Nyheter

Platinum ETPs See Largest Inflows in 6 Weeks as Mine Strike Positions Harden

Platinum ETPs See Largest Inflows in 6 Weeks as Mine Strike Positions Harden. Over the past week attention has been focused on platinum group metals as London hosted its annual Platinum Week activities. Platinum ETPs also saw increased attention with ETFS Physical Platinum seeing its largest inflows in six weeks. The ongoing strike action in South Africa is driving interest in the metal as the stalemate looks like it will persist for some time to come. Gold traded in a very tight range as US Fed minutes revealed little urgency in tightening policy while the Ukrainian crisis continued to drive safe haven buying.

ETFS Physical Platinum (PHPT) sees highest inflows in six weeks. With the strike in South Africa showing little sign of resolution, the platinum price rose 1.4% and US$6.1mn flowed into PHPT. Despite the three largest miners in South Africa using the Labour Court to mediate the wage dispute with Association of Mineworkers and Construction Union (AMCU), Impala’s CEO conceded that the strike could go on for longer. Johnson Matthey, published its latest forecast for the industry, projecting a 1.2mn oz supply deficit for platinum (from 0.9mn oz deficit last year) and a larger 1.6mn oz supply deficit for palladium (from 0.4mn oz last year). Even after the pay dispute is resolved there will be a lag before production can be ramped up to full capacity, prolonging the delay in getting supply to the market. It is clear that secondary supply is unable to catch up with the primary deficit, keeping the market very tight.

Profit-taking drives US$4.5mn of outflows from long WTI crude oil ETPs. US$3.5mn flowed out of ETFS WTI Crude Oil (CRUD), the highest in 13 weeks, while a further US$1mn withdrew from ETFS Daily Leveraged WTI Crude Oil (LOIL), the most in 5 weeks as WTI prices rose 2.2% over the week. Against analysts’ expectations, total crude oil inventories in the US dropped sharply by 7.2 million barrels, the largest drawdown since early January. Last week’s withdrawals could potentially mark the beginning of the seasonal drawdown ahead of the US summer driving season. An earlier-than-expected pick-up in oil demand would provide further support to the WTI price currently at around US$104/bbl.

Broad agriculture ETP sees largest outflows in a month as grain supply expectations rise. As most agricultural prices slipped, investors withdrew $5.6mn from ETFS Agriculture last week. The USDA’s corn surplus forecast for 2014/15 and rain assisting US wheat production led to price declines of 1.5% and 2.8% respectively. Some investors saw the price moves as a buying opportunity, with US$3.1 of inflows into long corn ETPs (a 10 week high) and 2.5mn into long wheat ETPs (13 week high). The coffee price continued to fall last week (dropping 6.6%) as more market participants digested the report from Conab (Brazilian National Agricultural Supply Company) that showed that damage from the drought earlier this year was not as bad as feared.

US$3.4mn flowed out of long copper ETPs, the most in 11 weeks, driven by profit taking. Copper rose 0.3% last week, bringing its monthly gain to 4.1%. Last week’s better-than-expected HSBC Chinese manufacturing PMI helped bolster the metal as the outlook for China’s industrial demand improves. Given the heavy net short speculative positioning in the futures market we believe that copper has significant upside potential we target US$7500/MT as industry expectations of supply surplus this year will likely need to be trimmed.

Key events to watch this week

A relatively quiet will see focus placed on the US durable goods orders as a gauge for the strength of consumer demand for big-ticket items.

Note: All flow and AUM data in this report are based on ETF Securities ETPs to 22 May 2014 and are denominated in USD unless otherwise indicated.

Important Information

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (”ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (”FCA”).

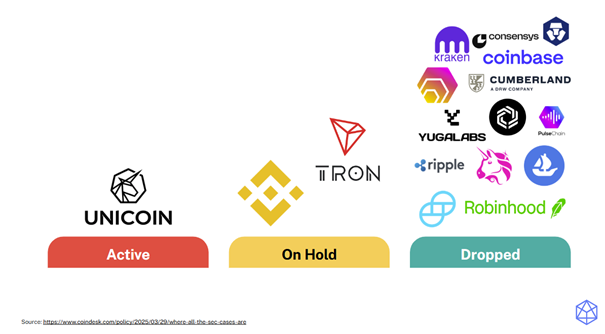

Since President Trump appointed Mark Uyeda as acting SEC chair two months ago, many investigations into crypto businesses have been dropped, as the SEC moves away from regulation by enforcement and works to create a framework for digital assets. As regulations become clearer and news flow turns more positive, crypto prices—which dropped sharply this week—should begin to better reflect the new regulatory landscape in the US.

We believe this regulatory shift could ultimately help trigger the next leg of the current bull run, as investors better understand the significance of regulatory clarity and seek to acquire bitcoin and altcoins at what we believe are currently very favorable levels.

Market Highlights

SEC Dismisses Crypto Enforcement Actions

The SEC dropped its enforcement actions against crypto-related companies Kraken, Consensys, and Cumberland DRW.

This indicates a shift in SEC’s regulatory approach, favoring clearer guidelines over enforcement actions. Such a pivot could foster a more predictable environment, encouraging innovation within the sector.

Banks to Engage in Crypto Activities

The FDIC has rescinded previous guidelines which prevented financial institutions from engaging with crypto activities without prior sign-off.

By removing bureaucratic hurdles, banks may more readily offer crypto-related services, potentially leading to broader adoption and integration of digital assets.

Bitcoin ETFs Inflow Streak Surpassed $1 Billion

US spot Bitcoin ETFs have recorded a 10-day inflow streak exceeding $1 billion marking the longest such streak in 2025.

