Nyheter

Payrolls Data Highlights Policy Divergence

ETFS Multi-Asset Weekly Payrolls Data Highlights Policy Divergence

- Freezing weather conditions support natural gas prices.

- Confirmation of QE sends gold miners lower.

- Divergent monetary paths pressures Euro.

This week will be dominated by the launch of the heavily anticipated quantitative easing program by the ECB. A strong US non-farm payroll reading on Friday underlined the stark contrast in circumstances for the Federal Reserve and the European Central Bank. As demonstrated on Friday, European and American economies are likely to continue to diverge in line with prospects for monetary policy. However, after the official Chinese growth target was lowered this week attention may shift to Chinese lending data due next week.

Commodities

Freezing weather conditions support natural gas prices. Snowfall and frigid temperatures in the eastern half of the US boosted heating demand for natural gas. A larger-than-expected withdrawal from natural gas inventories last week sent prices higher, with Henry hub gas ending the week up 5.3%. Reports that US crude stocks rose to a record 444.4mn barrels last week failed to prevent WTI prices climbing higher. The US crude benchmark was supported by a release of the Federal Reserve’s beige book which detailed the likely cut in capital expenditures by US oil producers in 2015 as the plunge in oil prices impacts the industry. Carbon prices fell 4.4%, as coal-reliant members of the European parliament posed a potential roadblock to negotiations towards the relief of the current oversupply of allowances in the emissions market.

Equities

Confirmation of QE sends gold miners lower. After reaffirming the launch of quantitative easing, Mario Draghi delivered a relatively upbeat assessment of the Eurozone’s economic prospects. The positive tone sent European bourses rising with the DAX 30 and FTSE MIB climbing 1.6% and 1.1%, respectively. The prospect of stimulus in Europe boosted sentiment and dented safe haven demand for gold resulting in its decline through the psychological US$1,200/oz level. The fall in gold prices caused DAXglobal® Gold Miners Index to fall 4.8%. The strong performance of European stocks pushed volatility lower and the EURO STOXX 50® Investable Volatility Index to its lowest level this year at 15.3. The MSCI China A Index fell 0.9% as the Chinese premier Li Keqiang reduced the official growth target to 7.0% from 7.5% as the country tackles structural and economic reform.

Currencies

Divergent monetary paths pressures Euro. Last week the prospect of the ECB’s QE programme launch caused the Euro to fall to an eleven and a half year low against the US dollar. These losses were extended on Friday as a strong US non-farm payroll reading increased the likelihood of US rate normalisation starting at the Fed meeting in June. Recent indications that the US economy continues to strengthen brings the timeline for higher interest rates forward. While in Europe the ECB plans to loosen monetary policy and various central banks have put negative interest rates in place to combat deflation. The differing outlooks have sent the Dollar and Euro in opposite directions against other major global currencies, a trend which only looks set to continue.

Important Information

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (”ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (”FCA”).

2024 was a landmark year for bitcoin, solidifying its role as a fully institutionalised asset class.

Institutional inflows into physical bitcoin exchange-traded products (ETPs) reached nearly $35 billion globally, signalling a major shift in how traditional investors view crypto. As bitcoin continued to enhance portfolios’ risk-return profiles, more institutional investors followed suit, reshaping the financial landscape.

Looking ahead, 2025 promises to bring exciting developments across the crypto ecosystem. Here are the top five crypto trends to watch.

Fear of being left behind

The era of bitcoin as a niche investment is over. Institutional adoption is creating a ripple effect, forcing hesitant players to reconsider. Portfolios with bitcoin allocations are consistently outperforming those without, highlighting its growing importance.

Figure 1: Bitcoin in a multi-asset portfolio

| 60/40 Global Portfolio | 1% Bitcoin Portfolio | 3% Bitcoin Portfolio | 5% Bitcoin Portfolio | 10% Bitcoin Portfolio | MSCI AC World | Bloomberg Multiverse | Bitcoin | |

| Annualised Return | 5.77% | 6.46% | 7.83% | 9.20% | 12.57% | 9.07% | 0.56% | 56.24% |

| Volatility | 8.79% | 8.86% | 9.14% | 9.62% | 11.42% | 13.94% | 5.05% | 67.28% |

| Sharpe Ratio | 0.48 | 0.55 | 0.68 | 0.79 | 0.96 | 0.54 | -0.20 | 0.81 |

| Information Ratio | 1.01 | 1.01 | 1.01 | 1.00 | ||||

| Beta | 70% | 71% | 73% | 75% | 81% | 100% | 24% | 181% |

Source: Bloomberg, WisdomTree. From 31 December 2013 to 30 November 2024. In USD. Based on daily returns. The 60/40 Global Portfolio is composed of 60% MSCI All Country World and 40% Bloomberg Multiverse. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investment may go down in value.

