Nyheter

Regulatory Wins and the Quest for Simplifying Crypto’s Complexity

• A more aggressive rate cut would likely alarm markets, signaling recession risks.

• Crypto regulation is advancing, with U.S. regulators regretting the confusion around ”cryptoasset securities.”

• The UK is moving toward recognizing cryptoassets as personal property, offering stronger legal protections in cases of fraud, theft, and bankruptcy.

• Rebranded Upgrades Season:

o Polygon’s migration from MATIC to POL aims to enhance multichain interoperability and boost investor interest, driving a 15% price jump for POL.

o Maker is transitioning from MKR to SKY, introducing new governance features and rewards, signaling a major shift in the protocol’s operation and community control.

• Multiple new approaches are being adopted to simplify crypto’s fragmented user experience:

o Socket network: offers an auction orderflow marketplaces that allows existing stakeholders to fulfill users desires, disregarding the targeted networks, rather than solving for native interoperability.

o Rabby Wallet: New Update allows one of the leading EVM-wallet users to pay with USDC as a gas currency.

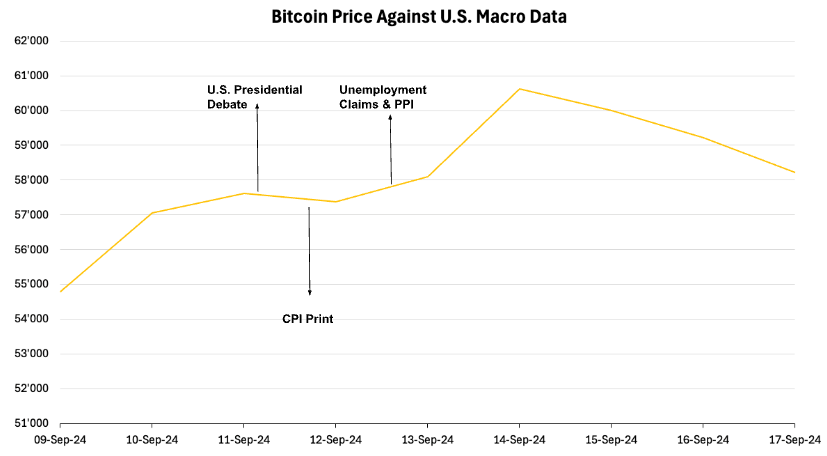

Figure 1 – Bitcoin’s Price Against U.S. Macro Data

Source: Coingecko, 21Shares

Welcome to arguably the most anticipated week since July 2023, when the Federal Reserve raised interest rates one last time to reach the highest point since 2001. Nevertheless, there is so much more to unpack this week, let’s dig in.

