Nyheter

Property Market Nearing a Trough?

Property Market Nearing a Trough? While some key economic indicators in China took a pause in July from their improving trend of recent months, we believe targeted policy stimulus will drive growth higher though the rest of the year and into 2015.

The domestic equity market has shrugged off the recent batch of weak numbers and the MSCI China A Share index has rallied 10% in the past month.

One of the factors weighing on economic performance recently is weakness in the property sector.

According to IMF calculations, the real estate sector together with construction accounts for 15% of GDP, a quarter of fixed asset investment and 14% of urban employment. The health of the property sector is therefore important to the health of the overall economy.

We believe that the property sector is going through an orderly correction and will near a trough in coming months as the effects of policy stimulus kicks in.

We believe the government has the capacity and the policy conviction to stimulate the property market and the broader economy into 2015.

ORDERLY PROPERTY MARKET CORRECTION

The Chinese property market is correcting. Price growth has moderated in year-on-year terms and on a month-on-month basis, more cities have reported declines than ever before. We believe the deterioration in July will prompt further policy stimulus that will lead to a turn in the property cycle. The government is determined to see economic growth measured in GDP terms hit 7.5% this year and is unlikely to let a downturn in the property market derail its plans.

Third tier cities suffering the most

The price moderation has been the most pronounced in third tier cities. Residential real estate inventories in third tier cities have increased the most. The oversupply is in part linked to local governments’ reliance on land sales to finance spending (see China Macro Monitor July 2014). Land is more easily available to developers in these cities as governments are keen to monetise their assets. We believe that reform in local government financing will reduce this source of supply over time.

Real estate investment has moderated, but shows signs of stabilisation

Real estate fixed asset investment accounts for about a quarter of total fixed asset investment. While its growth has been moderating, it has stabilised at a relatively high level of over 14% y-o-y over the past three months. According to IMF calculations, a 1% decline in real estate investment could shave off 0.1% of GDP growth in the first year1. China appears to be very far from seeing an actual decline in investment, but we would expect the government to be vigilant against any downturn that would threaten its growth targets. The IMF projects GDP growth of 7.4% this year, with real estate investment growth moderating to 5% y-o-y.

Property sales subdued while potential buyers wait on the side-lines

Potential buyers talking a ‘wait-and-see’ approach have been blamed for the decline in property sales. The pace of urban migration remains robust and pent-up demand to upgrade properties has certainly not fallen. With the threat of the malaise in the property market becoming self-fulfilling, we expect the government to offer further stimulus the break the cycle. Residential property sales had become less negative in June, but slipped further July alongside other measures of economic performance.

Low household leverage and continued urbanisation bode well for medium term property demand

China is little over 50% urbanised, significantly less than other emerging markets such as Brazil and Russia and will continue to urbanise at a strong pace over the coming 20 years. According to the United Nation’s projections, 310 million Chinese citizens (i.e. a population close to the size of the US today) will migrate from the countryside to cities over the next two decades. The Chinese government’s ambitions are even grander – to move close to 400 million people to the cities. That speed and scale of migration is unprecedented in human history. Even though a number of cities appear to be over-supplied with property today, we believe that excess supply will soon be absorbed.

Household indebtedness in China is also low by international standards. The orderly property market correction we foresee in China is unlikely to lead to a systemic problem for households because their financial leverage is relatively small.

We believe that such low level of indebtedness affords the government headroom to loosen house purchase restrictions (HPR) and lending criteria to stimulate the property market. As more Chinese people aspire to become homeowners, we are likely to see household leverage rise over time.

Policy relaxation will provide a tail-wind

In contrast to 2008 and 2011, when the People’s Bank of China cut the reserve requirement ratio (RRR) to stimulate lending activity across the board, recent stimulus has largely been left to local governments and is therefore highly targeted2.

For example, a number of cities have relaxed rules that previously prohibited households from owning more than one property (house purchase restrictions or HPRs). 37 out of 46 cities that had such restrictions have reportedly relaxed to some extent.

Some cities and provinces have announced tax subsidies to spur demand while others have been buying properties that have already been built to add to their pool of social housing.

The PBoC has also asked banks to speed up mortgage approvals and apply ‘reasonable’ pricing, which could quicken the pace of home sales. Anecdotal evidence from media reports point to banks following through on that request.

Changes to the loan-to-deposit ratio (LDR) made in July will also free up banks’ capacity to lend. By reducing the categories of lending that need to be included in the loan component and increasing the number of items that can be included in the deposit component, banks will be able to avoid hitting their LDR limits so easily, allowing them to lend more to prospective home buyers.

To support real estate development, the central government has increased its social housing target to 7 million units of new starts (of which 4.7 million units will come from shanty town renovation). The central government is also leaning on local governments to see that red-tape does not slow the process of fiscal disbursement and planning approvals.

The central government could go further by relaxing Hukou policies, which currently apply laws asymmetrically to migrants from the country and native city dwellers. Easing of these laws, could allow the freer movement of people ratio and cut mortgage interest rates (either as part of an overall cut in rates or independently).

Developers display cautious optimism

The annual decline in floor space started has been narrowing in recent months, in a sign that property developers are becoming more optimistic about future demand. Developers need to plan ahead of the actual turn given the lag between starting development and the actual completion of properties to sell in the market. Nevertheless, if their optimism proves to be timely, we could see the property market trough soon.

CHINA A SHARE SENTIMENT MARKEDLY IMPROVES

Despite the string of weak data in July, including disappointing loan and money supply growth, equity markets rallied. The MSCI China A Share index gained 9.5% last month.

The China A Share market is also likely to benefit from the launch of the Shanghai-Hong Kong Connect, which expected in October 2014 (see Shanghai-Hong Kong Stock Connect: A Boost For China A Shares) . The initiative will open up access to the Shanghai stock market for foreign investors trading through Hong Kong. Systems testing for the initiative will start at the end of this month. We believe that the manner in which the quotas are applied will drive net flows into the mainland. At the moment, dual-listed stocks are trading at approximately an 8% discount on the A shares market compared to the H share market. The introduction of the Shanghai-Hong Kong Connect should see that discount dissipate over time. Valuations of the China A share market indicate that it is cheap. Its prospective PE now stands at 10.2, 63% below its peak in 2007. It is not often that the stock market of one of the world’s largest and fastest growing economies is trading at one of the world’s lowest valuations. The imminent implementation of the Shanghai-Hong Kong Connect programme should help to speed the process of valuation normalisation.

Important Information

This communication has been provided by ETF Securities (UK) Limited (”ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the ”FCA”).

Stablecoins are digital currencies tied to assets like the U.S. dollar, offering the price stability needed for payments. They maintain their peg by being backed 1:1 by their underlying fiat currency, with issuers holding equivalent amounts in cash and cash equivalents, making stablecoins a digital representation of those reserves. Their market has doubled to over $235 billion, with daily usage nearly doubling in two years.

Why are stablecoins making headlines now?

Due to their clear product-market fit and growing mainstream adoption, stablecoins have become a top priority for regulation, with both industry leaders and policymakers calling for swift action.

On April 4, the Securities and Exchange Commission’s Division of Corporation Finance finally clarified that stablecoins are not securities if backed one-for-one by USD or similar assets and used for payments or value storage. These “Covered Stablecoins” are not marketed as investments, lack profit incentives, and include protections like reserves, making securities law registration unnecessary for issuance or redemption.

The GENIUS Act, introduced in February and advanced by the U.S. Senate Banking Committee in March, marks a major step toward creating a clear legal framework for stablecoin issuance and oversight. This clarity is driving momentum as Fidelity is set to launch its own stablecoin, and Bank of America is preparing to follow it once legislation is finalized.

Globally, the European Union’s Markets in Crypto Assets (MiCA) framework has already come into effect, reinforcing a broader shift toward formal integration of stablecoins into traditional finance. These developments reflect a growing consensus that stablecoins are emerging as essential infrastructure for global payments, treasury management, and digital asset adoption.

What are the benefits of stablecoins?

Stablecoins are digital currencies designed for fast, low-cost, and stable transactions. Since their launch in 2014, they’ve become a go-to tool for online payments, especially cross-border transfers. As they’re pegged to stable assets like the U.S. dollar or euro, they avoid the wild price swings seen in other cryptocurrencies.

They’re accessible to anyone with internet, making them especially valuable in regions with high inflation or limited banking access, like Argentina or Turkey.

With some built on public blockchains, stablecoins offer transparency, letting users track transfers and supply in real time. For institutions, they also simplify treasury management by acting as efficient digital cash that can be deployed instantly.

Who are the major players in the stablecoin race?

Tether (USDT) and Circle (USDC), the two largest stablecoin issuers, collectively hold over $204 billion in U.S. Treasuries, making them the 14th largest holders globally. Their combined treasury holdings surpass those of entire nations, including Norway and Brazil.

USDT leads with $144 billion in circulation; USDC, backed by Coinbase and known for compliance, has become a trusted digital dollar across global finance.

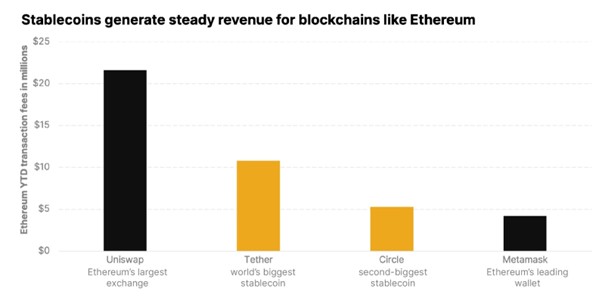

Why stablecoins matter: A revenue engine for blockchains

Stablecoins generate steady revenue for blockchains like Ethereum and Solana by driving transaction fees with each transfer. With trillions in annual volume, they help sustain network activity beyond speculation.

On Ethereum, for example, USDT and USDC transactions are major contributors to daily gas fees. Year to date, Tether ranks #3 and USDC ranks #5 in terms of total gas consumed. Tether and Circle also dominate daily transaction activity on Ethereum, averaging approximately 12 million and 6 million transactions per day, respectively, making them the top two entities on the network by daily transaction count.

Meanwhile, on Solana, stablecoin activity has surged, helping sustain validator rewards and strengthen protocol economics. In addition to the mainstream utility, stablecoins represent reliable, protocol-level cash flow, making them crypto’s killer use case.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Stablecoins: The real powerhouse of crypto

BE29 ETF är en portfölj företagsobligationer med förfall 2029

Guld-ETFer slår Bitcoin-ETFer kraftigt under första kvartalet 2025

INGH ETF är en satsning på global infrastruktur

SPFT ETF är en global satsning på teknikföretag

Fonder som ger exponering mot försvarsindustrin

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Warren Buffetts råd om vad man ska göra när börsen kraschar

Svenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV mars 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSju börshandlade fonder som investerar i försvarssektorn