With bitcoin’s ability to noticeably improve portfolios’ risk-return profiles, asset managers face a clear choice: integrate bitcoin into multi-asset portfolios or risk falling behind in a rapidly evolving financial landscape. In 2025, expect the competition to heat up as clients demand exposure to this powerhouse cryptocurrency.

Expanding crypto investment options

In 2024, regulatory breakthroughs opened the doors for physical bitcoin and ether ETPs in key developed markets. This marked a critical step towards making cryptocurrencies mainstream, providing seamless access to institutional and retail investors alike.

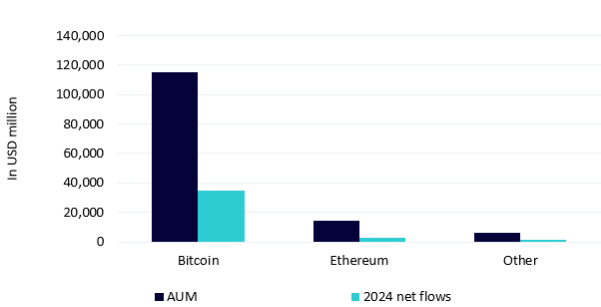

Figure 2: Global physical crypto ETP assets under management (AUM) and 2024 net flows

Source: Bloomberg, WisdomTree. 02 January 2025. Historical performance is not an indication of future performance and any investment may go down in value.

In 2025, this momentum is expected to accelerate as the crypto regulatory environment becomes more friendly in the United States and as key developed markets follow Europe’s lead and approve ETPs for altcoins such as Solana and XRP. With their clear utility and growing adoption, these altcoins are strong candidates for institutional investment vehicles.

This next wave of altcoin ETPs will expand the diversity of crypto investment opportunities and further integrate cryptocurrencies into the global financial system.

The maturing of Ethereum’s layer-2 ecosystem

Ethereum’s role as the backbone of decentralised finance (DeFi), non-fungible tokens (NFTs), and Web3 is unmatched, but its scalability challenges remain a hurdle. Layer-2 solutions—technologies such as Arbitrum and Optimism—are transforming Ethereum’s scalability and usability by enabling faster, cheaper transactions.

In 2025, Ethereum’s recent upgrades, such as Proto-Danksharding (introduced in the ‘Dencun’ upgrade), will drive layer-2 adoption even further. Innovations like Visa’s layer-2 payment platform leveraging Ethereum for instant cross-border transactions will underscore the platform’s evolution.

Expect Ethereum’s layer-2 ecosystem to power real-world use cases ranging from tokenized assets to decentralised gaming, positioning it as the infrastructure of a truly scalable digital economy.

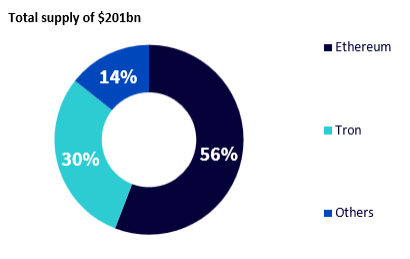

Stablecoins: bridging finance and blockchain

Stablecoins are becoming indispensable to the global financial system, offering the stability of traditional assets with the efficiency of blockchain. Platforms such as Ethereum dominate the stablecoin landscape, hosting stablecoin giants Tether (USDT) and USD Coin (USDC), which facilitate billions in daily transactions.

Figure 3: Key stablecoin chains

Source: Artemis Terminal, WisdomTree. 05 January 2025. Historical performance is not an indication of future performance and any investment may go down in value.

As we move into 2025, stablecoins will increasingly interact with blockchain ecosystems such as Solana and XRP. Solana’s high-speed, low-cost infrastructure makes it ideal for stablecoin payments and remittances, while XRP Ledger’s focus on cross-border efficiency positions it as a leader in global settlements. With institutional adoption rising and DeFi applications booming, stablecoins will serve as the backbone of a seamless, interconnected financial ecosystem.

