Nyheter

Rate Cuts and Bitcoin’s Scaling Potential: What Happened in Crypto This Week?

• Exciting Future for Bitcoin’s Scaling Potential

• BTC’s Rising Accumulation Meets a Growing Delta-Neutral Trading Strategy

• Rooting for Rate Cuts, Banking Crisis Looms in the U.S.

Rooting for Rate Cuts, Banking Crisis Looms in the U.S.

Benchmarks of monetary policy success are shifting around the world. The 2% inflation rate target is no longer within reach in the immediate term, while high interest rates seem to be doing more harm than good. On June 5, Canada was the first G7 country to lower its interest rate to 4.75% from the 5% it stuck to since July 2023. Despite its two-year high unemployment rate of 6.1% and an inflation rate of 2.7% in April, Canada’s move might have started the rate cut season.

Now, while Europe’s inflation has improved over the past six months, inching towards the 2% medium-term target, the European Central Bank (ECB) might have followed suit. For the first time since 2019, the ECB lowered interest rates to 25 basis points. Starting June 12, the EU’s key interest rate will be reduced to 3.75% from 4%, where it has been since September 2023. Realizing the 2% target is far from reach, European monetary policy seems to factor in a more realistic dimension. The ECB staff added 20 basis points to their annual inflation forecasts to be 2.5% in 2024 and 2.2% in 2025.

At the same time that 20 European countries will be celebrating the long-awaited rate cut, the U.S. will be rooting for a cool Consumer Price Index (CPI) print that would boost the Federal Reserve’s confidence that inflation is heading in the right direction. However, the labor market is showing mixed signs of recovery in May, with the unemployment rate increasing slightly above expectations at 4%. In contrast, nonfarm payroll employment increased to 272K, 50K higher than the monthly average. Average monthly earnings have also inched up from April’s reading, increasing by 0.4%. As seen, the delicate balance between inflation control and economic growth remains uncertain, which would definitely be reflected in the Federal Reserve policy decisions. Thus, crypto will remain sensitive to the different interpretations of macro data.

Specifically, volatility will be expected this week in anticipation of the Federal Open Market Committee statement scheduled to shed some light on the U.S. monetary policy on June 12. However, more macro data is coming out later in the week. As shown in the calendar at the end of this newsletter, we’ll know more about changes in wholesale prices on Thursday and conclude the week with the University of Michigan survey results around consumer sentiment, which should give a more complete picture of where the economy stands.

Moreover, the higher-for-longer approach is straining the banking sector in the U.S., with 63 banks declared to be sitting on $517B in unrealized losses, increasing by $39B in the first quarter. Higher unrealized losses on residential mortgage-backed securities, resulting from higher mortgage rates in the first quarter, drove the overall increase. This is the ninth straight quarter of unusually high unrealized losses since 2022, when the Federal Reserve began raising interest rates.

How will this developing crisis affect BTC? Bitcoin usually stood strong amid banking crises, acting as a hedge against counterparty failure over the past few years. That was evident in March 2023, when Bitcoin jumped by 30% after the world experienced the most significant banking stress since 2008. Lack of transparency, mismanagement, and vulnerability towards a single point of failure led to the collapse of hundreds of banks between 2007 and 2012. These factors led to what is now known as the Great Recession, inspiring the creation of Bitcoin in the process. The network’s disciplined monetary policy, combined with its immutable nature and decentralization, became the antithesis of the failures of traditional finance.