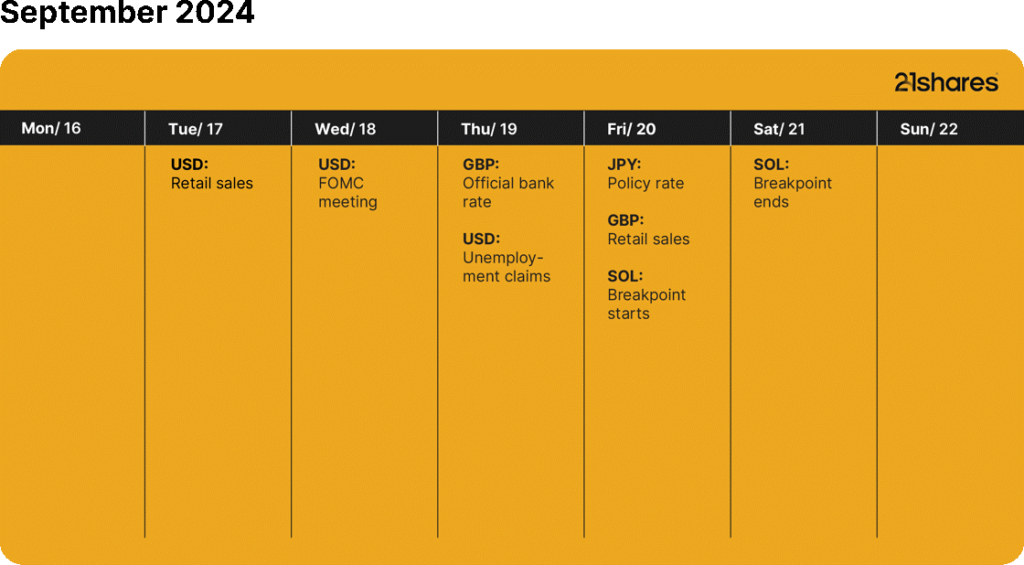

Rate cuts: U.S. annual inflation met expectations at 2.5%, down from 2.9%. Core inflation, which excludes volatile food and energy prices, rose 0.3% monthly, exceeding forecasts. The Federal Open Market Committee (FOMC), meeting on Wednesday, typically focuses on core data. Aside from inflation, the Fed is also expected to consider labor market data, which saw slightly more people file for unemployment claims than expected. However, retail sales outperformed, indicating robust consumer spending, giving a healthier picture of the U.S. economy.

At the time of writing, the CME FedWatch tool predicts a 63% chance of a 50 bps rate cut, contrary to recent sentiment. A larger cut might signal greater fears of a recession, potentially impacting risk assets in the short term. However, this doesn’t alter Bitcoin’s fundamental long-term outlook. Further economic weakening could lead to Fed balance sheet expansion, historically boosting Bitcoin demand.

In the lead up to the FOMC meeting, crypto celebrated a few regulatory wins last week.

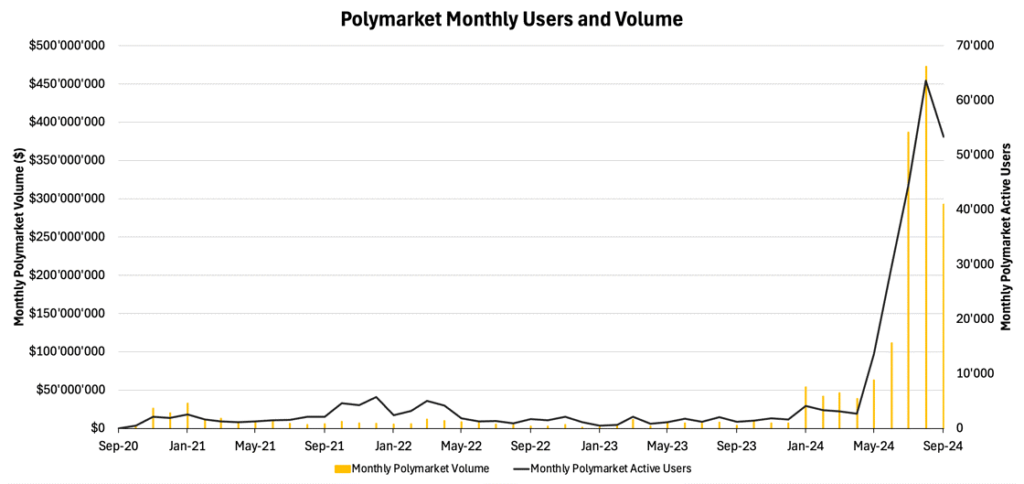

Prediction markets receive an initial nod: Polygon-based Polymarket has been gaining traction for its U.S. elections betting venue, attracting over 60K monthly active users, making more than $450M in trading volume, as shown below in Figure 2. In parallel, prediction markets have drawn some legal concerns in the traditional world.

The Commodity Futures Trading Commission (CFTC) said that prediction markets are vulnerable to manipulation. On September 6, the agency filed a motion to shut down the election betting markets offered by Kalshi, an exchange and prediction market that launched in July 2021. A DC judge released an opinion on September 12, essentially allowing betting platform Kalshi to compete with Polymarket which had been pushed to pursue its operations off-shore after paying a $1.2-million fine in 2022.

Figure 2 – Polymarket Monthly Users and Volume

Source: Dune Analytics

Why does this matter? Essentially, the ruling could clear the pathway for a crypto-native protocol to participate in the U.S. political sphere, thus potentially allowing one of crypto’s dominant applications to play a bigger role outside the boundaries of the web3 industry. In line with this, diversifying blockchain utility is as crucial as portfolio diversification. Expanding use cases attracts a broader user base beyond traditional Web3 enthusiasts. For example, Polymarkets has seen consistent user growth since May, bucking the trend of overall market decline. This highlights the demand for blockchain applications that transcend crypto’s typical boundaries.

SEC’s change of heart? In a recent settlement agreement with the SEC, crypto exchange eToro agreed to de-platform all cryptoassets except for BTC, Bitcoin Cash, and ETH, essentially claiming everything else was a security. More importantly, the SEC announced its “regrets [for] any confusion [the term crypto asset securities] may have invited” in a footnote of another filing attached to the agency’s lawsuit against Binance.