This underscores growing institutional and retail investor confidence in Bitcoin as an asset class that helps increase market stability and possibly paving the way for the approval of other crypto-based financial products.

Market Metrics

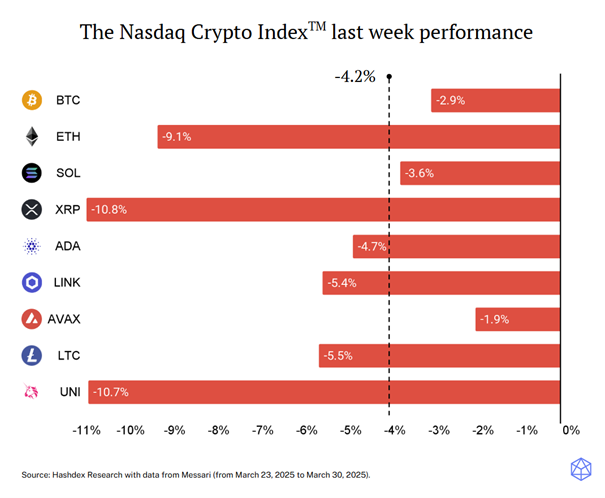

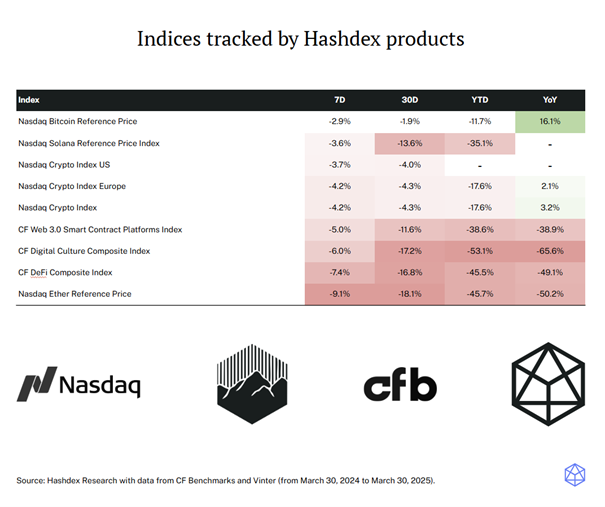

All NCITM constituents had negative performance last week, with XRP (-10.8%) and UNI (-10.7%) seeing the steepest declines. ETH also experienced a sharp drop (-9.1%), contributing to NCITM’s underperformance relative to BTC (-2.9%). The NCITM -4.2% decline reflects a broader risk-off sentiment in the crypto market, as investors reassess their positions amid ongoing macroeconomic uncertainties.

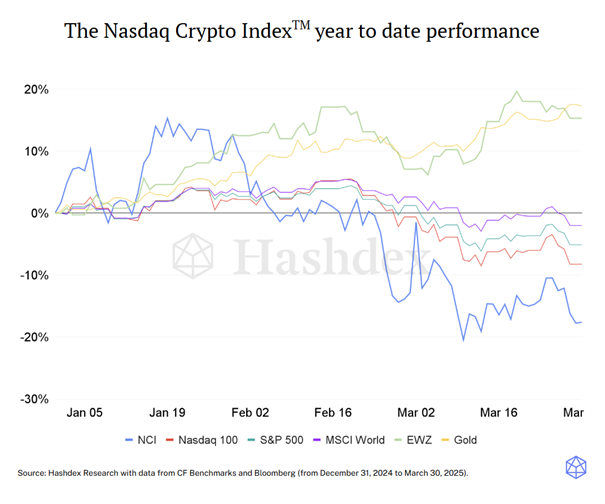

NCITM (-4.2%) extended its underperformance last week, deepening year-to-date losses. Traditional indices like the S&P 500 (-1.5%) and Nasdaq 100 (-2.4%) saw smaller declines. The gap between crypto and other risk assets continues to widen, while gold has emerged as the top performer in 2025, gaining nearly 20% amid ongoing macroeconomic uncertainties. This trend highlights a growing risk-off sentiment, with investors shifting toward defensive assets and away from high-volatility investments.

21Shares ringer i klockan på Nasdaq Stockholm när denna kryptoemittent fortsätter att utöka sitt utbud av produkter som är tillgängliga i regionen med noteringen av sina börshandlade produkter CBTC (Bitcoin), ASOL (Solana) och AXRP (Ripple) ETP på Nasdaq Stockholm (OMX).

Detta markerar ytterligare ett steg framåt för 21Shares i Norden när 21Shares tittar på att göra ytterligare 21Shares-produkter mer tillgängliga för 21Shares lokala kundbas i svenska.

US regulatory shift provides a beacon for optimism

BCFP ETF en ackumulerande fond som investerar i Nasdaq-100

21Shares ringer i klockan på Nasdaq Stockholm

Börshandlade fonder på australiensiska och japanska statsobligationer från DWS

BlackRock utökar Active ETF Suite med Fixed Income Enhanced UCITS ETFer

Fonder som ger exponering mot försvarsindustrin

WisdomTree lanserar europeisk försvarsfond.

Warren Buffetts råd om vad man ska göra när börsen kraschar

Trumps återkomst får europeiska aktier att rusa

SAVR Global by Vanguard: Ett billigt alternativ till globala indexfonder

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanWisdomTree lanserar europeisk försvarsfond.

-

Nyheter7 dagar sedan

Nyheter7 dagar sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanTrumps återkomst får europeiska aktier att rusa

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSAVR Global by Vanguard: Ett billigt alternativ till globala indexfonder

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDe bästa börshandlade fonderna för tyska utdelningsaktier

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanUtdelning i XACT Norden Högutdelande mars 2025

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanEn av de mest nedladdade finansapparna i Sverige