robin Linus introduced BitStream, a decentralized file hosting on Bitcoin, where users can upload unique files, enabling anyone to monetize their excess bandwidth and data storage capacities without relying on trust or heavy-weight cryptography. BitStream’s pay-to-download approach solves the problem of bandwidth costs that could skyrocket beyond the initial download revenue. It allows the server to charge for each download, ensuring that the revenue scales with the popularity and demand for the media, creating a balanced and profitable ecosystem. According to the whitepaper, the uploaded files would be fraud-proof, by splitting them into fixed-sized chunks and then hashed into a Merkle tree to derive a unique fileId. This development is yet another expansion to Bitcoin’s burgeoning use cases and would onboard a diversified audience. With BitStream’s promise, Bitcoin can capture the total addressable market of data storage, which stands at at least $230B. Although BitStream’s pricing scheme is not clear yet, decentralized data storage solutions, like Filecoin and Arweave, have been proven to be a lot cheaper than Google Cloud, Amazon S3, and its other centralized peers, varying by usage, as shown in the figure below.

Figure 3: Cost of decentralized storage vs. centralized storage in 2023

Source: State of Crypto issue 9, Coingecko

Kraken Looks to Build Their Own Blockchain

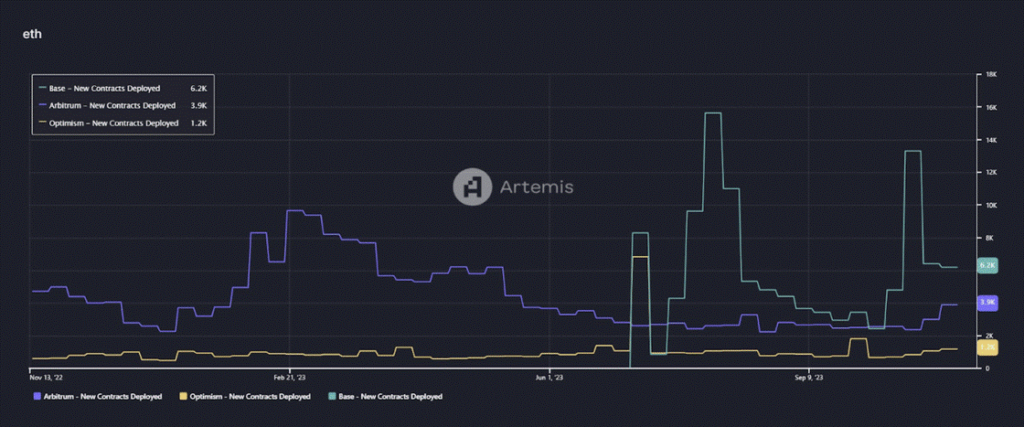

In their pursuit, Kraken is exploring potential partnerships with Polygon Labs, Matter Labs, or the Nil Foundation to establish a Zero-Knowledge-powered network, setting themselves apart from Coinbase. This move isn’t surprising, given Coinbase’s Base accrued ~$5.4M in profit since its launch, equating to around $20 million in annualized profits. Further, despite a recent decline in Base’s sequencer revenue and a 30% drop in AUM over the past weeks, the network still outperforms the rest of ETH scaling solutions in terms of hosting new applications, as shown in Figure 4, indicating a robust developer ecosystem posed to generate diversified income streams. While exchanges launching their networks is not new, the current trend of building atop Ethereum eliminates the necessity for launching a token, which strategically avoids regulatory scrutiny in the current environment. In light of this, we anticipate compliant exchanges to emulate this model and seize the opportunity to capitalize on a diversified income source in the upcoming cycle.