Although the aforementioned instances do not count as a reversal of the agency’s previous position, they still indicate a willingness to reconsider its approach to crypto regulation. This could spark the beginning of a more industry-specific regulatory framework in the future and alleviate some of the uncertainty surrounding the overall market. This could push pending bills to the finish line, one prime example is the Financial Innovation and Technology for the 21st Century Act that passed by the House of Financial Services Committee in May 2024, with “overwhelming” bipartisan support.

Check out our Monthly Wrap for May 2024, where we broke down what this act would mean for the cryptoassets industry, replacing the four-pronged Howey Test with five conditions for a decentralized system.

Crypto as a personal property: The UK government introduced the Property (Digital Assets etc.) Bill before the Parliament on September 11, legally recognizing cryptoassets and non-fungible tokens as personal property. Although this move comes as part of a wider trend to turn the UK into a crypto hub, this bill wants to specifically tackle owner protection. Legal protections would include:

• Rights in disputes and instances of improper interference; legal mechanisms like freezing injunctions could be applied to digital assets.

• Incorporation in bankruptcy and insolvency processes; digital assets could be included in estates that may be liquidated to settle debts with creditors.

• Legal measures can be taken in cases of fraud and theft.

We saw the first implementation of this bill a day after its introduction, when a UK High Court ruled USDT as personal property in the case of a plaintiff who claimed that he was defrauded of over £2.5M ($3.3M) in cryptocurrency, including USDT. This is a meaningful step forward to achieving crypto’s mass adoption, with more clarity being offered around its status under different jurisdictions.

The Era of Rebranded Upgrades: Cutting-Edge Improvements or a Corporate Ploy to Drive Interest?

As the crypto landscape continues to mature, several high-profile networks are executing significant upgrades to enhance scalability, security, and token utility. One of the most pivotal transformations is Polygon’s migration from MATIC to POL, a cornerstone of Polygon 2.0, aimed at evolving the network into a multi-chain ecosystem. Alongside this, Maker is also undergoing major transitions—highlighting a broader trend of protocol upgrades that could redefine these platforms’ value propositions. It could spark renewed investor interest as these corporate moves reignite attention on the network.

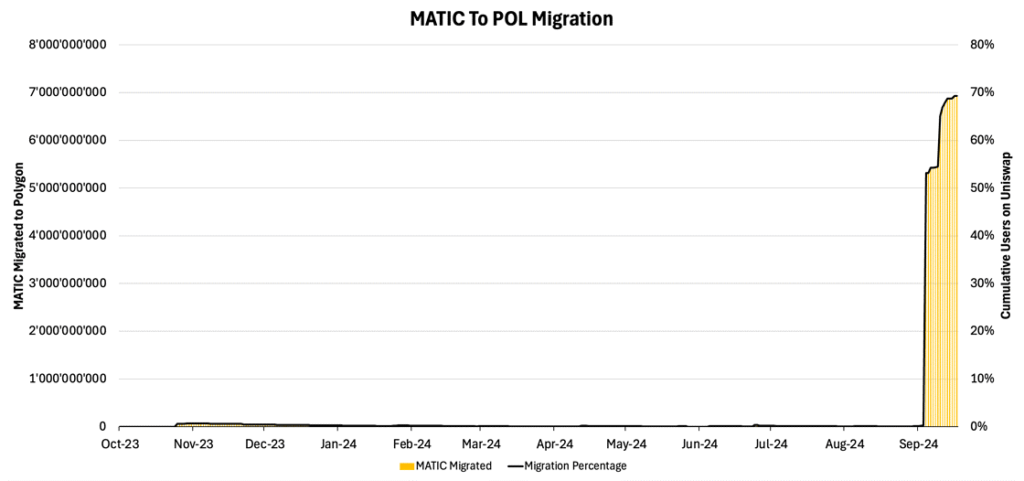

Polygon’s MATIC → POL Migration: The Shift to Multichain Interoperability

On September 4, the Polygon network witnessed a major leap in its MATIC to POL migration. Prior to this date, less than 1% of MATIC had been converted to POL. However, as all MATIC tokens on Polygon PoS automatically migrated to POL, the upgrade rate surged and is currently almost at 70%, as shown below.