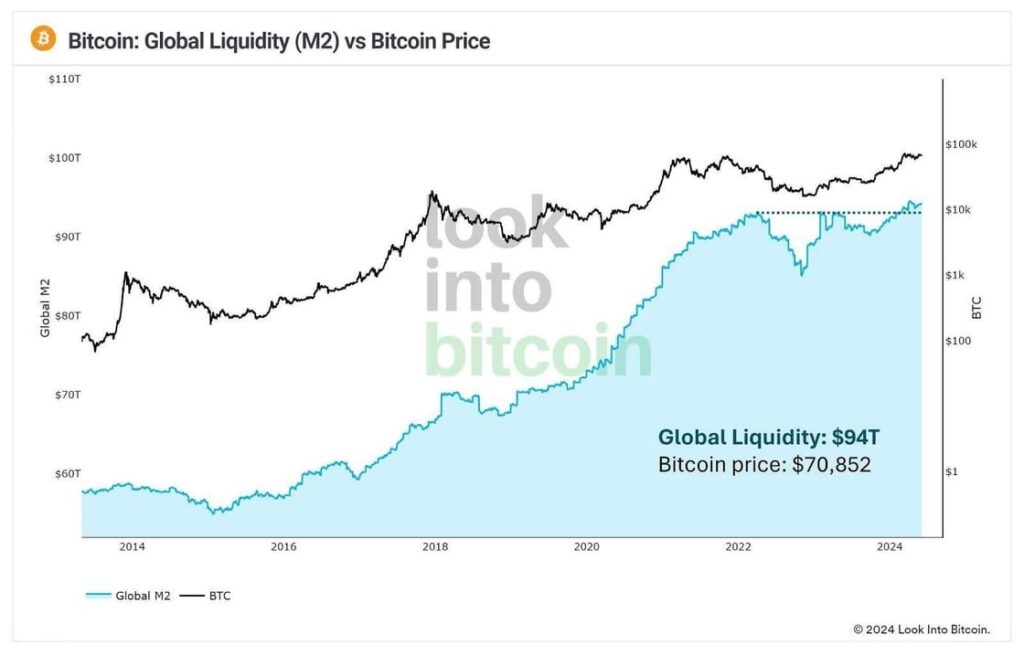

On another but rather relevant note, global liquidity has experienced an uptick in the past month, reaching an all-time high of $94T, as shown in Figure 1. As we trace the two lines, we can deduce that Bitcoin is a big profiteer of the expanding global liquidity. Almost $3T has been added since Bitcoin’s all-time high of $69K in 2021. If the banking crisis persists in the U.S. and spreads worldwide, like last year, central banks will have to step in to make their banks whole, which will translate into the growth of their balance sheets even more. Higher liquidity reduces perceived uncertainty, encouraging investors to increase their risk-taking in assets like equities and crypto.

Figure 1 – Bitcoin’s Performance Against Global Liquidity

Source: IntoTheBlock

BTC’s Rising Accumulation Meets a Growing Delta-Neutral Trading Strategy

Last week, the Bitcoin ETF market sustained its recent momentum, mostly driven by the shifting sentiment around the global economy’s battle against inflation, as discussed in the previous section. This was symbolized by the ECB and Bank of Canada’s move to cut rates, which led Bitcoin to hit $72K while its open interest reached an all-time high of $32.02B. However, this was shortly met with a cascade of liquidations (~$400M) as the excitement was countered by the jobs report, which gave a troubling signal of the FED’s progress on taming inflation, leading the entire crypto market to drop by 4%.

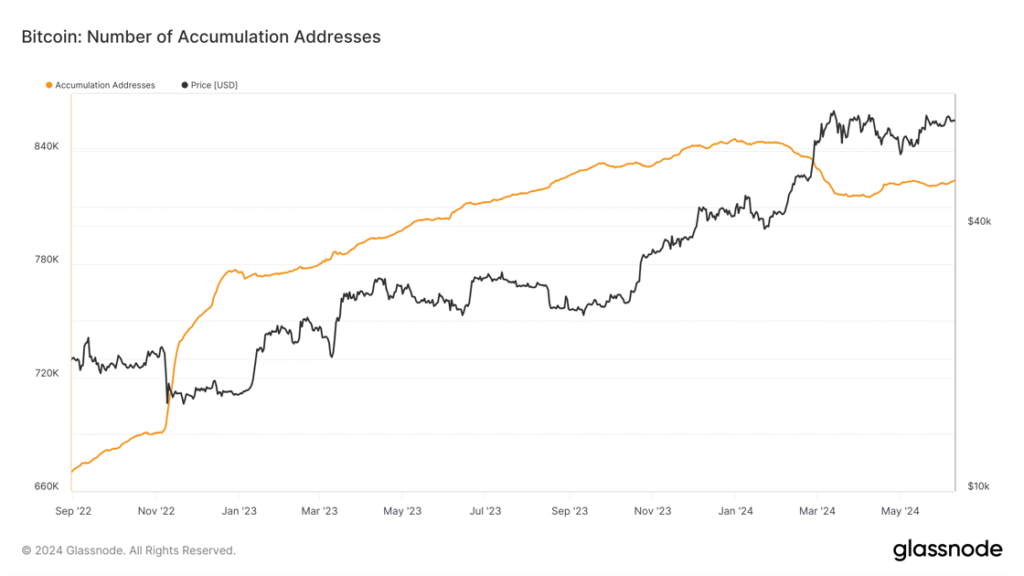

That said, U.S. spot ETFs accumulated nearly 25,729 BTC over the last week, equivalent to eight weeks’ worth of new BTC supply entering the market from block rewards. Notably, the impressive recent inflows led to recording the second strongest day of inflows since late March, with more than 12K BTC absorbed via ETFs on June 4. Overall, ETFs now hold close to 5% of Bitcoin’s total supply while making up roughly 60% of Gold ETFs assets under management in the U.S. As we’ve emphasized over the past months, the impact of ETFs on the supply and demand dynamics of the BTC market shouldn’t be ignored. They continue to lay the groundwork for a supply shock that could occur in the medium to long term, especially as BTC on exchanges continues to reach the lowest point in over six years. Similarly, Bitcoin’s accumulation addresses (wallets that have received more than two transactions and have never spent their funds) saw an uptick in the last few weeks, as shown in Figure 2. This echoes our belief that long-term believers are unfazed by their short-term volatility and believe that Bitcoin still has more room to grow.

Figure 2: Total Number of Bitcoin Accumulation Addresses

Source: Glassnode

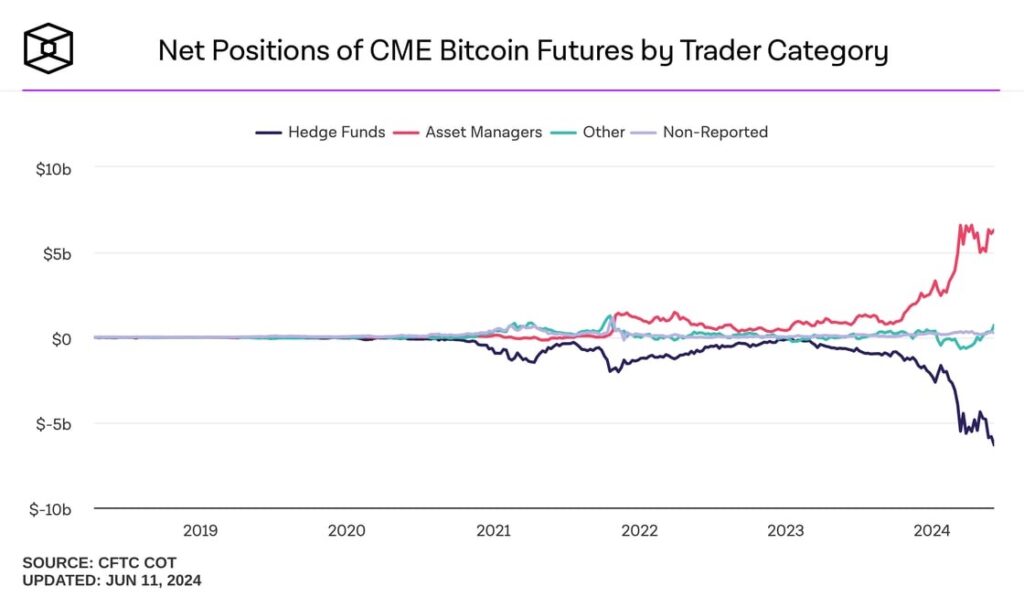

However, one notable trend to monitor though is the emergence of a cash-and-carry trade, as depicted in Figure 3. This strategy involves investors purchasing Bitcoin on the spot market through ETFs, while simultaneously shorting it on the CME Group exchange to capitalize on the arbitrage opportunity. This phenomenon helps rationalize why the buying pressure from ETFs was being offset by the shorting activity on the futures market. In that sense, it provides a more comprehensive understanding of the surge in Bitcoin’s open interest while potentially explaining why BTC wasn’t able to break through its major resistance at $72K.

Figure 3: The Net Positions of Different Investors on CME Exchange

Source: TheBlock

Exciting Future for Bitcoin’s Scaling Potential

Moving on, Bitcoin’s fundamentals received a significant boost last week. Starknet, the developer of one of Ethereum’s leading scaling solutions, announced its plans to expand to Bitcoin. The company aims to integrate its Zero-Knowledge technology, which powers its Layer 2 platform, to scale Bitcoin without requiring any hard forks. According to Starknet’s founder, the solution will be designed to allow applications to settle transactions on both Bitcoin and Ethereum simultaneously, enhancing Bitcoin’s competitiveness as a settlement platform for a broader landscape of transactions. That said, the key to making this integration a reality lies in the potential soft fork upgrade known as OP_CAT, which could unlock new possibilities for Bitcoin’s scripting language.

For context, OP_CAT is a decade-old script from the Satoshi era that enabled a more feature-rich programming language that paves the path for smart contracts on top of Bitcoin. However, Satoshi removed it as it was feared that it could introduce more security risks into the network, which we’ll break down later. Nevertheless, the function is now making a resurgence as certain segments of the Bitcoin community are looking for different ways to scale the network. This is inspired by the innovation spurred by Ordinals last year, which was enabled on the back of the 2021 soft fork upgrade called the Taproot upgrade.

In line with this, reintroducing OP_CAT could significantly benefit Bitcoin. It can simplify the creation and management of assets’ metadata, thereby laying the groundwork for asset tokenization. It can also enable secure vaults to safeguard against unauthorized access to users’ wallets through advanced multi-signature setups. Additionally, OP_CAT can support escrow wallets, which is crucial for financial use cases that involve locking BTC in a smart contract for yield-generation purposes or using it as collateral for money markets. Lastly, OP_CAT will play a pivotal role in enabling expressive smart contracts, such as trustless bridges, essential for the emergence of Layer 2 solutions, which Starknet aims to capitalize on replicating Ethereum’s scaling success on Bitcoin.