Figure 4: Deployment of New Applications Across ETH Scaling Solutions

Source: Artemis

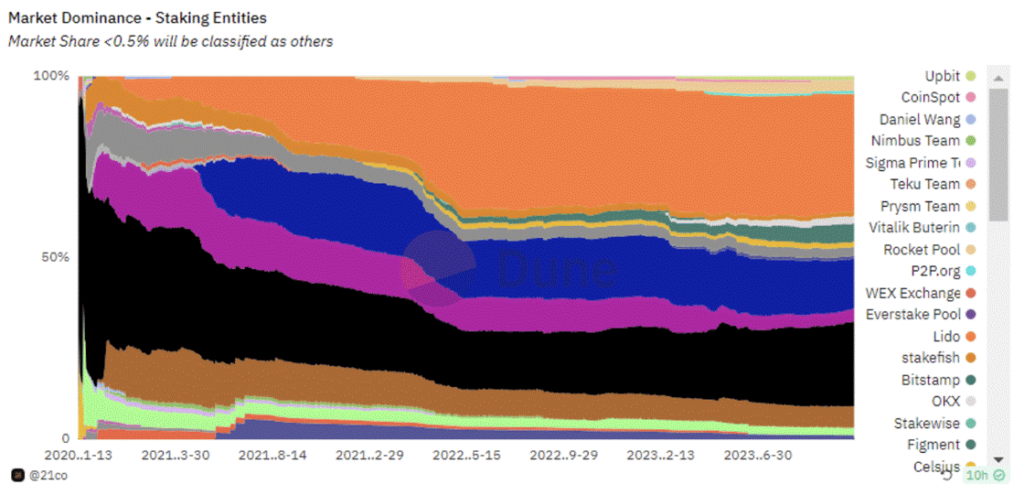

Lido is Decentralizing its Node-Infrastructure Operations

Lido DAO, the largest non-custodial staking provider, approved two proposals to adopt Distributed Validation Technology. DVT refers to a mechanism spreading out key management and signing responsibilities across multiple parties to reduce single points of failure and increase validator resiliency. That said, Lido will integrate DVT modules with Obol and SSV protocols, which is set to introduce a more diverse profile of node operators beyond its current list of 38 Validators and help address a key concern around centralization. This is a key development as Lido stirred a debate since it’s close to accounting for a third of staked ETH (see Figure 5),; it could have undesired influence over the network’s validation process and block production. Thus, this implementation is crucial to ensure the diversification of the protocol’s node operators and increase their reliability in case of validator failures or attempts of censorship. Conversely, SSV and Obol networks represent new primitives, so it’s essential to remain vigilant regarding any unforeseen vulnerabilities they could introduce.

Figure 5: Dominance of Entities Staking on the Ethereum Network

Source: 21co at Dune

What You Should Pay Attention To

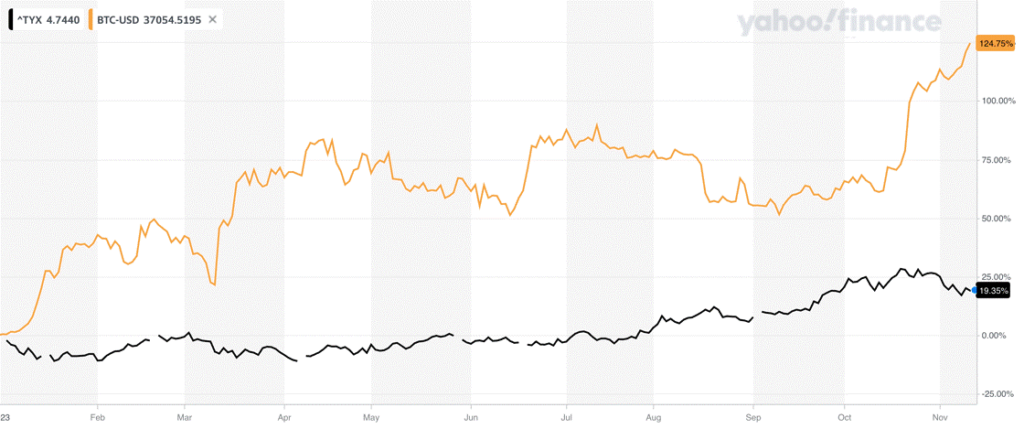

US Credit Outlook: From Stable to Negative

Citing political polarization and fiscal deficits, Moody signals negative indicators for the U.S. economy, lowering the credit rating from stable to negative. 10 and 30-year Treasury yields rose on Monday, taking a toll on investor portfolios and making it more expensive for the government to borrow more money. In the case that the U.S. government doesn’t honor its federal debt of $33.7 trillion, the country might be paving its way to a recession. Although the bull run of Bitcoin can be likely triggered due to speculation around a potential spot ETF in the U.S., the weakening of credit ratings and sticky inflation strengthens Bitcoin’s narrative as a hedge against currency debasement.

