Nyheter

Krona strength may resurface

Market Insight – Foreign Exchange – Krona strength may resurface

Swedish economy surpasses expectations

Krona strength may resurface. Swedish growth and underlying inflation have continued to develop strongly, rising to the highest levels in over four years and beating expectations of both its own central bank (Sveriges Riksbank or the “Riksbank”), and the market consensus (see Figure 1). Yet, the EUR/SEK currency pair has risen almost 1.8%* in the past month (SEK weakening), as accommodative monetary measures aimed at limiting Krona strength have been successful. However, at the last two monetary policy meetings, there have been increasing signs that members of the Riksbank’s Executive Board view further monetary easing as unnecessary, especially given the strong outperformance of the Swedish economy and the improving financial environment. Data due in the next three weeks1 will likely reaffirm these views and potentially reduce expectations of intervention. This may remove upward momentum for the EUR/SEK and potentially cause the pair to reverse recent gains.

(Click to enlarge)

Board members voice differing views

The Riksbank cut its benchmark interest rate to -0.5% in February and expanded its asset purchase programme by SEK45bn (US$4.8bn) at its April meeting. The measures were taken to ensure weakness of the Krona and reinforce its important contribution in helping lift inflation. At the last two meetings, Executive Board members have dissented when voting for additional monetary measures, or expressed a more conservative view as to the appropriate course of action. In the absence of a significant catalyst, further monetary measures to weaken the SEK are likely to be met with resistance, especially if upcoming growth and inflation data (due on the 30th May and 14th June respectively) surprise to the upside.

(Click to enlarge)

Resistance ahead

The EUR/SEK is moving towards the higher end of its recent 9.15-9.5 range. Should the pair approach its 2016 high of 9.5046* then it is likely that it will face resistance (see Figure 2). This is because at such levels the Krona weakness would sit in stark contrast to the significant outperformance of the Swedish economy relative to its European peers. In Q4 15, Sweden’s GDP growth was 4.5%*, almost three times that of the Euro Area over the same period.

Important Information

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

The information contained in this communication is for your general information only and is neither an offer for sale nor a solicitation of an offer to buy securities. This communication should not be used as the basis for any investment decision. Historical performance is not an indication of future performance and any investments may go down in value.

This document is not, and under no circumstances is to be construed as, an advertisement or any other step in furtherance of a public offering of shares or securities in the United States or any province or territory thereof. Neither this document nor any copy hereof should be taken, transmitted or distributed (directly or indirectly) into the United States.

This communication may contain independent market commentary prepared by ETFS UK based on publicly available information. Although ETFS UK endeavours to ensure the accuracy of the content in this communication, ETFS UK does not warrant or guarantee its accuracy or correctness. Any third party data providers used to source the information in this communication make no warranties or representation of any kind relating to such data. Where ETFS UK has expressed its own opinions related to product or market activity, these views may change. Neither ETFS UK, nor any affiliate, nor any of their respective officers, directors, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

ETFS UK is required by the FCA to clarify that it is not acting for you in any way in relation to the investment or investment activity to which this communication relates. In particular, ETFS UK will not provide any investment services to you and or advise you on the merits of, or make any recommendation to you in relation to, the terms of any transaction. No representative of ETFS UK is authorised to behave in any way which would lead you to believe otherwise. ETFS UK is not, therefore, responsible for providing you with the protections afforded to its clients and you should seek your own independent legal, investment and tax or other advice as you see fit.

Nyheter

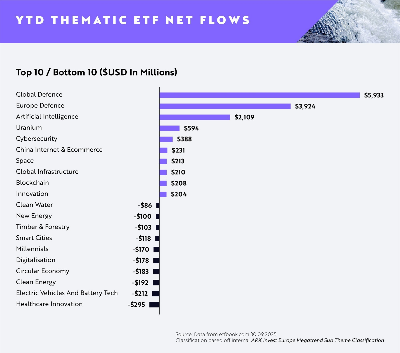

AI minskar gapet mot försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

Flödena av europeiska tematiska UCITS-ETFer fortsätter att öka uppåt i takt med att investerare dras mot högt övertygande megatrender, med AI (Artificiell Intelligens), försvar, energi (specifikt uran) och Kinas internet och e-handel alla i ledande positioner.