Figure 3 – MATIC to POL Migration

Source: Dune Analytics

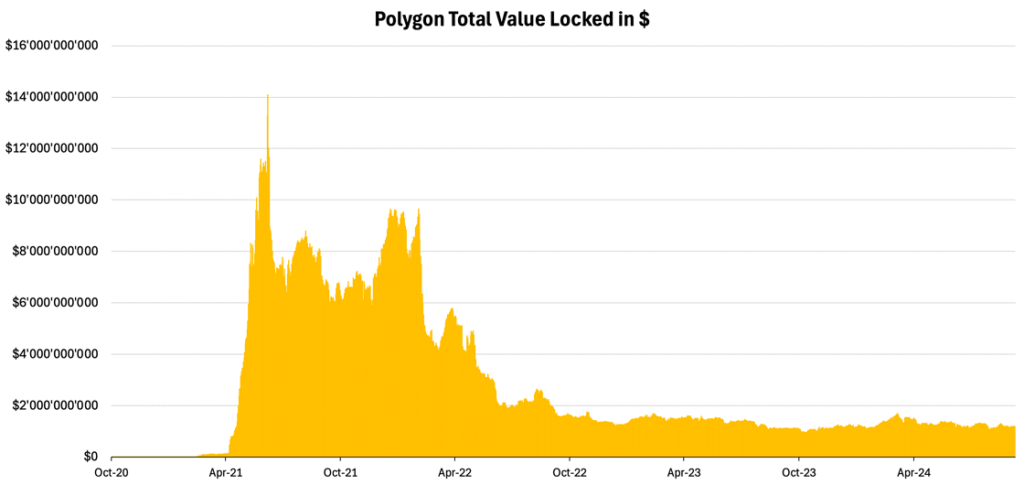

This shift was accelerated by key exchanges like Binance completing their migration last week. POL’s listing triggered a 15% price jump in POL, underscoring the market’s response to this upgrade. The migration not only brings technical advancements to the network but also serves as a catalyst for investor’s interest. In that view, the migration has the potential to spotlight Polygon’s role and revitalize the chain after a period of slow growth, where Total Value Locked (TVL) has not grown since the start of 2023, as shown below.

Figure 4 – Polygon Total Value Locked (TVL)

Source: DeFiLlama

The POL token represents more than just a new name for MATIC—unlocking a range of enhanced features aimed at improving the utility and scalability of the entire Polygon ecosystem. Here are the key takeaways:

• Expand the role of POL as a hyper-productive token securing the entire Polygon-based ecosystem, not just Polygon POS. This should amplify the demand for POL as it becomes increasingly vital for securing the entire ecosystem while increasing revenue share for Polygon’s validators

• Enhance Interoperability: by Introducing the AggLayer which offers a unifying and trust-minimized framework for sharing liquidity across the Polygon Ecosystem

For a deeper understanding of what this upgrade means to the Polygon ecosystem, check out this previous breakdown.

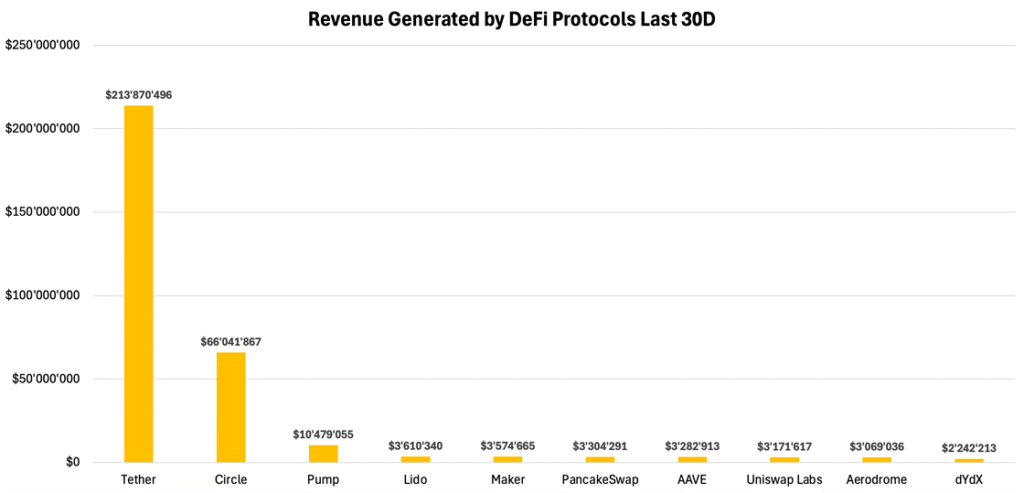

Similarly, Maker, one of the largest DeFi protocols by revenue generation, as shown below, is set to initiate its long-awaited migration from MKR to SKY this Wednesday. This marks a key milestone in the launch of the Sky Protocol, which also includes the introduction of the SKY governance token and the USDS stablecoin.