Figure 6: 30-Y Treasury Bill Yields Plotted Against Bitcoin’s Performance (YTD)

Source: Yahoo Finance

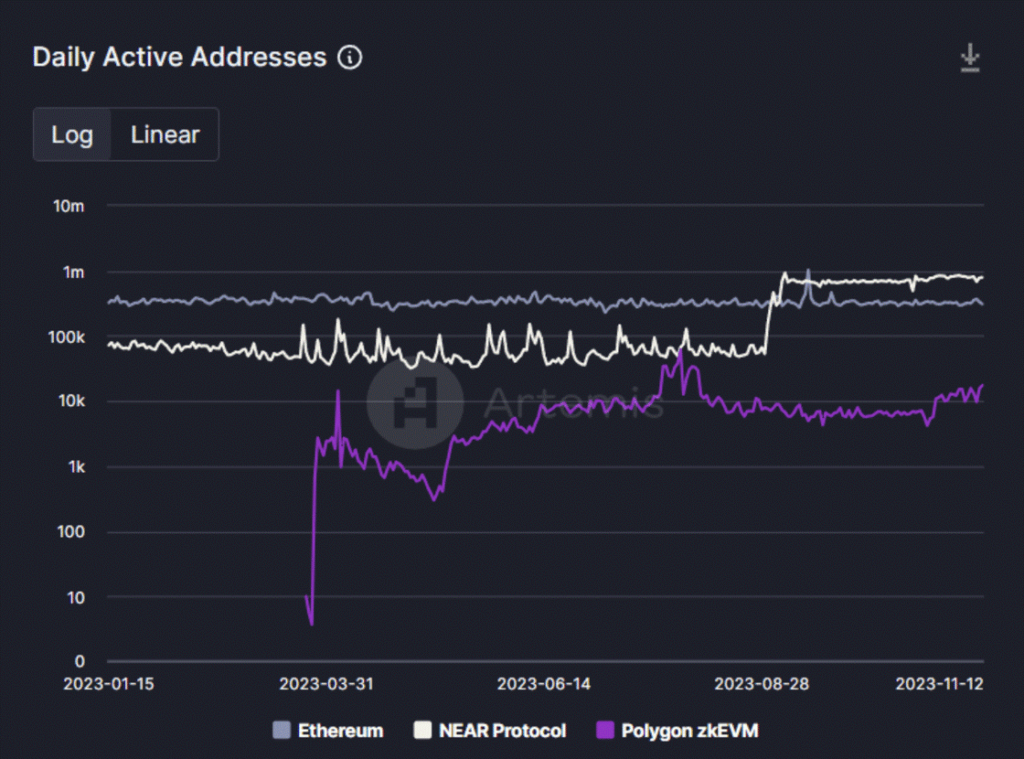

NEAR Announcing Multiple Partnerships Aimed at Closer Alignment with Ethereum

First, Near Foundation unveiled a collaboration with Polygon Labs, marking a significant stride in building a zkWASM prover. In other words, the partnership enables WASM-based networks to validate their settlements on Ethereum, tapping into its battle-tested security guarantees. For context, WebAssembly (WASM) is an alternative operating system to Ethereum’s EVM, offering data efficiency and a versatile toolkit supporting languages like Rust and C++, and powers platforms like Solana, Cosmos, and Near.

This collaboration is pivotal as it provides developers on Polygon CDK with expanded choices for building customizable networks beyond Ethereum’s EVM constraints and using technologies like sharding that are not yet feasible on Ethereum. Finally, the integration facilitates access to Ethereum’s robust liquidity via Polygon’s shared layer, offering a strategic advantage to external non-EVM entities lacking this capability. In essence, this implementation fosters interconnectivity and interdependence between incompatible blockchain operating systems. The synergy also has the potential to propel Polygon’s ZK-EVM user base, enabling it to bridge the gap with both Ethereum and Near networks, as shown below in Figure 7.

