Nyheter

Är det slut på börsrallyt?

Donald Trump’s return to the White House has forced European leaders to reconsider their defence capabilities. Trump’s administration has stated that it expects European countries to take on a greater role in their own security, as well as giving overt signals that it has less interest in the future of the continent’s security. In a worst-case scenario, there are growing fears about the US’ continued commitment to the NATO alliance. This article will outline the scale of the task ahead for Europe to prepare for a world where it can potentially no longer rely on the US for its security.

Europe alone?

First, it is worth noting that the prospect of a US pullout of NATO remains unlikely. While members of Trump’s cabinet have endorsed a withdrawal, the president himself has not. Key members of Trump’s cabinet such as Secretary of State Marco Rubio appear to remain strong believers in the alliance. Crucially, in 2023, the US Congress passed a law requiring a two-thirds majority vote before any President can withdraw from the alliance. Given the current makeup of Congress, such a vote passing seems unlikely.

However, European leaders are taking the risk seriously. Even if the worst-case scenario of a total US withdrawal from NATO does not come to pass, the prospect can no longer be discounted. At the same time, even if the US continues as a member, there is a growing expectation of Europe to develop its own defence capabilities. There is, therefore, a renewed sense among European leaders that they must develop credible security deterrence in the absence of the US.

What is needed?

A recent analysis by Bruegel and the Kiel Institute for the World Economy provides insights into the measures Europe would need to undertake to deter potential aggression from Russia in the absence of US support. [1]

First, soldiers. Currently, the US has around 100,000 troops stationed on the continent, with NATO military planners assuming an additional 200,000 would be rapidly dispatched to Europe in the event of conflict.

A theoretical absence of US support, therefore, means considering how Europe may replace these 300,000 soldiers. Europe, including the UK, currently has almost 1.5 million active-duty military personnel. In theory, this makes replacing the 300,000 US troops easy enough. However, as analysis by Bruegel notes: “The combat power of 300,000 US troops is substantially greater than the equivalent number of European troops distributed over 29 national armies.”

A crucial weakness of European troops will be fragmentation. A Europe without US support, therefore, is faced with two choices: replace the 300,000 with substantially more soldiers – to offset the fragmented weakness – or rapidly enhance cooperation.

The challenge is also stark when it comes to equipment. The Bruegel analysis claims that preventing a rapid Russian breakthrough in the Baltic states would, at a minimum, require “1,400 tanks, 2,000 infantry fighting vehicles and 700 artillery pieces (155mm howitzers and multiple rocket launchers)”. To put this into perspective, that is more firepower than the French, German, Italian, and British land forces combined. And that is just for providing a credible deterrence in the Baltic states.

European states will also have to invest substantially in developing their own transport, missile, drone, communications, and intelligence capabilities.

Historic underspend

Future-proofing European defence against a potential absence of US support, therefore, is a tremendous task. Achieving anything approaching what is needed to shore up the continent’s defence will cost tremendous sums.

This has been made harder by the underspending on defence among European NATO members over the past few decades. The euphoria of the post-Cold War era saw European governments slash their defence spending. Money that had previously been spent on military security could be reallocated to spending on social security.

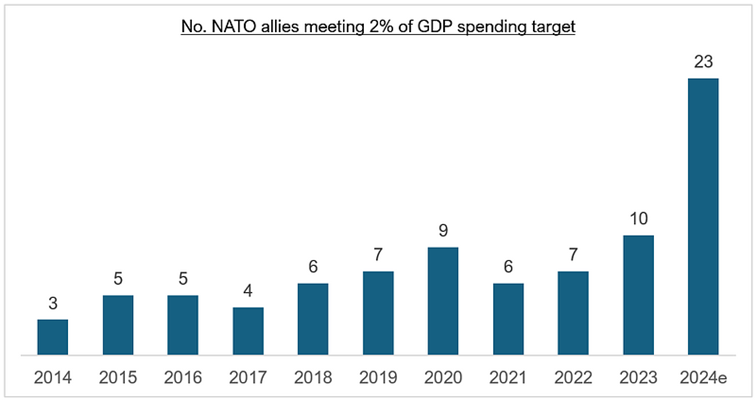

With Russia’s first invasion of Ukraine in 2014, NATO took steps to reverse this, principally by setting a defence spending target of 2% of GDP for members. But very few NATO members actually reached this target. As late as 2021, just 6 members of NATO spent 2% or more on defence.

However, as the graph below shows, the number of NATO members hitting the 2% target has rapidly ramped up, with 23 members now hitting the 2% target.

Source: NATO, June 2024. Data excludes the U.S. For illustrative purposes only. Chart displays expected data.

Yet the historic underspending by Europe leaves a hole in European defence capabilities. Figures from Exante Data shows that the cumulative underspend since 2014, relative to the 2% targets, among European NATO members equals €850bn. [2]

The road to 5%

The task for both readying Europe for defence challenges in a world without US support, as well as addressing the historic underfunding of European defence, will require defence spending rising significantly above 2% of GDP.

