Nyheter

Disappointment creates opportunity

FX Research Disappointment creates opportunity

Highlights

• The US Federal Reserve (Fed) lowered its projected policy path at its September meeting, causing the USD to experience a broad based drop.

• Market expectations of a December interest rate hike fell marginally, despite indications from Yellen and other committee members that a 2016 rate hike is on the table.

• The USD/JPY and AUD/USD currency pairs offer attractive levels from which to enter long/short tactical positions.

Meetings fall short

The US Federal Reserve (Fed) delivered a dovish message at its monetary policy meeting this Wednesday, causing the trade weighted US Dollar to fall approximately 1.2%. Clear indications of a December rate hike from Fed chair Janet Yellen were overshadowed by downward revisions to the Fed’s 2016 full year growth forecast (by 0.2% to 1.8%) and projected policy path, now forecasting only one hike this year followed by two in 2017 (compared to two and three respectively predicted in June – see Figure 1). The change in the Fed’s assumptions appeared be underpinned by a greater focus toward sustaining the recent rise in inflation, justifying a more “wait and see” approach to the current tightening cycle. It remains our view that by following this tactic the Fed is at risk from making a policy mistake as domestic inflationary pressures continue to mount and threaten to de-anchor inflation expectations (see Why the FOMC should hike but won’t). With the Bank of Japan (BoJ) also delivering an insufficiently accommodative monetary policy framework on Wednesday, the USD/JPY soared 2.61% intraday, pushing the pair to increasingly oversold levels.

We believe that the US labour market reports scheduled for release in the next three months will come in strong and prompt greater pricing of a rate hike in December, causing the USD to rally into year end. This view is best expressed by gaining bullish exposure to the USD/JPY and bearish exposure to AUD/USD, both of which look extended following market disappointment over the past few days.

Market pricing unchanged

Market pricing of December rate hike has barely moved following Wednesday’s meeting, slightly falling to 58.4% from 58.7%. This is surprising given the fact that Yellen explicitly stated that the “case for an increase had strengthened” and three members of the committee (namely Esther George, Loretta Mester and Eric Rosengren) dissented, voting towards an immediate increase in the policy rate. Put in perspective, this time last year only one committee member, Jeffrey Lacker, voted for a hike. We therefore see current market pricing of a December hike as insufficient and believe expectations will rise as incoming US labour market data affirms progress towards the Fed’s policy objectives, providing a lift to the US Dollar over the next few months.

Attractive entry points

The dovish nature of the Fed meeting saw the USD/JPY and AUD/USD approach the bottom and top of their respective ranges, running into support/resistance levels established in the middle of August. USD/JPY tested the psychologically important 100 level while the AUD/USD came near 0.77 which it hasn’t closed above since April. Momentum indicators also suggest the pairs are looking increasingly extended meaning that present levels offer attractive entry points for bullish USD/JPY and bearish AUD/USD positions which would benefit from greater market pricing of a December rate hike.

Investors wishing to express the investment views outlined above may consider using the following ETF Securities ETPs:

For more information contact:

ETF Securities Research team

ETF Securities (UK) Limited

T +44 (0) 207 448 4336

E info@etfsecurities.com

Important Information

The analyses in the above tables are purely for information purposes. They do not reflect the performance of any ETF Securities’ products . The futures and roll returns are not necessarily investable.

General

This communication has been provided by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

This communication is only targeted at qualified or professional investors.

Dogecoin’s performance and staying power across multiple market cycles suggest it is not “just another one of those memecoins”.

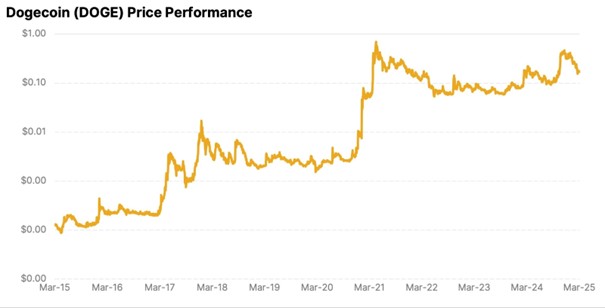

Over the past decade, DOGE has outperformed even Bitcoin, delivering over 133,000% in returns, nearly 1,000x BTC’s gains in the same period. Despite deep drawdowns during bear markets, Dogecoin has shown remarkable structural resilience.

Following each major rally, it has consistently formed higher lows, a pattern of long-term appreciation and compounding strength.

Historically, Dogecoin has closely mirrored Bitcoin’s movements, often peaking a few weeks after. While 2024 saw Bitcoin dominate headlines following landmark ETF approvals, DOGE still followed its trajectory, though it has yet to stage its typical delayed breakout.

As macro uncertainty continues to fade and momentum returns to the market, retail participation is likely to accelerate, setting up conditions in which Dogecoin has historically thrived.

At the same time, regulatory clarity around Dogecoin has improved. The SEC recently confirmed that most memecoins are not considered securities, comparing them to collectibles. Additionally, they clarified that proof-of-work rewards, like those earned from mining DOGE, also fall outside that scope. These developments further legitimize Dogecoin’s role in the ecosystem, potentially setting the stage for its next paw up, especially as it now holds a firm base around $0.17, nearly 3x its pre-rally level before reaching a new all-time high in the last cycle.

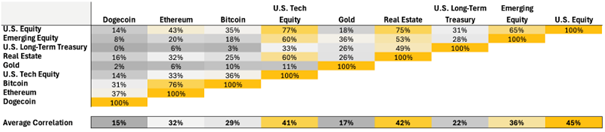

In addition to its long-term performance, Dogecoin stands out as an asset that behaves asymmetrically, offering investors a rare source of uncorrelated returns across both traditional and crypto portfolios. With an average correlation of just 15% to major assets, DOGE’s price action remains largely detached from broader macroeconomic trends, reinforcing its value as a true diversification tool.

Dogecoin demonstrates significant independence within the crypto market, with its correlation to Bitcoin at only 31% and to Ethereum at 37%. This divergence stems from unique capital flow dynamics, where higher-beta assets like DOGE tend to rally after blue-chip crypto assets reach major milestones.

While Bitcoin slowly evolves into a digital store of value and Ethereum powers decentralized infrastructure, Dogecoin remains largely a cultural asset, thriving on narrative momentum and crowd psychology, offering explosive upside when risk appetite surges.

For investors seeking an upside without mirroring the behavior of core holdings, Dogecoin offers a compelling case. Its ability to decouple from market trends while tapping into more speculative surges makes it a powerful, though unconventional, addition to a portfolio with wildcard potential.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Asset Manager ETF-Workshop 2025

Börshandlade produkter som ger exponering mot Sui

The Dogecoin case study: How to value memecoins

MWOA ETF köper aktier i industriföretag

XENIX ETF AWARDS Nordics 2025, Stockholm

Bitcoin var den bäst presterande tillgången men…

Sju börshandlade fonder som investerar i försvarssektorn

Världens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa

HANetfs Tom Bailey om framtiden för europeiska försvarsfonder

-

Nyheter2 dagar sedan

Nyheter2 dagar sedanBitcoin var den bäst presterande tillgången men…

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetfs Tom Bailey om framtiden för europeiska försvarsfonder

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFastställd utdelning i MONTDIV april 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanInvestera i Polen med börshandlade fonder

-

Nyheter5 dagar sedan

Nyheter5 dagar sedanInvesterarna söker fonder som ger exponering mot försvarsindustrin