Nyheter

Enter the dragon: Parsing Lunar New Year opportunities among emerging markets

As we enter the year of the dragon, Dina Ting, Head of Global Index Portfolio Management, assesses the opportunities and risks in China and Taiwan, which saw divergent market performance last year. She also highlights a region that not only has seen rising engagement with China but was also an EM bright spot that outperformed the S&P 500 Index in 2023—Latin America.

While Western season’s greetings are merry with wishes of joy, peace, love and blessings, those for Chinese cultures tend toward “good fortune.” In tandem with happiness for the Lunar New Year, wishes for prosperity are typical—and something that China investors could certainly use as we enter the year of the dragon.

China and Hong Kong markets had a humbling 2023 with equities down more than 10%. Fortunately, regulators in Beijing have turned up the dial on reform measures to stoke some of that auspicious dragon luck. Expectations are rising for even more support to come. In early February, China’s central bank made changes to allow its financial institutions to hold smaller cash reserves, cutting the reserve requirement ratio by 50 basis points. This is set to release nearly US$140 billion in long-term capital as Beijing seeks to boost targeted growth and market confidence.

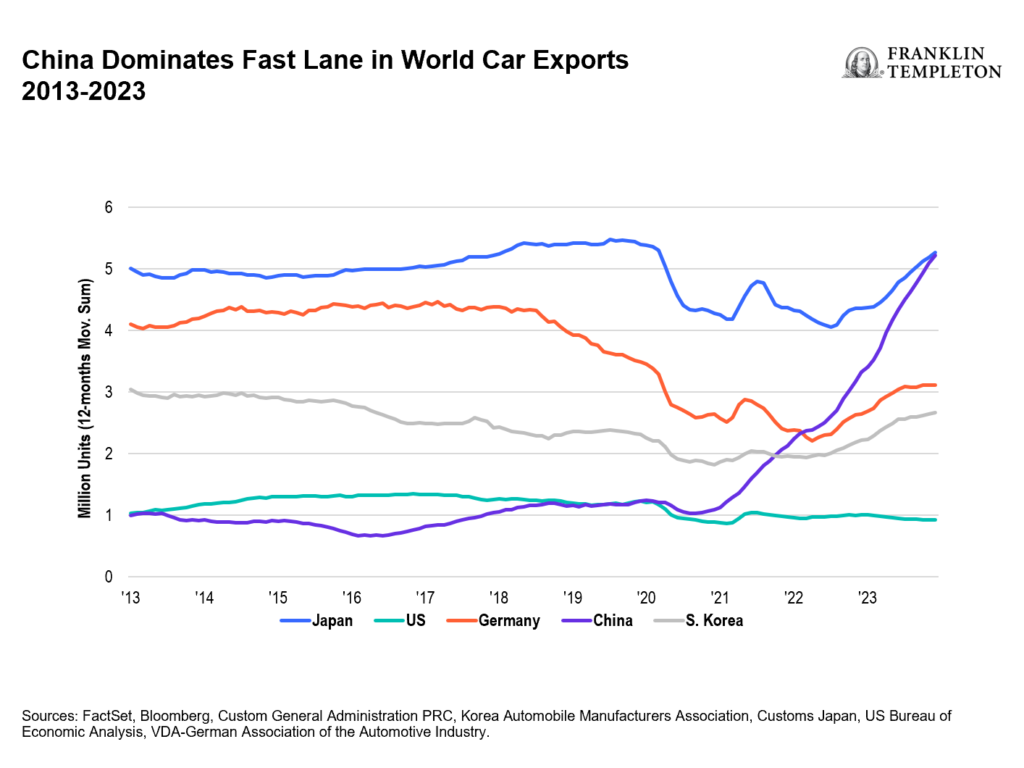

A rise in the country’s passenger vehicle sales also offers some hope, and 2023 saw China surpass Japan as the world’s largest car exporter.1 Year-over-year retail passenger car sales were up 57% in January, according to the China Passenger Car Association. The country’s expertise in so-called new-energy vehicles—fully electric and plug-in hybrids—is partly responsible for the export surge.2 Another important shift to note is that China’s auto industry is increasingly shipping to wealthier countries—exports to Australia tripled year-over-year during the first half of last year and sales to Spain rose 17-fold to nearly 70,000 vehicles.3 With renewed government support, China’s electric vehicle (EV) makers are making a big splash on the world stage. Shenzhen-based automaker BYD overtook Tesla as the world’s top seller of EVs at the end of 2023, and China’s overall passenger EV sales are forecast to make up 59% of world sales this year, compared to 50% in 2019.4

Still re-opening

Beijing has also begun stepping up tourism and travel promotions, granting visa-free entry to 11 countries, with Singapore and Thailand the latest to be included. Other policies to combat soft consumer demand include simplified visa procedures that allow travelers to apply for entry permits upon arrival at some ports and lower visa application fees for some foreign nationals.