Figure 7: Active Daily Users of Near vs Polygon ZK-EVM vs Ethereum

Source: Artemis

Near also revealed its NEAR DA, a new data availability solution offering ETH scaling networks (L2s) like Arbitrum and Optimism, a cost efficient means for posting data. For context, traditional blockchains combine all key functions such as settlement, consensus, execution and data availability, which make networks inefficient as they grow in size. Thus, the modular approach instead focuses on separating few intensive processes, like posting data on Ethereum to prove their validity, in order to help L2 streamline their operations.

In the case of Near, it’s expected to be 8000x cheaper to post data on the network than on Ethereum, specifically it would cost rollups ~$26 to post 100KB of call-data on Ethereum versus $0.0033. Near is now the second protocol offering the modular approach after Celestia announced their mainnet deployment at the end of October. This is a crucial development to help scale the Ethereum ecosystem further and diversify away from the monolithic architectures that are more complex and less flexible.

Comparatively, Near inked a partnership with EigenLabs, the company building the re-staking primitive on top of Ethereum. As a refresher, restaking refers to repurposing staked ETH to validate the security of other applications and networks. With this in mind, Near is building a fast-finality rollup solution, powered by Eigen’s Active Validator Service (AVS), or restakers, to enable near-instant transaction finalization, surpassing the current time frames of hours or days, and is 4000X cheaper than current options. This would ensure that rollups can inherit the security of Ethereum via re-staking, while benefiting from Near’s faster settlement guarantees and help address the fragmentation of liquidity amongst ETH L2s with a cross-rollup communication system in the process. These key developments align with our thesis of a multichain future, with projects seamlessly utilizing various networks in a trustless manner for their distinctive benefits, making infrastructure imperceptible to end-users, while Ethereum continues to wield significant influence in fueling the ecosystem.

Bookmarks

• Insights from our last newsletter were featured on CoinDesk.

• In collaboration with ARK Invest, 21Shares is listing 5 products in the Chicago Board Options Exchange.

• Get a digital copy of State of Crypto issue 10!

Next Week’s Calendar

These are the top 3 events we’re monitoring for next week.

• November 17: UK Retail Sales, European Central Bank’s President Christine Lagarde speaks

• November 21: FOMC Meeting Minutes

• November 23: Flash manufacturing and services PMI data for Germany, France and the UK.

Source: Forex Factory

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

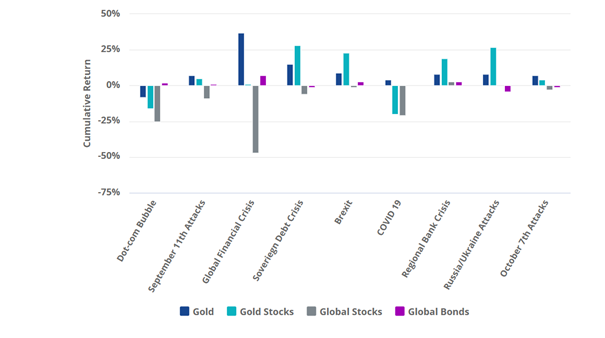

The investment environment in 2025 has been marked by increased uncertainty, including evolving trade dynamics involving the U.S. and rising geopolitical risks, which have weighed on overall market sentiment. Notably, though, gold has shone, surging past the symbolic $3,100 per ounce mark for the first time in history.

Gold has recently gained attention as investors seek potential hedges against rising inflation, currency fluctuations, and broader market volatility. Historical data suggests that both gold and gold mining equities have sometimes outperformed during periods of market stress, though such outcomes are not guaranteed and may vary depending on broader macroeconomic dynamics. The chart below displays historical episodes where gold and gold mining equities experienced relative strength during market corrections. However, such past performance should not be interpreted as a reliable indicator of future results.

Source: VanEck, World Gold Council.

The early months of 2025 have seen a resurgence in gold mining stock interest, with the VanEck Gold Miners ETF (GDX) receiving significant capital inflows. These flows reflect changing investor sentiment but should not be viewed as a guarantee of future returns.

Improved management

While gold mining stocks are a play on the gold price, they are much more than that. In the past, gold mining companies indulged in wanton value destruction. During gold’s last bull market that ended in 2011, mining companies borrowed heavily to fund new developments and extract gold from low quality mines. After the gold price dropped, they were forced to announce write-downs.