On the other hand, the concerns that led Satoshi to avoid OP_CAT remain pertinent today. The reintroduction of this function could create large scripts that consume significant resources, potentially leading to vulnerabilities such as Denial of Service (DOS) attacks that could cripple Bitcoin’s usage. DOS involves flooding and overwhelming a system with a massive number of requests and messages to bring it down to a halt and make it impossible to process transactions. The function could also introduce unforeseen security threats that weren’t relevant a decade ago, while it could result in a hard fork if certain node operators don’t support the upgrade.

Thus, given the network’s value proposition as the oldest and most secure blockchain, the trade-off between modifying the network’s codebase to add more features, which increases its complexity, versus leveraging external solutions that transform the network’s utilization is contentious. This explains why the functionality has been hotly debated for years but has never been implemented. Nevertheless, it is noteworthy that OP_CAT was formally designated as BIP420 in April, leaving the decision to implement the upgrade to the community for consideration and debate.

In conclusion, the emergence of various scaling solutions for Bitcoin is a significant development. This includes Stacks’ approach utilizing sidechain technology, BitVM enabling rollups similar to Ethereum’s Arbitrum and Optimism, Ordinals and Runes creating unique digital assets, and now the potential of OP_CAT. The diversity of these scaling methods is essential for fostering a robust and resilient ecosystem, as it ensures that Bitcoin is not limited to a single approach and can continue innovating if one solution becomes obsolete.

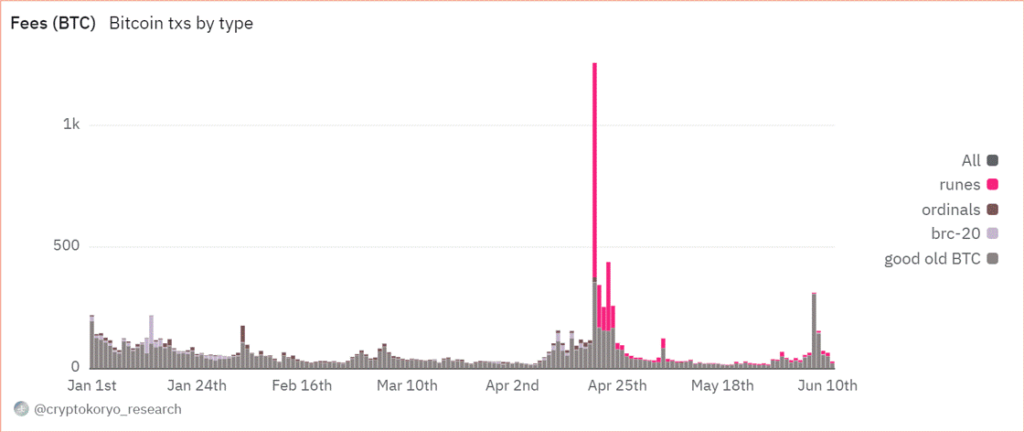

This is crucial because miners need a supplementary source of income to mitigate the decline in revenue resulting from block issuance and ensure the long-term sustainability of the network as the newly mined BTC supply continues to decrease. Similarly, the economic impact of Ordinals, BRC20, and Runes can’t be understated, as they play a sizable role in Bitcoin’s on-chain activity. For context, miners were able to generate close to 11K BTC, equating to $750M, in fees from processing transactions related to all three aforementioned primitives over the last year, as seen below in Figure 4. This underscores the necessity for scaling solutions to offset the diminishing revenue from Bitcoin’s decreasing block issuance by allowing an on-chain economy to emerge on the largest crypto network by market capitalization.

Figure 4: Revenue Generated from Bitcoin’s Ordinals, BRC20, Runes

Source: CryptoKoryo on Dune Analytics

Ethereum: The Future of Finance and the Internet Itself

The 12th issue of our State of Crypto is out! What’s Inside?

• An introduction to the Ethereum economy: ETH supply, smart contracts, and gas fees.

• A map of the Ethereum ecosystem of scalability solutions and decentralized applications.

• An explainer of Ethereum’s Staking and Re-Staking primitives and their associated risks.

• Our signature Ethereum valuation methodologies

You can download the report here.

This Week’s Calendar

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Fem spanska fonder som har ökat med +12% under 2025

ASRP ETF ett spel på medtech företag världen över

Europafokuserade ETPer ser större andel av flödena under första kvartalet

JAAA ETF an aktiv satsning på säkerställda obligationer

Can crypto outperform amidst the current market turmoil?

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Svenskarna har en ny favorit-ETF

MONTLEV, Sveriges första globala ETF med hävstång

Sju börshandlade fonder som investerar i försvarssektorn

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEuropeisk försvarsutgiftsboom: Viktiga investeringsmöjligheter mitt i globala förändringar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa