Nyheter

FlexShares: Expectations For Real Assets

In any market environment, we believe that real assets should be an essential element of every investment portfolio. Growing numbers of institutional investors have steadily increased their real asset allocations over the past few decades. We believe investors are looking for what real assets can offer: the potential for income, gains and capital preservation in an unclear global environment. FlexShares: Expectations For Real Assets

Investors continue to benefit from innovation within a variety of investment vehicles that focus on real assets. Furthermore, strong demand for real assets is being met with an unprecedented supply of opportunities for investment, and we believe trends indicate that it will continue to grow. The Real Assets classification (e.g., timber, water, infrastructure, natural resources, etc.) is continually evolving, influenced not only by new asset types, but also regulatory and issuance changes.

Defining The Asset Class And Its Potential

Real assets—which we define as real estate, infrastructure and natural resources—form the pillars of the global economy. As such, these classifications are inherently tied to global developments, inflation and other macroeconomic trends. Notably, the cash flows that historically have been produced by real assets can be valuable in times of both economic expansion and contraction. Real assets represent physical assets that are often linked to inflation—a favorable characteristic as potential demand rises in periods of economic expansion.

At the same time, increasing demand for the goods and services that real assets provide may be relatively predictable and inelastic (insensitive to changes in price or income), which can be helpful in periods of economic contraction.

While cash-flow stability has historically been characteristic of real asset investments, the fundamentals that drive the cash flows are distinct. As such, real assets can provide an effective way to enhance portfolio diversification beyond traditional stock and bond allocations.

Portfolio Diversification

Real asset returns have historically had low correlations to traditional equity and fixed-income investments. Our findings suggest they can provide an effective way to enhance the diversification of a traditional stock and bond portfolio. Individual real asset categories have also shown low correlations with each other—consequently investors may be able to diversify further by investing in more than one real asset class.

As highlighted in the chart below, the correlations of real estate with infrastructure and natural resources are 0.85 and 0.62, respectively. The return streams of two assets having a correlation of 1.00 would be perfectly correlated. These measures are relatively moderate because the drivers behind the returns of these categories are distinct.

Consider natural resource pricing, which for some assets, like timber, is highly dependent on short-term factors such as climate, temperature and water supply. In contrast, the cash flows from some infrastructure assets, such as toll roads, tend to rise with an expanding economy, while those derived from more essential services, such as utilities, tend to be more highly regulated, and consequently during times of economic weakness tend to have more locked-in levels of usage pricing.

Capital Appreciation Potential

Our research has shown that both income return and capital appreciation represented meaningful amounts of the historical total returns generated by real assets. Historically, many of these hard assets have tended to be long term and increase in value over time as replacement costs rise and operational efficiencies are achieved.

For many investors, this scenario may be visualized within their own daily experience as they observe the leasing of vacant space, the climb of toll road fees, the rising use of energy or increases in lumber prices. We believe that income from real-asset-related investments may help protect value on the downside, while operational efficiencies may enhance value on the upside.

Potentially Higher Risk-Adjusted Returns

Adding real assets may also enhance the risk-adjusted returns* of a mixed-asset portfolio. The chart below shows the various historical Sharpe ratios of the three real asset categories in comparison to stocks and bonds. The Sharpe ratio is a measure of return per unit of risk, which indicates whether an investment’s return sufficiently rewards investors for the level of risk assumed (the higher the Sharpe ratio, the greater the level of risk-adjusted performance).

For example, the 10-year Sharpe ratio for infrastructure as defined in the chart below is 0.214, which means that an investor should have a greater risk-adjusted return in comparison to an investment in real estate and in comparison to a Treasury bond which has a Sharpe ratio of zero. Only when an investor compares one investment’s Sharpe ratio with that of another investment can the investor get a feel for the return versus the relative amount of risk they can expect to take to achieve that return.

While real assets tend to retain value during economic downturns and contribute to value creation during economic upturns, performance generally lacks drastic movements in either direction. This potential performance stability may provide investors with portfolio benefits in a variety of market environments.

Implementing The Real Assets Portion Of A Portfolio

A number of considerations should be taken into account whenbuilding a portfolio of real assets. One approach for the initial structure isto define the investor’s objectives in terms of yield versus growth-orientedstrategy and sensitivity to the impact of inflation.

For the Yield Investor, a real assets strategy may emphasizeincome-oriented but inflation-sensitive investments that generate potentialsteady cash flows.

For the Growth Investor, a real assets strategy mayseek broader exposure to natural resources to help pursue a growth objective.

For the Growth Investor, a real assets strategy mayseek broader exposure to natural resources to help pursue a growth objective.

Building a real asset portfolio is a process that requires multiple considerations in terms of planning, implementation and monitoring. Real assets can play a fundamental role in a portfolio, depending on an investor’s objectives. Given the current low-yield environment, along with the potential diversification that real assets have historically provided, we believe that investors should consider them in order to create a well-diversified portfolio.

*Risk-adjusted return refines an investment’s return by measuring how much risk is involved in producing that return.