Much like Polygon’s transition, this upgrade represents a significant shift in how Maker operates and is part of its broader rebranding. The migration will begin on September 18, giving MKR holders the option to convert their MKR tokens to SKY at a rate of 1 MKR to 24,000 SKY. Both tokens—MKR and SKY—will coexist for the foreseeable future, meaning users can choose whether to upgrade or continue holding MKR. Importantly, no definitive sunset date for MKR has been announced, allowing flexibility for token holders. With SKY set to become the primary governance token, the upgrade introduces advanced governance features intended to increase community participation and give the community greater control over the protocol’s future direction.

Figure 5 – Revenue Generated by DeFi Protocols

Source: DeFiLlama

What we know so far is that the SKY token will bring several notable features and mechanisms that could strengthen Maker’s governance and reward structure. Here are the key enhancements:

• Elevated Token Rewards: SKY introduces a 600M annual SKY token reward pool for participants holding USDS, the upgraded stablecoin replacing DAI.

• Sealed Activation and Regular Activation: SKY holders can choose between Sealed Activation, which involves committing governance tokens for a longer term in exchange for higher rewards (primarily in USDS), and Regular Activation, which allows users to stake tokens without a lock-up period. These features are designed to encourage long-term governance participation and ecosystem stability.

• Introduction of Stars (Formerly SubDAOs): Maker’s governance will be divided into smaller, decentralized units called Stars. These units will allow for more specialized governance, enabling the protocol to scale more effectively while enhancing decision-making within specific areas of the ecosystem.

• Enhanced Stablecoin (USDS): DAI holders can upgrade to USDS at a 1:1 ratio, unlocking access to SKY token rewards. USDS also includes additional features, such as the Savings Rate, which has been a core part of Maker’s lending system for over seven years.

Considering that Maker’s upgrade is quite significant, stay on hold for a dedicated report into what the upgrade means, the remaining questions that still need to be resolved to fully comprehend its potential impact.

All in all, the Maker and Polygon migrations are part of a broader trend in the crypto space as major networks undergo significant corporate actions to remain competitive. Just as Polygon has shifted to a multichain structure with POL to reinvigorate its ecosystem, Maker is embarking on a journey to redefine governance and rewards with SKY.

Abstracting Crypto’s Complexity

One of the hurdles slowing crypto’s adoption is the absence of a user-intuitive experience. For example, there are more than 380 networks across the smart-contract platforms (alternative L1s) and scaling solutions (L2s) built on top of Ethereum, which results in a daunting maze for newcomers.

On the L1 level, fragmentation creates significant user challenges. Managing multiple wallets with diverse seed phrases and transaction methods is cumbersome. The need for crypto forex services (bridging solutions) across +300 networks further complicates asset transfers. Additionally, users must juggle various native gas tokens (e.g., ETH, AVAX, POL) for transacting on different blockchains.

Alternatively, across the L2 vertical, interoperability persists as the prime challenge. Despite Ethereum-based scaling solutions sharing a common settlement layer, thus users can leverage the same wallet (Metamask), each network’s unique approach to scaling creates barriers for cross chain transfers. This diversity hinders the development of a universal forex exchange that could seamlessly connect the +80 L2 networks.

