Nyheter

Gold, Oil, and Inflation in 2018

Like Bitcoin, Dogecoin uses a proof-of-work (PoW) consensus mechanism but runs on its own blockchain, originally forked from Litecoin. It uses the Scrypt hashing algorithm, which is less resource-intensive than Bitcoin’s SHA-256, making mining more accessible to everyday users with consumer-grade hardware. Due to merged mining with Litecoin, Dogecoin benefits from shared infrastructure, with hashpower recently reaching all-time highs of 2.7 petahashes (quadrillion hashes) per second, making the network increasingly difficult to attack.

Dogecoin’s design is built for speed and utility, has no maximum supply, and confirms blocks every minute (10x faster than Bitcoin). Moreover, it maintains ultra-low transaction fees, which is ideal for tipping, microtransactions, and everyday use.

More than a meme

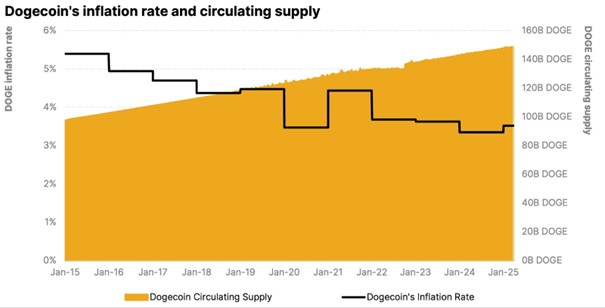

Although its supply is technically unlimited, Dogecoin’s issuance model is clear and predictable. Approximately 10,000 DOGE are mined every minute, adding up to around 5.25 billion new tokens each year. As the supply base expands, this fixed issuance creates a natural disinflationary trend that has cut nearly in half over the past decade while ensuring network security through consistent miner rewards.

Dogecoin’s technology fosters an aligned ecosystem between users and miners. With sustainable economic incentives, it acts as a kind of “retail Bitcoin”, built not just for hoarding but for real-world use, too.

While Dogecoin began as a lighthearted experiment, its evolution has proven it to be far more than a meme. Thanks to its speed, low fees, and strong community backing, Dogecoin has grown into a functional digital currency with a range of real-world use cases. From payments and merchant adoption to infrastructure development and charitable giving, Dogecoin continues to demonstrate its staying power as a practical and accessible tool in the broader crypto ecosystem.

Dogecoin as a payment tool

Dogecoin has transformed into a widely accepted digital currency, embraced by major brands like Tesla, AMC, Newegg, and the Dallas Mavericks. With fast transaction speeds and low fees, even amid surging transaction volumes, it has become a practical option for everyday payments. Crypto payment processors like BitPay have further expanded its reach, enabling thousands of merchants worldwide to accept DOGE. Most recently, The Open House Group, a prominent Tokyo Stock Exchange-listed real estate firm, added Dogecoin to its supported list, making it one of the few digital assets accepted for property transactions.

Enhancing Dogecoin’s payment infrastructure

Initiatives like Dogebox and GigaWallet are simplifying DOGE integration for businesses, while its scaling solution, Laika, is making meaningful progress in improving transaction speed and reducing costs.

Meanwhile, RadioDoge is working to expand access by enabling offline transactions in remote regions through low-cost radio and Starlink technology, advancing global crypto inclusion. A rumored integration with Elon Musk’s X platform could extend Dogecoin’s utility across digital tipping and commerce. These efforts collectively reinforce Dogecoin’s growing relevance in real-world payments and its potential as a frictionless, decentralized transaction layer.

Do Only Good Every Day

As we’ve seen, community drives memecoins, and Dogecoin’s community shines the brightest. This global network not only thrives on memes but also channels that energy into social good. From funding clean water in Kenya to sending Jamaica’s Bobsled Team to the Olympics and raising over $1 million for Ukraine relief, DOGE’s community transforms internet culture into real-world impact. Low fees and fast transactions make it a favorite for grassroots giving, showing a coin born as a joke can leave a lasting legacy. Dogecoin is more than a digital asset—it’s a movement powered by a community that believes in doing good every day.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Börshandlade fonder för den som vill investera i skogen

EDOG ETF med fokus på telemedicin och digital hälsa

The Dogecoin story: The emerging “intrinsic value”

JCLU ETF är en högkvalitativ aktiv europeisk CLO-ETF

SAVR erbjuder nu handel i mer än 700 polska aktier

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Svenskarna har en ny favorit-ETF

MONTLEV, Sveriges första globala ETF med hävstång

Sju börshandlade fonder som investerar i försvarssektorn

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEuropeisk försvarsutgiftsboom: Viktiga investeringsmöjligheter mitt i globala förändringar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedan21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa