Nyheter

Profit-taking leads to outflows in gold ETPs

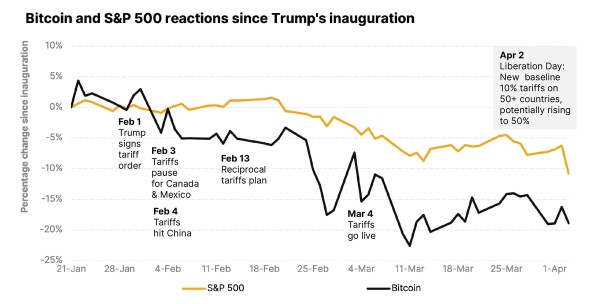

Crypto trades around the clock and often responds quickly to market uncertainty. Bitcoin usually drops first during the market turbulence because it’s risky and easy to trade, just like tech stocks. Here’s how Trump’s tariffs are playing into that.

Stablecoins: The real powerhouse of crypto

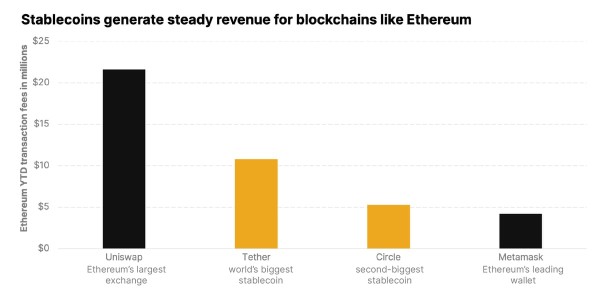

Stablecoins are digital currencies tied to assets like the U.S. dollar, making them stable in price and easy to send worldwide instantly. They drive the crypto economy, moving billions, powering financial applications, and reshaping payments. From remittances to billion-dollar treasuries, explore how leading stablecoins like USDT and USDC are making it happen.

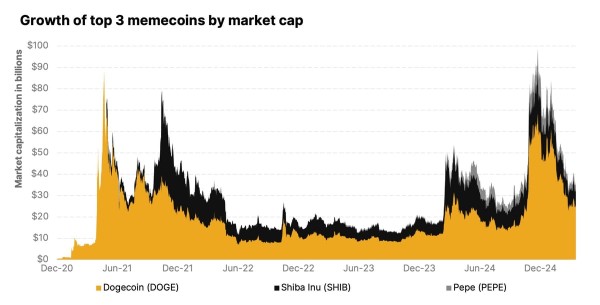

Why the memecoin mania isn’t a joke

A memecoin is a cryptocurrency inspired by internet memes or viral trends. Unlike traditional cryptocurrencies focused on utility (like Bitcoin or Ethereum), memecoins thrive on community engagement, humor, and speculative momentum. With low barriers to entry, they’re easy to create and trade, making them a go-to starting point for crypto newcomers.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

JESM ETF en fond från JPMorgan som satsar på emerging markets

Trump’s Liberation Day: The impact of tariffs on the crypto market

WEBN ETF en billig globalfond från Amundi

Mar.25 crypto update, Research commentary on market turmoil, CIO Notes and ETP performance attribution

NXTB ETP spårar värdet på kryptovalutan Bitcoin

Fonder som ger exponering mot försvarsindustrin

Warren Buffetts råd om vad man ska göra när börsen kraschar

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

De bästa börshandlade fonderna för tyska utdelningsaktier

Svenskarna har en ny favorit-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa börshandlade fonderna för tyska utdelningsaktier

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetf lanserar Europa-fokuserad försvars-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEn av de mest nedladdade finansapparna i Sverige