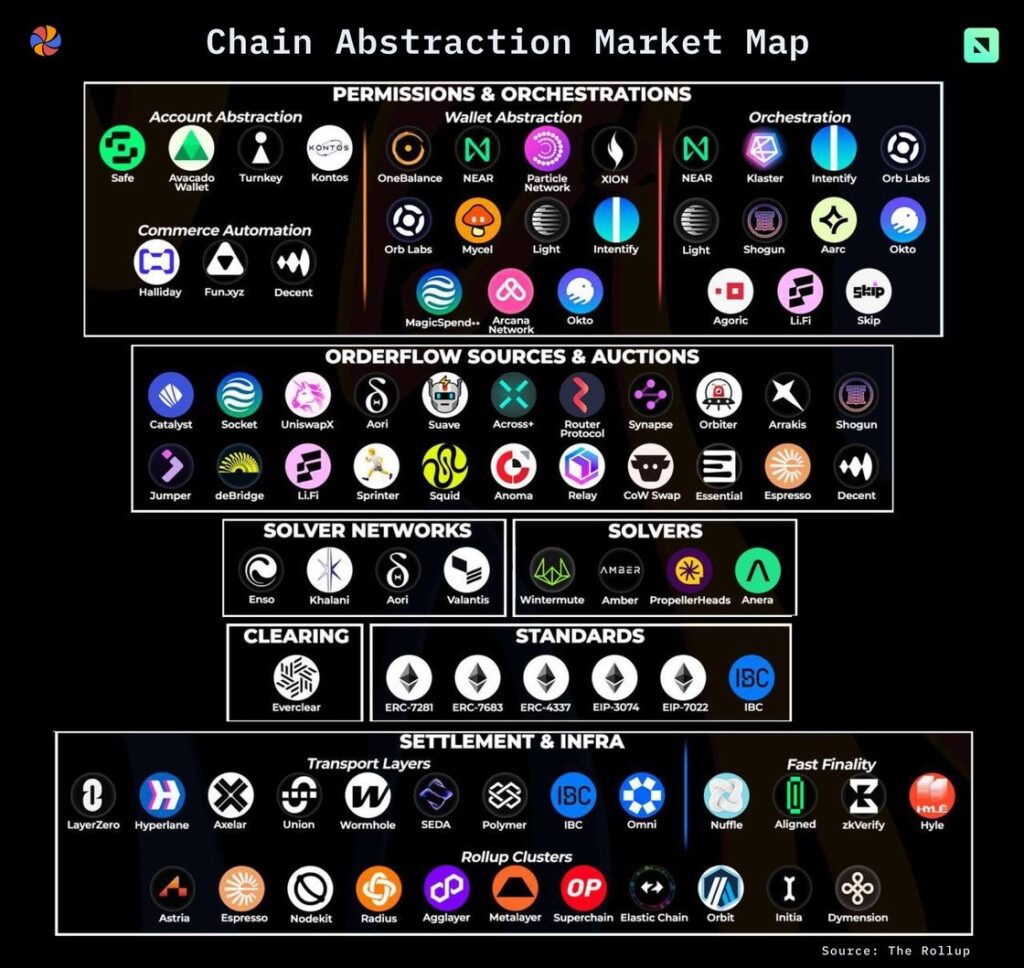

Given this extent of fragmentation, it’s crucial to examine the different interoperability approaches. While chain abstraction is a broad topic deserving its own analysis, this report will focus specifically on account and wallet abstraction as key strategies to enhance user experience.

Figure 6 – Mapping of the Crypto’s Modularity Industry

Source: OurNetwork

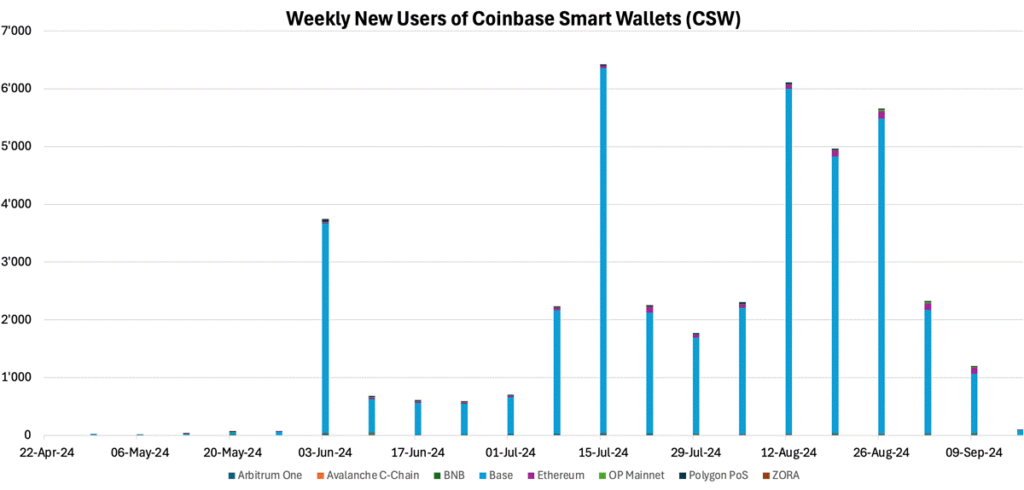

On one side, Account Abstraction refers to the ability to customize blockchain accounts and make them smarter. In this regard, Ethereum’s Pectra upgrade will be one of the key milestones to enable this functionality on the network level, thus making it easier to create smarter wallets. That said, with Coinbase’s smart wallet being the first major adopter of the ERC-4337, its growth has been impressive so far, onboarding a total cumulative number of ~37K users, as seen in Figure 7.

Figure 7 – Weekly New Users of Coinbase Smart Wallets (CSW)

Source: Dune Analytics

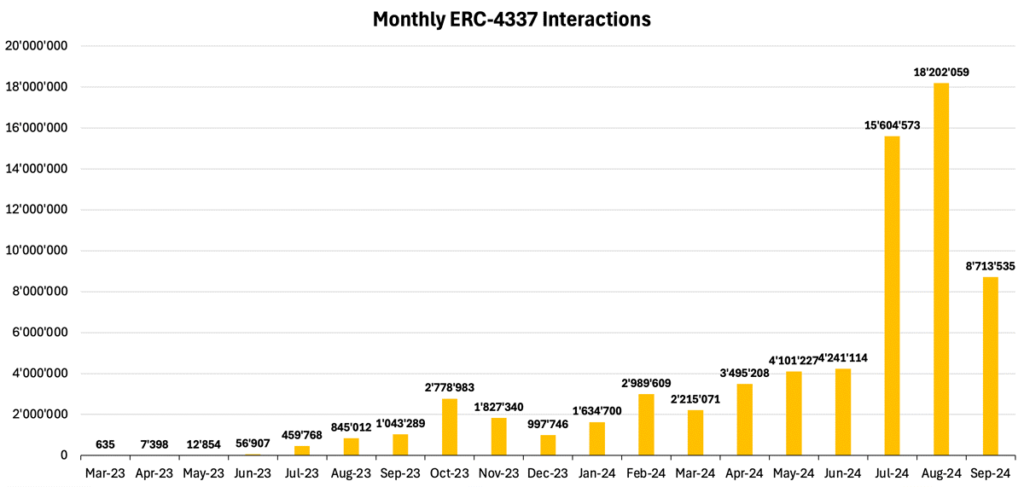

However, we expect the standard’s adoption to accelerate significantly after the activation of the Ethereum Pectra upgrade. Nevertheless, it is worth noting that this trend is gaining significant momentum, as illustrated in Figure 8 below.

Figure 8 – Monthly ERC-4337 (AA) Interactions

Source: Dune Analytics

Alternatively, Socket Network, an interoperability-focused infrastructure provider, offers an innovative solution to cross-chain challenges through its Modular Order Flow Auction (MOFA) protocol. In that, Socket creates a competitive marketplace where execution agents (validators and sequencers) bid to fulfill cross-network user-requests. This system employs chain-abstracted bundles, streamlining multi-network transactions and eliminating the need for users to directly interact with different networks. Socket’s approach offers advantages to both users and existing stakeholders, positioning it as a noteworthy alternative to Coinbase’s solution in addressing cross-chain interoperability.

- Users: Enjoy improved execution and a simplified experience across fragmented crypto infrastructure.

- Stakeholders (sequencers, validators, market makers): Gain expanded roles and increased fee-earning opportunities within the ecosystem.

While related, wallet abstraction focuses on enhancing the user interface itself, simplifying wallet creation and management through familiar web2 credentials, and streamlining cross-blockchain interactions. In essence, account abstraction implements protocol-level changes, whereas wallet abstraction improves the application-level experience.

Rabby Wallet, one of the leading wallet providers, exemplifies this trend with its new gas abstraction feature. This innovation allows users to deposit USDC or USDT into a dedicated gas account, enabling them to pay transaction fees across multiple supported networks using these stablecoins. While this optimized transaction method may incur slightly higher costs due to multiple asset transfers, the added convenience likely outweighs the premium for most users.

In conclusion, the ongoing efforts to simplify crypto’s complexities are vital for attracting new users. To achieve mainstream adoption, the crypto experience should mirror the user-friendly nature of Web 2.0, eliminating the need for users to grapple with technical concepts like gas fees, seed phrases, or cross-network transfers. These initiatives aim to transform crypto interactions into a seamless, familiar web experience, paving the way for broader acceptance and usage.

What’s happening this week?