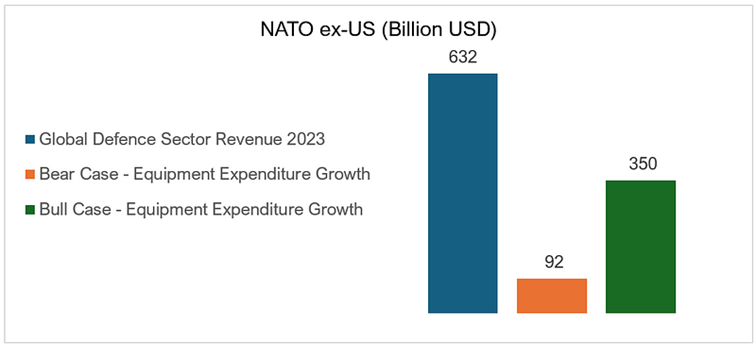

Currently, European (and Canada) NATO members spend, on average, around 2% of GDP on defence. If NATO ex-USA members were to increase defence spending to 5% of GDP, what would this look like? If certain assumptions are made, we can map out the bullish and bearish scenarios for NATO defence spending.

In our bull case scenario, we assume NATO ex-US defence budgets to increase to 5% of GDP by 2029, while assuming equipment spending as % of total NATO budget growing by 1% per year. It also includes assumptions of GDP growth per year standing at 2%.

In this scenario, equipment expenditure would increase by $350billion, over half the total revenue generated by defence companies in 2023.

Meanwhile, in our bear case scenario, equipment expenditure still grows by almost $100billion over the period. This bear case scenario assumes NATO ex-US defence budgets grow to 3.5% by 2029, with equipment expenditure remaining steady as a percentage of defence spending (31.6%) and GDP growth of 1% per year. This would see additional equipment expenditure increase by $92billion.

Source: NATO, HANetf analysis. Charts display projected data. For illustrative purposes only. Additional sources available upon request.

The Future of Defence

While the complete withdrawal of the US from NATO is a hypothetical scenario, these estimates underscore the significant investments and structural changes Europe would need to implement to maintain a credible defence posture independently.

Future of Defence UCITS ETF (ASWC) seeks to provide exposure to the companies generating revenue from NATO and NATO+ ally defence and cyber defence spending. The “NATO screen” seeks to align with the values of investors who may have concerns about defence investing, but cannot ignore the current political climate, and therefore seek a smarter and more considered approach.

NATO is a defensive alliance and itself states that “deterrence and defence is one of its core tasks” – focusing on companies operating in NATO allied countries limits the possibility of constituents of the ETF being companies operating in countries that could one day be adversaries to the alliance.

Key Risks

• Thematic ETFs are exposed to a limited number of sectors and thus the investment will be concentrated and may experience high volatility.

• Investors’ capital is fully at risk and may not get back the amount originally invested.

• Exchange rates can have a positive or negative effect on returns.

• For a complete overview of all the risks, please refer to the “Risk Factors” in the Prospectus.

Handla ASWC ETF

HANetf Future of Defence UCITS ETF (ASWC ETF) är en europeisk börshandlad fond. Denna fond handlas på flera olika börser, till exempel Deutsche Boerse Xetra och London Stock Exchange. Av den anledningen förekommer olika kortnamn på samma börshandlade fond.

Det betyder att det går att handla andelar i denna ETF genom de flesta svenska banker och Internetmäklare, till exempel DEGIRO, Nordnet, SAVR och Avanza.

Krypto-ETN från 21Shares ger tillgång till både Bitcoin och Ethereum

WGRU ETF köper kvalitativa utdelningsaktier

A hypothetical U.S. withdrawal from NATO

FTGA ETF satsar på den globala flygindustrin och försvarssektorn

Virtune XRP ETP når1,1 miljarder kronor i förvaltat kapital

MONTDIV ETF är Sveriges första månadsutdelande ETF

Varför investera i indexfonder?

100 gånger pengarna, aktier som gör 10 000 kronor till 1 miljon

Montrose lanserar Sveriges första månadsutdelande ETF

BlackRock lanserar aktivt förvaltad Fixed Income UCITS ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMONTDIV ETF är Sveriges första månadsutdelande ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVarför investera i indexfonder?

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan100 gånger pengarna, aktier som gör 10 000 kronor till 1 miljon

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMontrose lanserar Sveriges första månadsutdelande ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBlackRock lanserar aktivt förvaltad Fixed Income UCITS ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanInvesterarnas intresse kraftigt förändrat under februari 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSprotts Steve Schoffstall om kärnenergitrender, uranmarknaden och politiska effekter

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanNATO-anpassade Future of Defense ETF når en miljard USD i AUM