This is an excerpt from FlexShares’ research paper on Expectations for Real Assets.

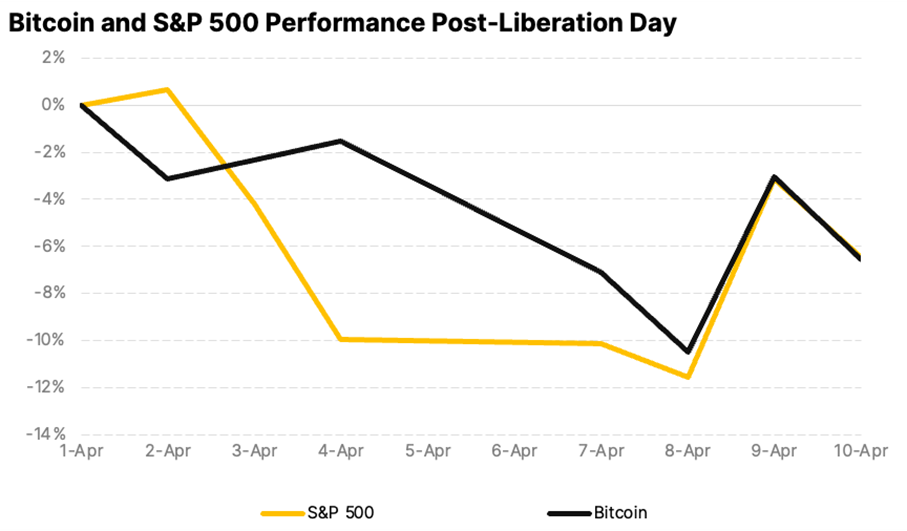

Since U.S. President Donald Trump announced tariffs on April 2, termed ”Liberation Day,” global markets have experienced significant volatility. The S&P 500 shed $5.83 trillion in market value over just four days, marking its steepest drop since the 1950s. Asian markets saw their worst session since 2008, reflecting widespread fears of an economic slowdown.

The U.S. 10-year Treasury yields initially fell below 4% as investors sought safety, but by April 8-9, they surged to a seven-week high of 4.515%. This spike, driven by bond market sell-offs potentially from basis trading or China’s strategic moves to pressure U.S. negotiations, suggests a precarious economic situation rather than risk-on sentiment.

On April 9, President Trump announced a 90-day pause on tariffs for most countries (excluding China, where tariffs jumped to 145%) in an effort to give markets time to absorb the changes and calm volatility. The move sparked a broad rally, with the S&P 500 surging 9.5% for its best day since 2008 and Bitcoin rebounding above $80,000 after a turbulent stretch.

Bitcoin is macro now

Despite persistent concerns about crypto volatility, Bitcoin’s price over the past two weeks has closely mirrored the S&P 500 and has actually been less volatile. This alignment reflects Bitcoin’s growing maturity as an asset class and highlights its resilience. As a highly liquid and accessible asset, it continues to attract investors looking for relative value in turbulent markets.

Sentiment shifts toward crypto ETFs

Spot Bitcoin ETFs recorded $700 million in outflows, while Ethereum ETFs lost $400 million since March, marking a sharp reversal after nine consecutive months of inflows. The pullback points to growing institutional caution amid broader macro uncertainty. Still, on-chain data reveals that long-term holders have been steadily accumulating since January lows, signaling continued confidence in the asset class.

Macroeconomic uncertainty takes center stage

The latest U.S. CPI print came in at 2.4%, which was lower than expected. A rate cut in May still seems premature as markets assess the full impact of new protectionist measures. Federal Reserve Chair Jerome Powell has warned that tariffs could raise inflation while slowing growth. As a result, the probability of three rate cuts in 2025 now exceeds 60%. Declining yields may be an early signal of future monetary easing, which could favor risk assets like crypto if economic pressures intensify.

Bitcoin: Dollar’s ally or alternative?

In the face of policy uncertainty, the debate around the U.S. dollar’s reserve currency status is gaining momentum. With its decentralized and censorship-resistant design, Bitcoin is emerging as both a potential complement and challenger to the dollar, especially as the U.S. increasingly wields its currency as a geopolitical tool through tariffs and sanctions.

Meanwhile, Bitcoin’s fundamentals remain solid. Hashrate is at all-time highs, regulatory clarity is improving, and long-term holders continue to accumulate. With prices consolidating above $80K, the current correction may offer a strategic opportunity for investors positioning for the next leg of growth, particularly as the macro picture evolves.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

iShares och Franklin Templeton listar nya ETFer på Xetra

BE28 ETF företagsobligationer med förfall 2028 och inget annat

Trump’s trade war puts Bitcoin in the spotlight

YCSH ETF är en satsning på den europeiska dagslåneräntan

Crypto’s stress-tested resilience

Fonder som ger exponering mot försvarsindustrin

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Warren Buffetts råd om vad man ska göra när börsen kraschar

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Svenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf lanserar Europa-fokuserad försvars-ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV mars 2025