Tokenization: redefining ownership and revolutionising finance

Tokenization is set to redefine how we think about ownership and value. By converting tangible assets like real estate, commodities, stocks, and art into digital tokens, tokenization breaks down barriers to entry and creates unprecedented liquidity.

In 2025, tokenization will expand dramatically, empowering investors to own fractions of high-value assets. Platforms such as Paxos Gold and AspenCoin are already showcasing how tokenization can revolutionize markets for gold and luxury real estate. The integration of tokenized assets into DeFi will unlock new financial opportunities, such as using tokenized real estate as collateral for loans. As tokenization matures, it will transform industries ranging from private equity to venture capital, creating a more inclusive and efficient financial system.

For the avoidance of any doubt, tokenization complements crypto by expanding the use cases of blockchain to include real-world applications.

Looking ahead

2025 is set to be a defining year for crypto, as innovation, regulation, and adoption converge. Whether it is bitcoin cementing its position as a portfolio staple, Ethereum scaling for mainstream use, or tokenization unlocking liquidity in untapped markets, the crypto ecosystem is poised for explosive growth. For investors and institutions alike, the opportunities have never been clearer or more compelling.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

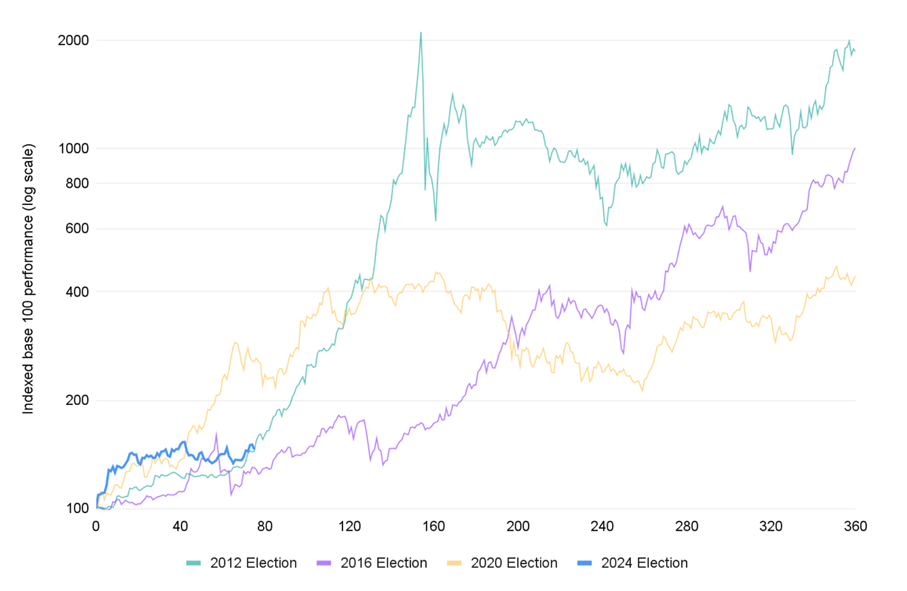

On January 20, 2025, bitcoin (BTC) reached a new all-time high, surpassing $109,000, and this milestone coincided with Donald Trump’s inauguration for his second term as U.S. President.

Historical trends show that BTC has performed exceptionally well in the 12 months following the past three U.S. elections. If history repeats, this could signal another bullish phase. With Trump’s pro-BTC stance and a U.S. Congress aligned on favorable digital regulation, the outlook for the coming months appears highly promising.

Source: Hashdex Research with data from Messari (from November 6, 2012 to January 19, 2025).

MARKET HIGHLIGHTS | Jan 13 2025 – Jan 19 2025

Bitcoin-backed loans enabled on Coinbase’s L2

• Now customers can borrow USDC in the new base’s lending protocol by using bitcoin as collateral.

• This underscores the importance of onchain innovations as the pillar for future adoption of blockchain technology, in this case enhancing personal finance to be more decentralized and intuitive in a permissionless etho..

ETF filings reiterate bullish regulatory tailwinds

• As Donald Trump’s inauguration approaches, several asset managers have filed applications for new crypto ETF products, including those focused on assets like LTC and XRP.

• This reflects optimism for 2025’s crypto regulations and their potential to transform the regulated products landscape.

Trump to make crypto top priority in US agenda

• U.S. President-elect Donald Trump allegedly plans to issue an executive order making crypto a national policy priority and establishing an advisory council.

• The announcement signals that crypto has gained political importance. Even if not all promises are met, crypto has already crossed the chasm.

MARKET METRICS

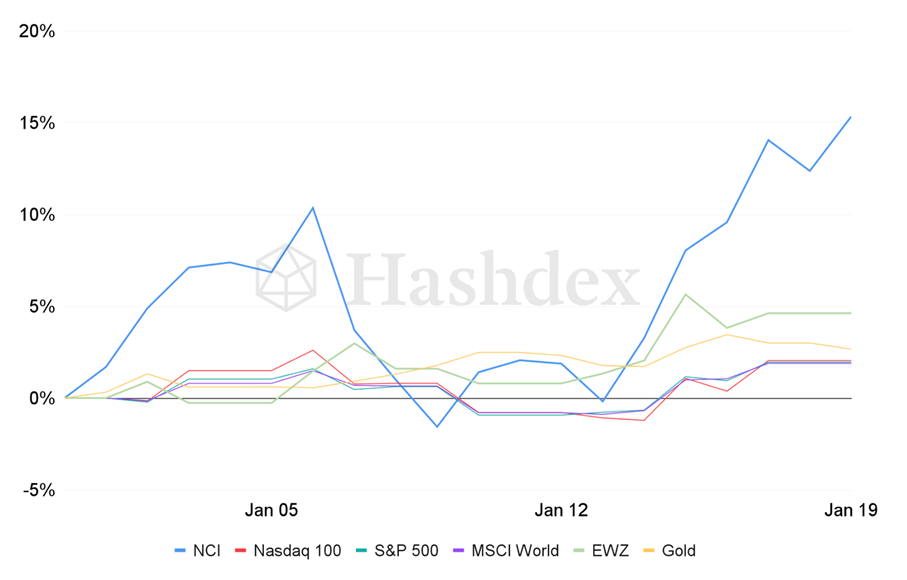

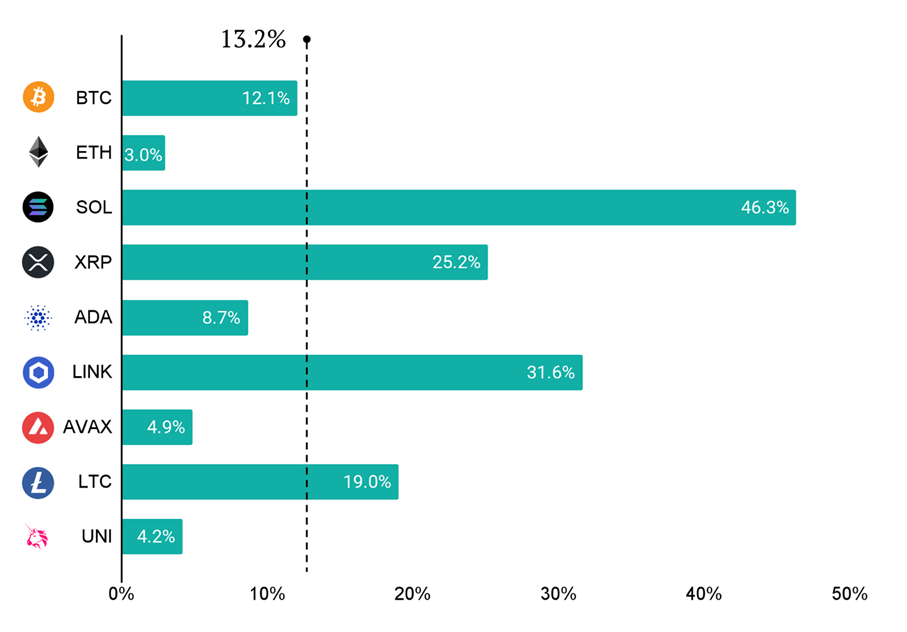

The Nasdaq Crypto Index™

This week saw a significant rise in digital assets as the market awaits Trump’s inauguration, with the NCI™ (+15.3%) outperforming all traditional asset classes. The NCI™ (+13.2%) also outperformed BTC (+12.1%), highlighting the value of diversification in a volatile market. The performance was positively impacted by SOL’s strong 46.3% gain, while ETH’s underwhelming 3.0% growth had a dampening effect.

