Nyheter

Tether Cornered in NYC Court, Helium Moving to Solana, and More!

Markets performed better than last week, despite the biggest cryptoassets still in capitulation zone. Bitcoin declined by almost 2% over the past week, while Ethereum grew its total value locked (TVL) by 3%. As shown in Figure 1, the three winners of the major categories in the cryptoassets industry were Solana and Metis, jumping by 6%, 5.5%, while Curve grew its TVL by a whopping 13.6%.

Figure 1: TVL and price development of major crypto sectors

Source: 21Shares, Coingecko, DeFi Llama

Key takeaways

• New York judge ordered Tether to provide proof of USDT’s backing

• Cardano’s most recent upgrade is triggered, Polygon streamlining supernet development.

• Stablecoins carry on proliferating across chains.

• Decentraland will introduce mintable NFT “Emotes” at Metaverse Music Festival

Spot and Derivatives Markets

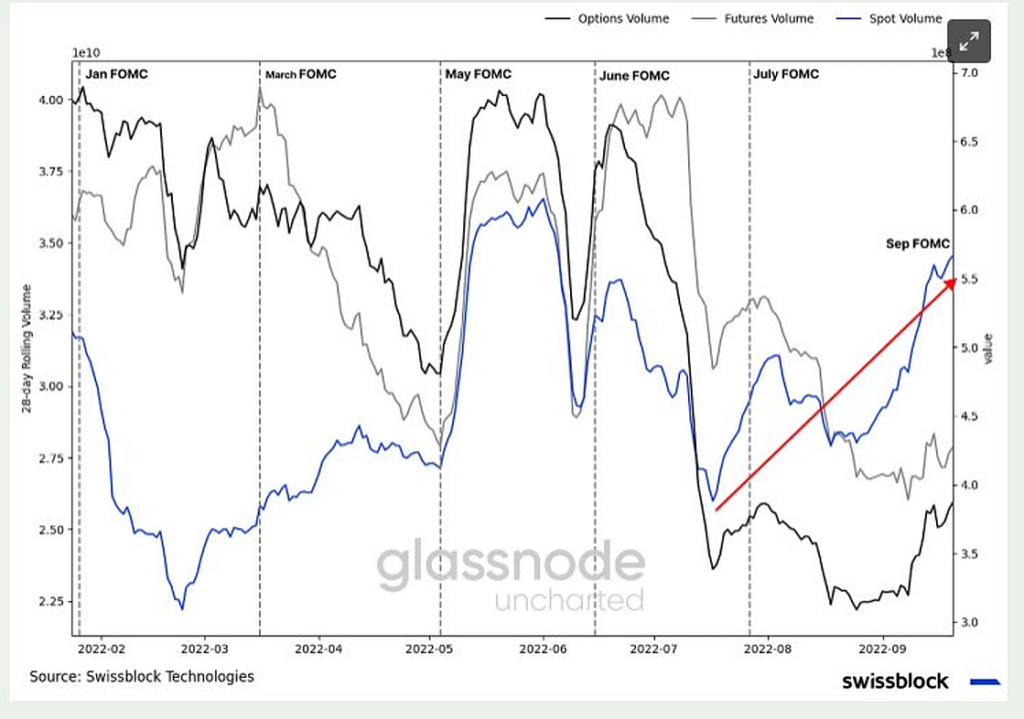

Figure 2:

Source: Glassnode, Swissblock Technologies

The figure above plots this year’s meetings of the Federal Open Market Committee (FOMC) against spot and derivatives 28-day rolling volume. The chart reveals that Bitcoin is under-levered for the first time this year, which in itself is a sign of true capitulation.