In our view, Beijing’s recent spate of new reform policies should hold long-term benefits for its state-owned enterprises (SOEs), including its “big four” banks, as well as corporations entrenched in the country’s energy sector. Of course, China’s domestic deflationary pressures and real estate market weakness remain dominant concerns.

Beyond the Magnificent Seven (Mag7),5 which drove US equity returns last year, the broader equity market had less impressive returns over the same period. Big tech’s outperformance, coupled with sharp declines in China, may have also obscured some encouraging trends for emerging markets (EM), where we saw pockets of stellar performance. Understandably, global investors may feel inclined to await more regulatory clarity before warming to China’s markets. Keep in mind that a typical EM portfolio, such as the FTSE Emerging Index, holds about a 25% weighting in mainland China versus 18% for Taiwan.6 The MSCI AC Asia ex Japan Index holds a 29% exposure to China versus 19% for Taiwan.7 So for a more precise, targeted approach, investors may consider low-cost single country-focused exchange-traded funds to express tactical views.

2023 outperformers

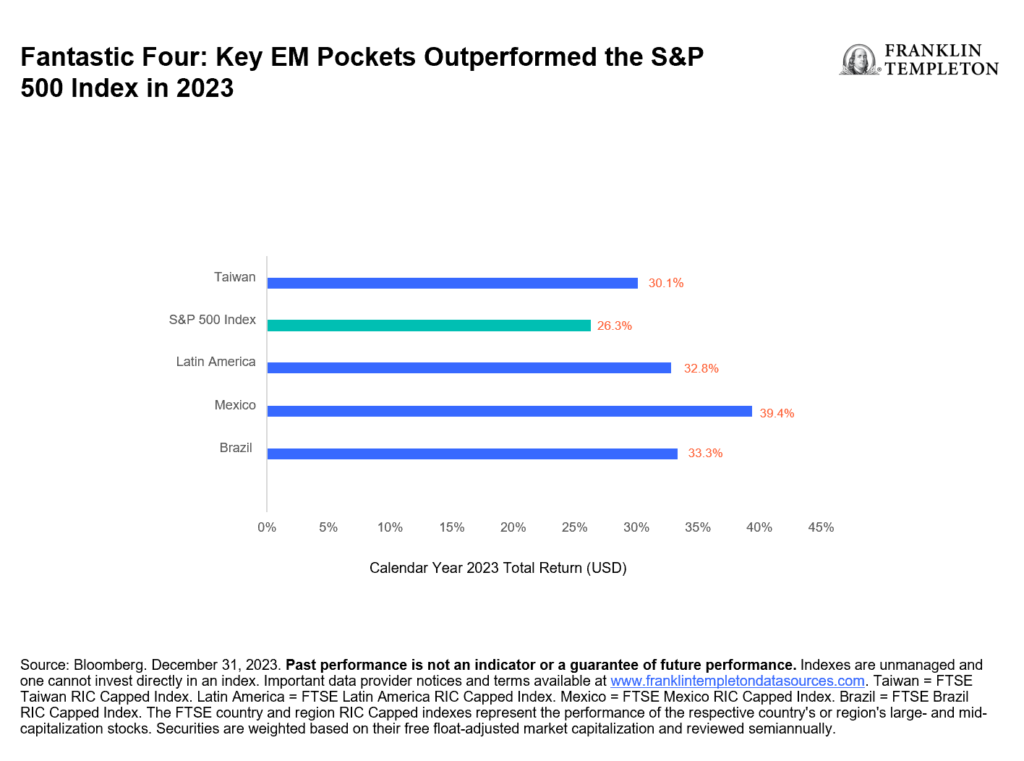

Instead of “Mag7,” perhaps “Fantastic Four” can catch on as a moniker for four pockets within EM markets that outperformed the S&P 500 Index last year. They are Taiwan, Mexico, Brazil and Latin America, which predominantly consists of its two largest economies.

Excluding China, EM stocks (as measured by the MSCI Emerging Markets ex China Index) returned 20.1% in 2023,8 with Latin America (as measured by the FTSE Latin America RIC Capped Index) faring well, up 33% for the year.9 The equity markets of Mexico (39.4%, as measured by the FTSE Mexico RIC Capped Index) and Brazil (33.3%, as measured by the FTSE Brazil RIC Capped Index) were standouts, and in Asia, tech powerhouse Taiwan (30.1%, as measured by the FTSE Taiwan RIC Capped Index) also posted stellar performance.10 For investors wanting to capture both of Latin America’s largest economies, the FTSE Latin America RIC Capped Index has a combined weighting of more than 90% in Brazil and Mexico, and notably lacks exposure to Argentina. In recent years, China has cultivated a growing influence in Latin America with trade pacts, overseas foreign direct investment and loans playing a major role in its strengthened ties with the region. While India’s market slightly trailed the S&P 500 last year, it still exhibited robust growth and is increasingly seen as an appealing alternative to China among both businesses and investors.

When chips are down…

Looking ahead, analysts expect an ongoing resurgence in global semiconductor sales to continue boosting Taiwan’s market. Powered by artificial intelligence and 3D tech, the chips revenue comeback is forecast to see a low to mid-teens percentage increase this year.11 Furthermore, to meet growing demand in key markets, Taiwan’s most valuable chip giant plans to expand its global footprint. In collaboration with Sony and Toyota, Taiwan Semiconductor Manufacturing has new plans to build a second plant in Japan.

In January, Taiwan saw its overall exports expand for a third consecutive month with an 18% year-over-year rise.12 During the month, the ruling Democratic Progressive Party’s (DPP) retention of the presidency in Taiwan’s recent elections appeared to support continuity in its economic policy. Although cross-straits relations continue to pose risks, markets had largely factored in the pro-independent DPP’s narrow victory.

- Source: “China Overtakes Japan As World’s Biggest Vehicle Exporter.” Barron’s. January 31, 2024.

- Sources: Xinhua news agency, China Passenger Car Association.

- Source: “How China became a car-exporting juggernaut.” The Economist. August 10, 2023,

- Source: BloombergNEF.

- The Magnificent Seven are (Mag7) Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia and Tesla.

- Source: FTSE Russell, February 13, 2024. The FTSE Emerging Index provides investors with a comprehensive means of measuring the performance of the most liquid large- and mid-cap companies in the emerging markets. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

- Source: MSCI, January 31, 2024. The MSCI AC Asia ex Japan Index captures large- and mid-cap representation across two of three developed market countries (excluding Japan) and eight emerging market countries in Asia. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

- Source: Bloomberg, as of December 31, 2023. The MSCI Emerging Markets ex China Index captures large- and mid-cap representation across 23 of the 24 emerging market countries excluding China. Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

- Source: Bloomberg, as of December 31, 2023. The FTSE country and region RIC Capped indexes represent the performance of the respective country’s or region’s large- and mid-capitalization stocks. Securities are weighted based on their free float-adjusted market capitalization and reviewed semiannually. Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

- Ibid.

- Sources: Deloitte, Semiconductor Industry Association, Gartner, Inc.

- Source: Ministry of Finance, Republic of China, February 2024.

This message may contain information that is legally privileged or confidential. If you received this transmission in error, please notify the sender by reply email, and delete the message and any attachments. This transmission is believed to be defect free; however, no responsibility is accepted by the sender for damage arising from its receipt.

All email and instant messages (including attachments) sent to or from Franklin Templeton (FT) personnel may be retained, monitored and/or reviewed by FT and its agents, or other authorized parties as disclosed in FT’s Privacy Notice, without further notice or consent. Refer to our country/region specific Privacy & Cookies Notice, which you can read here or access directly at: http://www.franklintempletonglobal.com/privacy to learn more. Depending on your location, other privacy laws and regulations may also apply to you.

Last week, I was in Washington, DC to attend the DC Blockchain Summit and to meet with regulators and policymakers to share our experiences as a crypto-focused asset manager over the last seven years.

The Summit, hosted by The Digital Chamber, included speeches from dozens of members of Congress, regulators, and industry leaders. After listening to presentations and speaking with a number of regulators and policymakers I have one key takeaway: Regulatory clarity for crypto will come much faster than I previously anticipated.

A dramatic shift in tone

As I wrote in January, US policymakers and government leaders—at nearly every level—are embracing this technology. For years, the lack of clear rules for digital assets in the US has been a major obstacle for institutional investors and financial firms looking to enter the crypto space. However, this past week in DC, as well as several of the conversations I’ve had with advisors and wealth managers over the last several weeks, has left me with an even higher sense of optimism.

One of the most striking takeaways from my meetings was the shift in how policymakers are discussing crypto. Just a year ago, many in Washington viewed digital assets primarily through the lens of risk—concerns over fraud, illicit finance, and speculative volatility dominated the conversation. While these concerns still exist, the discussions now are much more nuanced and focused on the opportunities that crypto can create to the American economy and how to address these risks through a clear regulatory framework.

Bipartisan support for legislation

Perhaps the most encouraging sign is the concrete progress being made on both legislative and regulatory fronts. Several key developments indicate that clearer guidelines for crypto businesses and investors could arrive sooner than expected. There is growing bipartisan momentum behind crypto-related legislation. The House Financial Services Committee and the Senate Banking Committee are moving forward with stablecoin legislation, and it is possible legislation could be signed into law as early as this summer. Stablecoins have also been a key focus of regulatory discussions, with growing consensus that they should be subject to clear guidelines similar to those governing payment systems and money market funds.

House and Senate committees are also actively discussing proposals that aim to define the jurisdiction of regulatory agencies, clarify the status of digital assets, and establish consumer protections. Unlike previous years, these efforts are being taken seriously by both parties, increasing the likelihood of meaningful legislative progress.

Adding to these regulatory discussions is the growing demand for crypto exposure from institutional investors. This demand is influencing policymakers and regulators, as they recognize that a lack of clarity is pushing innovation overseas.

What does this shift mean for investors?

The acceleration of regulatory clarity is a significant development for investors. While the approval of spot bitcoin ETFs last year was a watershed moment, it’s just the beginning. Several large financial institutions, including major banks and asset managers, are actively exploring tokenization, digital asset custody, and blockchain-based financial infrastructure. These institutions are engaging with regulators, advocating for a clear framework that allows them to enter the market with confidence.

Uncertainty has been one of the biggest barriers to broader crypto adoption by financial institutions and institutional investors in particular. As regulations become clearer this year, we expect to see:

• Increased institutional participation: With regulatory uncertainty diminishing, more traditional financial institutions will feel comfortable offering crypto products and using crypto technologies such as stablecoins to offer more efficient services, driving further mainstream adoption.

• Growth in tokenization and blockchain use cases: Clearer regulations will pave the way for asset tokenization, improving efficiency in markets like real estate, bonds, and private equity.

• A stronger US crypto market: By establishing a clear regulatory framework, the US can assert itself as a global financial leader, which we believe will help spur more regulatory clarity in other jurisdictions.

Final thoughts

The message from Washington is clear: crypto regulation is coming, and it’s coming faster than many expected. While there are still hurdles to overcome, the shift from uncertainty to structured regulation is well underway. For investors, this marks an important transition. Clearer rules will reduce risks, enhance market stability, and unlock new opportunities for institutional and retail participants alike.

At Hashdex, we remain committed to navigating these changes and providing investors with access to the best opportunities in this evolving landscape. As we move forward, continued engagement with regulators, policymakers, and financial institutions will be key. The crypto industry has a critical role to play in shaping the future of regulation, and by working collaboratively, we can help ensure that the next phase of crypto’s growth is built on a foundation of clarity and trust.

BSE9 ETF bara företagsobligationer med förfall 2029

Crypto’s political tailwinds are blowing hard: Lessons from a week in Washington

SPUT ETC spårar priset på uran

VanEck ETF utökar sitt kryptoerbjudande med Celestia ETN

B4NZ ETC en eurohedgad satsning på WTI Crude

Fonder som ger exponering mot försvarsindustrin

WisdomTree lanserar europeisk försvarsfond.

Warren Buffetts råd om vad man ska göra när börsen kraschar

De bästa börshandlade fonderna för tyska utdelningsaktier

Trumps återkomst får europeiska aktier att rusa

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanWisdomTree lanserar europeisk försvarsfond.

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa börshandlade fonderna för tyska utdelningsaktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanTrumps återkomst får europeiska aktier att rusa

-

Nyheter3 dagar sedan

Nyheter3 dagar sedanSvenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanUtdelning i XACT Norden Högutdelande mars 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf lanserar Europa-fokuserad försvars-ETF