Nyheter

What’s next for India’s economic ascent?

Since China’s lacklustre post-COVID reopening, we’ve been asked some form of this question many times—“Is India the next China?”

With its more youthful population, India recently surpassed China as the world’s biggest nation. Its manufacturing and services purchasing managers’ indexes (PMI) have long been in expansion mode as the world’s largest democracy continues to lure investment from foreign tech giants. What’s more, India took big leaps forward in aerospace achievements and diplomatic leadership last year as host of the G20 summit. India has drawn praise for embarking on a path of military modernization and reducing its reliance on Russian defence equipment. And by 2026, about US$534 billion in new infrastructure is expected to be rolled out, equal to the inflation-adjusted value of all infrastructure built over the past 11 years, according to Bloomberg Economics. Earlier this year, India also struck a new trade agreement with the European Free Trade Association (EFTA) to lift tariffs in exchange for US$100 billion in foreign direct investment commitments. The EFTA accord is expected to generate 1 million jobs in India over the next decade and a half.

Few would disagree that India is benefiting from China’s slowdown. But especially now that the dust has settled over Prime Minister Narendra Modi’s electoral setback, we believe the political outcome underpins the view that this noisy democracy is distinctly different.

Rather than splintering, several opposition parties united during general elections in what amounted to an anti-BJP (Bharatiya Janata Party) vote that presented hurdles for Modi even as the untested new coalition government could still prove fractious and unstable. Despite difference in political ideology, we believe all sides are committed to the same underlying objective of advancing India’s economy, and to some extent the infighting amounts to jockeying for credit over positive outcomes. Nevertheless, the divided power structure arguably bodes well for the country’s consensus-building process—a positive in our view.

We remain optimistic that policy reforms already in place set a strong foundation for export growth and the ongoing rise of a new class of Indian consumers. Certain sectors like energy and defence also tend to be less sensitive to partisan issues, and India remains a trusted value-chain partner for electronic device and chip manufacturers.

Consider that India’s equity market recouped post-election losses of nearly 6% for the S&P CNX Nifty Index at the fastest rate in recent history—over merely three sessions. The rebound reflects unwavering confidence among domestic retail investors. The country’s retail inflation also edged lower in May to 4.75%, down from 4.83% in April, aided in part by lower fuel prices despite continued elevated food prices, according to new government data.

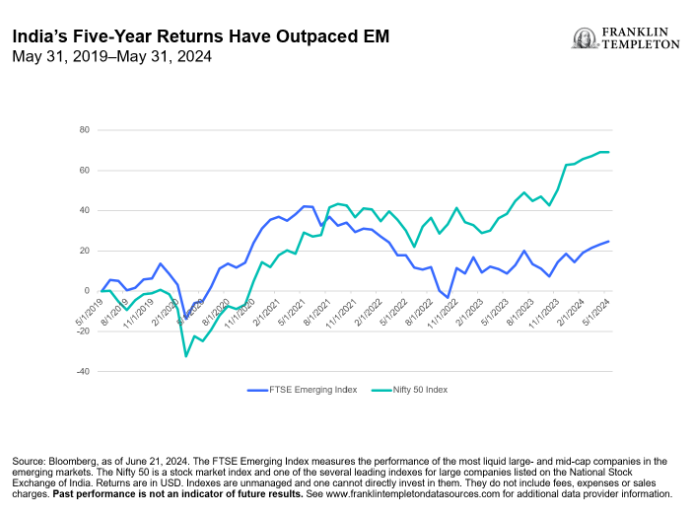

In January this year, the Indian stock exchange even overtook that of Hong Kong’s in capitalization (US$4.3 trillion versus US$4.29 trillion), reflecting India’s exceptional 2023 performance. This year, the Nifty 100 Index is up 12.7% year-to-date through June 20, compared to 9.3% for FTSE Emerging Index over the same period (returns are in USD).

Most broad emerging market (EM) benchmarks are still heavily weighted toward China, though solid performance among Indian equities has been closing this gap. A case in point for India’s rising prominence in EM: In May, MSCI boosted India’s weighting in its Emerging Market Index to nearly 19%, up from roughly 9% in 2020.

Investors seeking more targeted exposure to India may find single country exchange-traded funds to be compelling low-cost building blocks for asset allocation. For those wanting to tap exposure to India’s attractive mid-cap segment, keep in mind that some indexes offer a deeper portfolio compared to others.

India’s equity markets are also well-diversified across sectors and company types that potentially offer an elevated growth outlook and opportunities driven by domestic consumption and emerging industrial prowess. Financials hold the largest share, followed by significant consumer discretionary, industrial, energy and technology weightings. The market also offers good exposure to consumer staples, utilities and health care names.

As India’s gross domestic product (GDP) is forecast to increase at an average of 6.5% annually over the next five years, we feel optimistic that this diverse and dynamic economy can potentially realize a multi-decade growth story, perhaps with even hardier democratic checks in place.