Nyheter

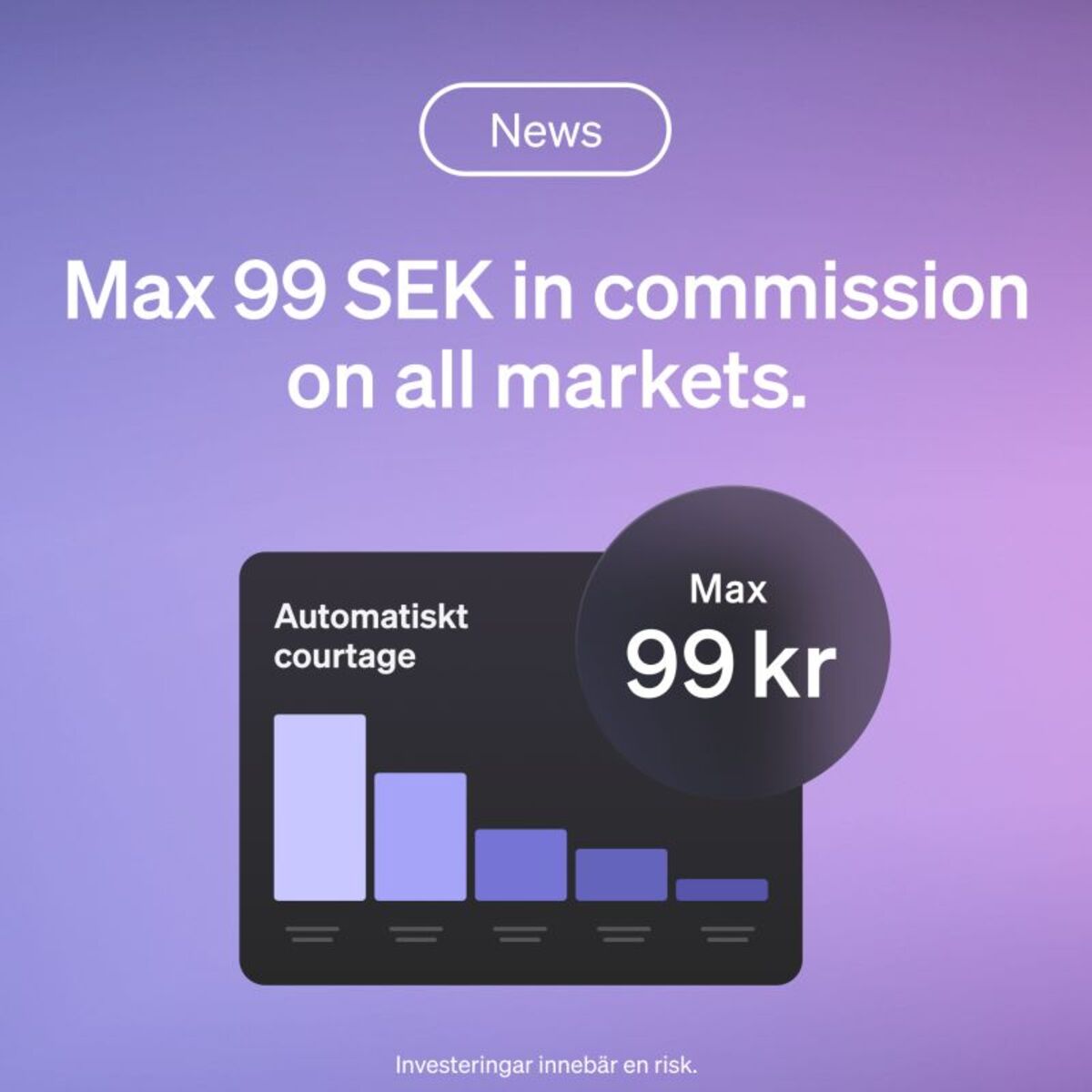

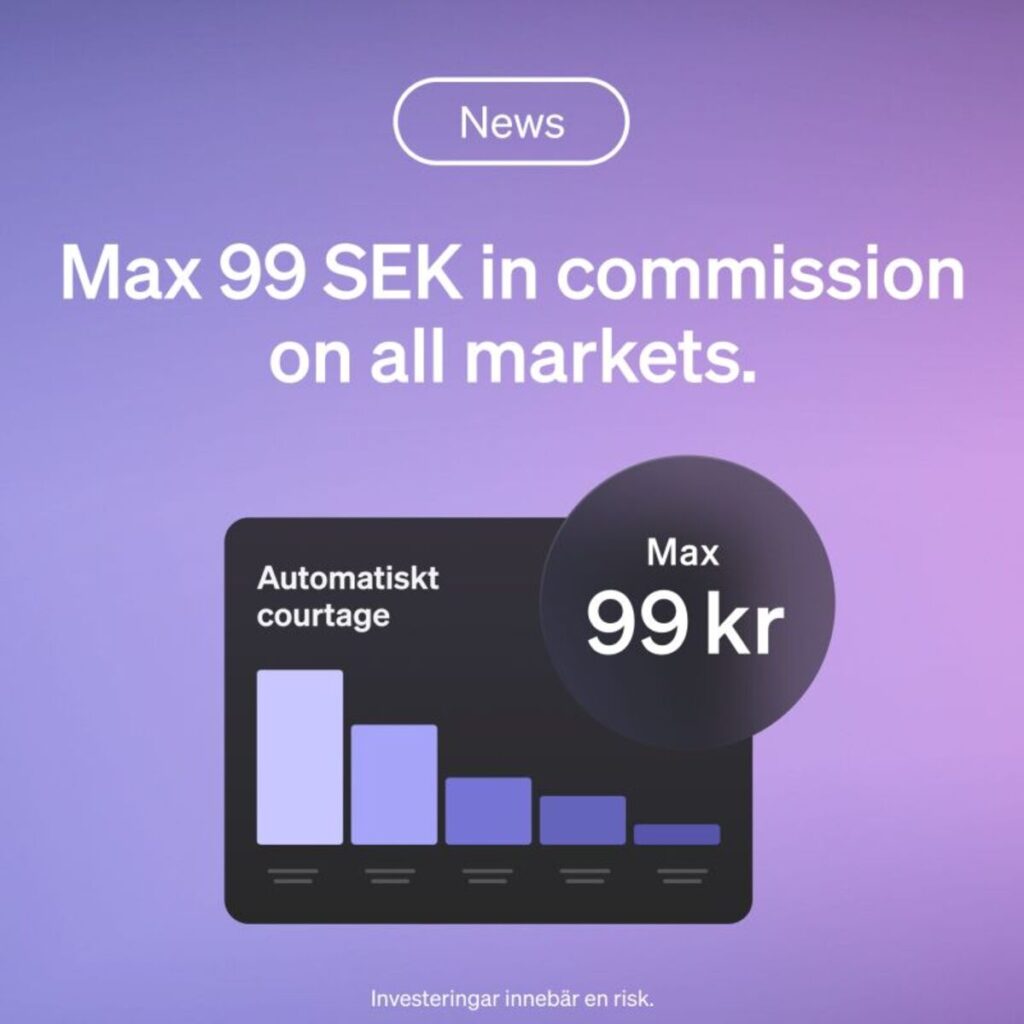

SAVR inför maxcourtage på 99 kronor

Internetmäklaren SAVR kickar igång veckan med några fantastiska nyheter: SAVR introducerar ett tak för det courtage deras kunder betalar som ligger på låga 99 kronor, något som gäller samtliga marknader. Flera konkurrenter har maxcourtage sedan tidigare, men det är begränsat till Norden.

Med andra ord ligger det courtage som kunder på SAVR betalar alltid mellan 1 och 99 kronor– oavsett vilken marknad du handlar på.

Huvudsakliga USP är

- 99kr max för alla marknader (konkurrenterba har bara ”fast pris” för Norden)

- Maxcourtage gäller samtliga aktiemarknader som SAVR erbjuder handel på – och så klart ETFer.

- Justerar automatiskt om du gör mindre transaktioner (då blir det en %), så du löper ingen risk att betala 99kr för en 1000kr transaktion (”automatiskt courtage”). Det finns alltså inte courtageklasser att hålla reda på hos SAVR.

Nyheter

VettaFi lyfter fram stabiliteten i midstreamsektorn mitt i oljevolatiliteten och tillväxten inom naturgas

Investera i vatten med en ETF

BE28 ETF ger exponering mot företagsobligationer med förfall 2028

VettaFi lyfter fram stabiliteten i midstreamsektorn mitt i oljevolatiliteten och tillväxten inom naturgas

NXTE ETP spårar priset på kryptovalutan Ethereum

Q2 2025 Outlook: In the Middle of the 3% Reckoning

Fonder som ger exponering mot försvarsindustrin

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Warren Buffetts råd om vad man ska göra när börsen kraschar

Svenskarna har en ny favorit-ETF

De bästa börshandlade fonderna för tyska utdelningsaktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa börshandlade fonderna för tyska utdelningsaktier

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf lanserar Europa-fokuserad försvars-ETF

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanMONTLEV, Sveriges första globala ETF med hävstång