But since then, they have learned to keep costs under control. Indeed, for more than 10 years gold mining companies’ costs have grown by far less than a gold price that’s at least doubled. Despite the sharp rise in gold prices, especially in post 2020, miners have lagged significantly, likely reflecting ongoing capital and operating challenges noted between 2011 and 2015. This divergence may suggest a potential value opportunity if mining equities eventually re-rate closer to gold’s performance. Nevertheless, this is an assumption and may not turn out to be true, as structural issues or market dynamics could continue to weigh on miners’ valuations.

Gold Miner Premium/Discount to Gold

Source: Scotiabank. Data as February 2025.

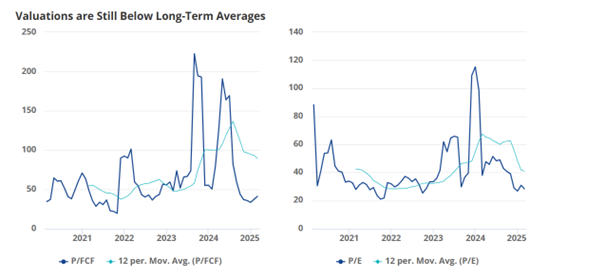

Gold miners are expanding their profit margins, generating cash and embarking on share buy backs. What’s more, many have strong balance sheets. Yet still they trade at valuations below historical averages. Valuation metrics such as price-to-free cash flow (P/FCF) and price-to-earnings (P/E) ratios remain below the 12-month moving average.

Valuations are Still Below Long-Term Averages

Source: Morningstar data.

Gold miners differentiate from gold because they are operating businesses influenced by company-specific factors such as management decisions, production efficiency, regulatory environments, and geopolitical risks. While gold is a passive asset driven by macroeconomic trends, miners add an additional layer of exposure to operational performance and cost structures.

A supportive macro backdrop

The performance of gold mining stocks is naturally influenced by the trajectory of gold prices. From a macroeconomic standpoint, factors such as inflation concerns and central bank policies continue to shape a cautiously optimistic outlook for gold, although the asset remains subject to volatility. Central banks continue to be net buyers, with 2023 marking a record year in terms of official sector demand. This trend has extended into 2024 and early 2025, underscoring institutional confidence in gold as a long-term store of value.

At the same time, the unfolding trade war is contributing to a more volatile global environment. These developments could support the case for gold and, by extension, gold mining equities. Moreover, recent efforts to improve transparency around global gold reserves, including audits of holdings in Fort Knox and London, have added credibility to the market, potentially reducing the perceived risk premium for miners.

Valuable portfolio diversification

From an investor’s perspective, gold mining stocks can be a useful diversifier in a broader equity portfolio, especially at a time of uncertainty for equity markets. Historically, gold mining stocks have exhibited a high sensitivity to changes in the price of gold, sometimes outperforming the metal itself during prolonged bull markets. However, they also tend to underperform during downturns, reflecting their leveraged exposure to gold price movements. Past performance is not indicative of future results. The table below shows the low correlation of the two VanEck gold miners UCITS ETFs with the MSCI World Index of global stock prices. This low correlation suggests that gold mining ETFs may perform differently than global equities, potentially helping to reduce overall portfolio volatility during periods of market stress. That said, they also carry equity-like risks, and investors should assess their portfolio objectives and risk tolerance accordingly.

Low Price Correlations with Stocks

| Investment | MSCI World | Gold Price | VanEck Junior Gold Miners ETF | VanEck Gold Miners ETF |

| MSCI World | 1.00 | |||

| Gold Price | 0.10 | 1.00 | ||

| VanEck Junior Gold Miners ETF | 0.38 | 0.76 | 1.00 | |

| VanEck Gold Miners ETF | 0.31 | 0.81 | 0.96 | 1.00 |

Source: Morningstar data.

A better way to play the rally?

When the VanEck Gold Miners UCITS ETF was introduced in 2015, it aimed to provide investors with a way to gain diversified exposure to gold mining equities. Early performance was tempered by concerns related to past capital discipline within the sector. Recent inflows into ETF may reflect renewed investor interest, although sentiment toward mining equities can remain sensitive to market and operational developments.