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Nyheter

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

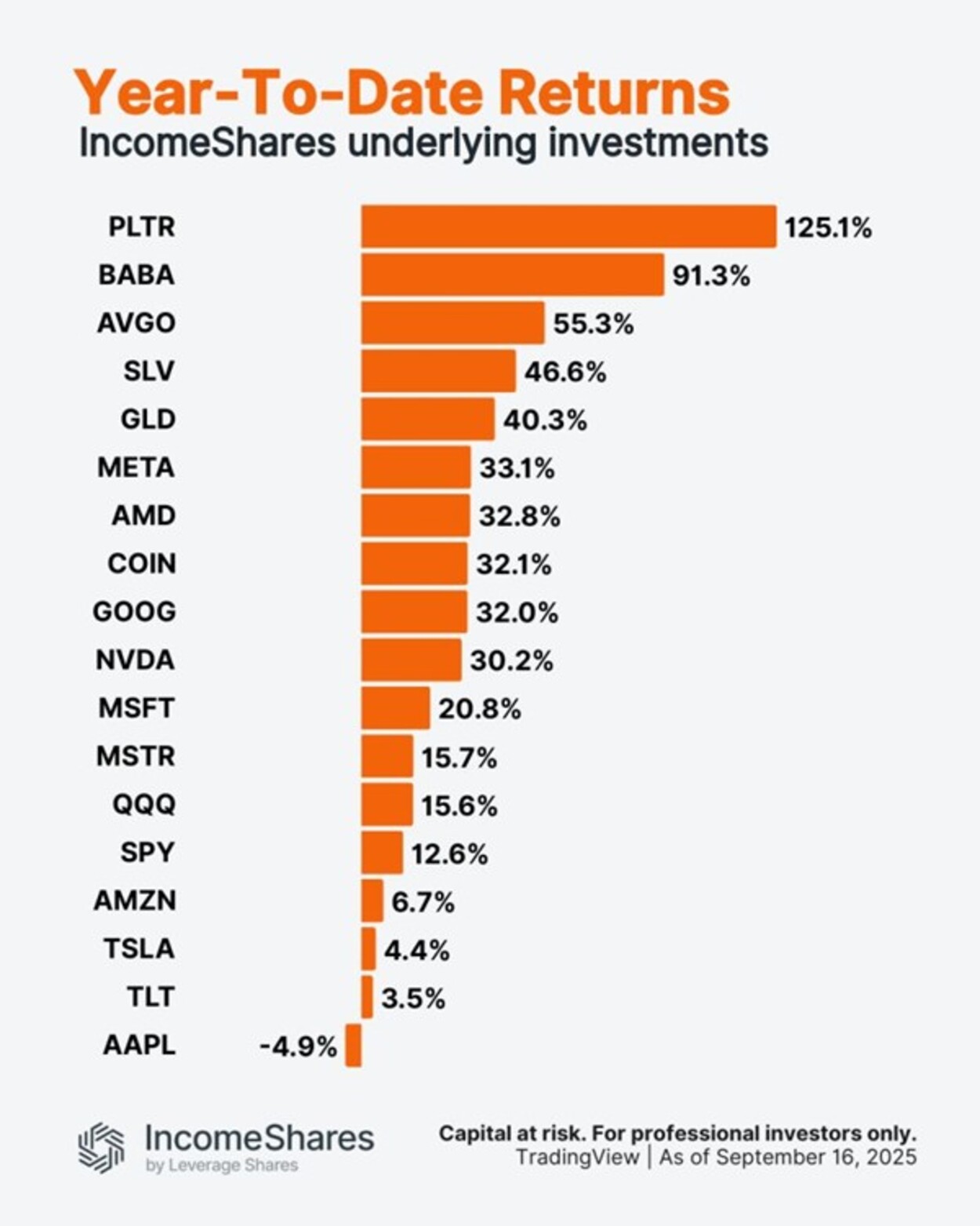

Palantir är upp 125 % i år. Apple är ner 5 %.

Utforska framtiden för AI och DeFi

ONCC ETP spårar den schweiziska dagslåneräntan

HANetf kommenterar kopparuppgången

Utdelningar och försvarsfonder lockade i augusti

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

ADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

Septembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSeptembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV augusti 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf kommenterar mötet mellan Kina, Ryssland och Nordkorea vid militärparad

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAICT ETF investerar i obligationer utgivna av företag från tillväxtmarknader