Viktiga punkter

- AI minskar gapet på försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

- Försvaret fortsätter att dominera under första till tredje kvartalet (+9,86 miljarder dollar)

- AI toppar nettoinflödena för augusti och september

Globala försvars-ETFer fortsätter att leda flödena hittills i år (YTD) med +5,93 miljarder dollar i nettoflöden, med europeiska försvars-ETFer på andra plats med +3,92 miljarder dollar i nettoflöden.

Emellertid har ETFer inom artificiell intelligens sett en anmärkningsvärd ökning i efterfrågan sedan slutet av första halvåret 2025, med dominerande inflöden under augusti och september för att nå nästan +2,11 miljarder dollar i nettoflöden hittills i dag. Detta motsvarar en ökning med cirka 133 % i nettoflöden sedan slutet av första halvåret jämfört med Global Defence på +23 % och European Defence på 29 %.

Investerarnas aptit för försvar är fortsatt stark då geopolitiska risker och moderna krigföringskrav driver strukturella medvindar för sektorn. Försvarsentreprenörer i framkant inom avancerad flyg- och rymdteknik, cybersäkerhet och drönarteknik tar en växande andel av de globala upphandlingsbudgetarna.

I Europa är allokeringarna fortfarande höga då regeringar över hela kontinenten reagerar på nya säkerhetsrealiteter med ökade utgiftsåtaganden. Investerare verkar fokuserade på lokala ledare med exponering mot underrättelsesystem, försvarselektronik och strategisk tillverkning.

Den ökade efterfrågan på ETFer inom artificiell intelligens visar att innovationstakten inom generativa modeller och företags-AI fortfarande är en viktig magnet för kapital. Investerare föredrar plattformar med skalbar AI-infrastruktur och exponering mot verkliga applikationer inom programvara, halvledare och robotteknik.

På andra håll rankades uran-ETFer på fjärde plats med +594 miljoner dollar i nettoflöden, medan cybersäkerhets-ETFer rankades på femte plats med +388 miljoner dollar. Båda teman fortsätter att attrahera kapital tack vare tydliga men hållbara drivkrafter: uran från den förnyade satsningen mot kärnkraft i övergången till ren energi och cybersäkerhet från eskalerande digitala hot och växande efterfrågan på motståndskraftig infrastruktur.

Rahul Bhushan, VD och global chef för investeringsprodukter på ARK Invest, kommenterade flödena: ”Investerare ompositionerar sig aktivt mot innovationsdrivna, strukturellt drivna teman i en föränderlig makromiljö. Med geopolitiska risker, genombrott inom generativa modeller och AI-ledd innovation uttrycker investerare starka åsikter om megatrender snarare än breda, odifferentierade exponeringar. Det är tydligt att tematiska ETFer inte längre bara är taktiska satsningar, de är centrala strategiska exponeringar.”

HANetfs Hector McNeil förklarar hur ETFer genererar hög avkastning med covered calls

JPEY ETF högavkastande företagsobligationer vautasäkrade till Euro

AI minskar gapet mot försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

XMME ETF – Levler MSCI EM by Xtrackers

34GI ETF bara eurodenominerade företagsobligationer med förfall 2024

De bästa lågvolatilitets ETFer på marknaden

Fokus mot en helt ny börshandlad produkt i september 2025

M5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

Could Bitcoin be the key to your dream house?

Börshandlade fonder för europeiska small caps

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCould Bitcoin be the key to your dream house?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanLevler noterar ytterligare fyra börshandlade fonder i Sverige

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanThe Investment Case for TLT (Long-Dated Treasury Bonds)

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMiners Find Their Mojo as Gold Consolidates