As gold glitters at a time of market volatility, there are good reasons to think gold miners may be a better way to play the rally. It should however be noted that while gold prices and mining companies are closely linked, investing in miners introduces additional layers of risk and complexity and investors should consider all the risk factors before investing.

IMPORTANT INFORMATION

This is marketing communication. Please refer to the prospectus of the UCITS and to the KID/KIID before making any final investment decisions. These documents are available in English and the KIDs/KIIDs in local languages and can be obtained free of charge at www.vaneck.com, from VanEck Asset Management B.V. (the “Management Company”) or, where applicable, from the relevant appointed facility agent for your country.

For investors in Switzerland: VanEck Switzerland AG, with registered office in Genferstrasse 21, 8002 Zurich, Switzerland, has been appointed as distributor of VanEck´s products in Switzerland by the Management Company. A copy of the latest prospectus, the Articles, the Key Information Document, the annual report and semi-annual report can be found on our website www.vaneck.com or can be obtained free of charge from the representative in Switzerland: Zeidler Regulatory Services (Switzerland) AG, Neudtadtgasse 1a, 8400 Winterthur, Switzerland. Swiss paying agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zürich.

For investors in the UK: This is a marketing communication targeted to FCA regulated financial intermediaries. Retail clients should not rely on any of the information provided and should seek assistance from an IFA for all investment guidance and advice. VanEck Securities UK Limited (FRN: 1002854) is an Appointed Representative of Sturgeon Ventures LLP (FRN: 452811), which is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, to distribute VanEck´s products to FCA regulated firms such as Independent Financial Advisors (IFAs) and Wealth Managers.

This information originates from VanEck (Europe) GmbH, which is authorized as an EEA investment firm under MiFID under the Markets in Financial Instruments Directive (“MiFiD). VanEck (Europe) GmbH has its registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, and has been appointed as distributor of VanEck products in Europe by the Management Company. The Management Company is incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM).

”The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk for any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”), expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, noninfringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. It is not possible to invest directly in an index.”

This material is only intended for general and preliminary information and shall not be construed as investment, legal or tax advice. VanEck (Europe) GmbH and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed.

VanEck Gold Miners UCITS ETF (the ”ETF”) is a sub-fund of VanEck UCITS ETFs plc, an open-ended variable capital umbrella investment company with limited liability between sub-funds. The ETF is registered with the Central Bank of Ireland, passively managed and tracks an equity index. Investing in the ETF should be interpreted as acquiring shares of the ETF and not the underlying assets.

VanEck Junior Gold Miners UCITS ETF (the ”ETF”) is a sub-fund of VanEck UCITS ETFs plc, an open-ended variable capital umbrella investment company with limited liability between sub-funds. The ETF is registered with the Central Bank of Ireland, passively managed and tracks an equity index. Investing in the ETF should be interpreted as acquiring shares of the ETF and not the underlying assets.

Investing is subject to risk, including the possible loss of principal. Investors must buy and sell units of the UCITS on the secondary market via a an intermediary (e.g. a broker) and cannot usually be sold directly back to the UCITS. Brokerage fees may incur. The buying price may exceed, or the selling price may be lower than the current net asset value. The indicative net asset value (iNAV) of the UCITS is available on Bloomberg. The Management Company may terminate the marketing of the UCITS in one or more jurisdictions. The summary of the investor rights is available in English at: complaints-procedure.pdf (vaneck.com). For any unfamiliar technical terms, please refer to ETF Glossary | VanEck.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH ©VanEck Switzerland AG © VanEck Securities UK Limited

iShares noterar fond för flyg- och försvarssektorn på Xetra

8RMY ETF köper bara aktier i europeiska försvarsföretag

Are Gold Mining Equities Regaining Attention Amid Rising Gold Prices?

Fem spanska fonder som har ökat med +12% under 2025

ASRP ETF ett spel på medtech företag världen över

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Svenskarna har en ny favorit-ETF

MONTLEV, Sveriges första globala ETF med hävstång

Sju börshandlade fonder som investerar i försvarssektorn

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEuropeisk försvarsutgiftsboom: Viktiga investeringsmöjligheter mitt i globala förändringar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa

Pingback: How Markets Reacted to New US Credit Rating: What Happened in Crypto Last Week? | Aktiegruvan