On-chain Indicators

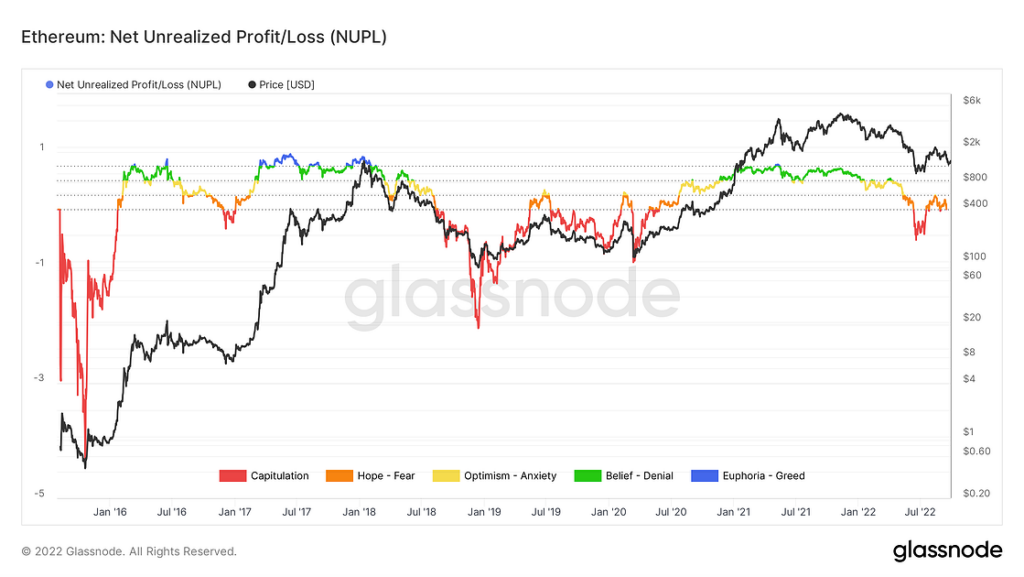

Figure 3: Ethereum’s NUPL ratio

Source: Glassnode

Ethereum’s NUPL ratio is currently at -0.09, which means that the second-largest cryptoasset by market capitalization is still at the capitulation zone. The current level is similar to levels seen in December 2016 when ETH was at $8.4, with a market cap of $626M, a few months before it jumped within the belief and euphoria levels for a little over a year.

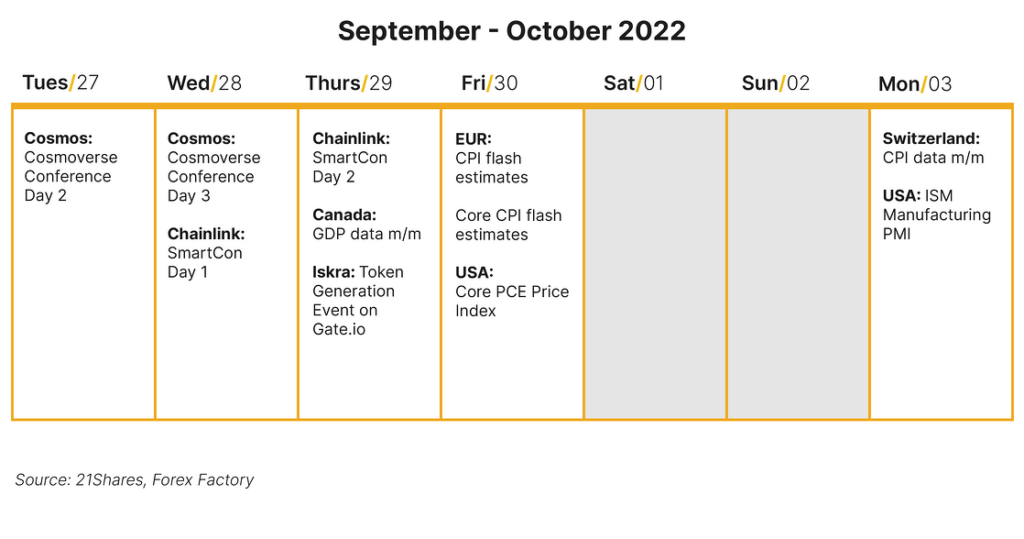

Next Week’s Calendar

Read full report here

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.