Source: Hashdex Research with data from CF Benchmarks and Bloomberg (from December 31, 2024 to January 19, 2025).

It was a strong week for the NCI™ , with SOL leading the pack (among others, like XRP and LINK), surging 46.3%, while BTC (12.1%) and ETH (3.0%) lagged behind. This price action seems driven by excitement around Trump’s inauguration and the crypto-friendly environment his promises suggest.

Source: Hashdex Research with data from Messari (from January 12, 2025 to January 19, 2025).

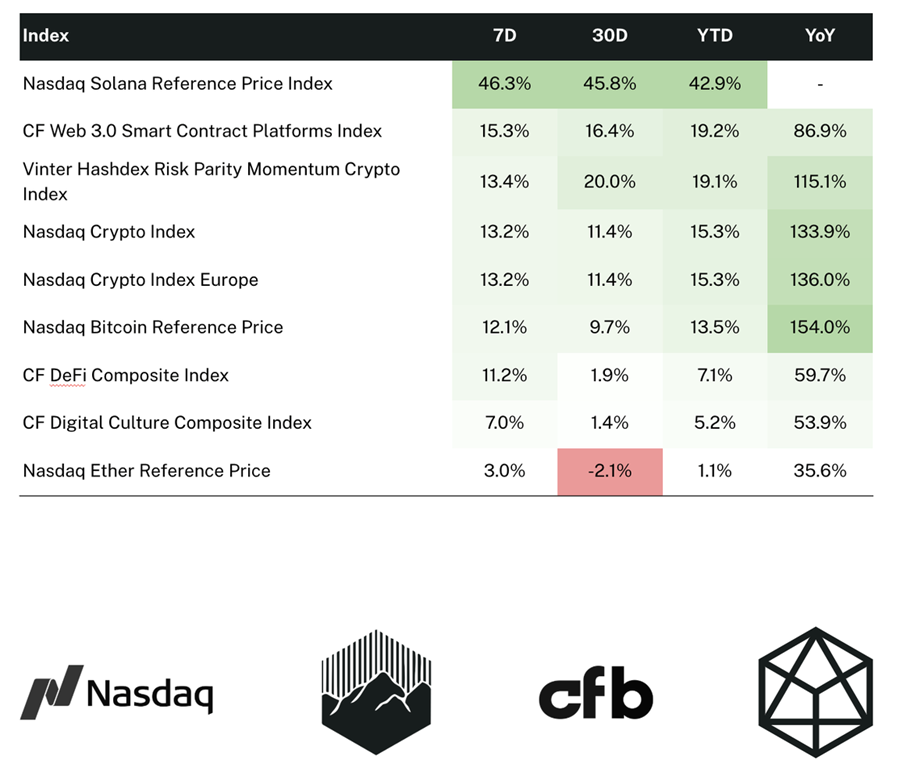

Indices tracked by Hashdex

Source: Hashdex Research with data from CF Benchmarks and Vinter (from January 19, 2024 to January 19, 2025).

5 crypto trends to watch in 2025

FGLR ETF gör hållbara investeringar i hela världen

Trump’s inauguration day, BTC all-time high and the US election bullish effect

AXA IM antar SDR-märkningar för tre aktiefonder i Storbritannien

HSDD ETF köper aktier i hållbara företag från den utvecklade världen

De mest eftersökta ETFerna i december 2024

De bästa ETFerna för värdeaktier

Post-election rally cools at year end

BlackRock slår rekord med lanseringen av bitcoin ETF

Hector McNeil kommenterar Trumps krav på Natos försvarsutgifter

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe mest eftersökta ETFerna i december 2024

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa ETFerna för värdeaktier

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanPost-election rally cools at year end

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBlackRock slår rekord med lanseringen av bitcoin ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHector McNeil kommenterar Trumps krav på Natos försvarsutgifter

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBuffertstrategin på Nasdaq-100 med december 2024/2025 som ny målperiod

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanValour PYTH SEK spårar priset på kryptovalutan PYTH

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanHANetfs Tom Bailey om utsikterna för koppar och uran