Nyheter

Investor Hedging Favours Gold

ETF Securities Commodity ETP Weekly Investor Hedging Favours Gold

Gold ETPs see three consecutive weeks of inflows.

Third consecutive week of inflows for industrial metals, led by ETFS Copper (COPA).

ETFS Wheat (WEAT) sees fifth consecutive week of inflows.

Profit-taking in oil ETPs for the eighth consecutive week.

Although Greece managed to scrape together its €750mn payment to the IMF, the fact it had to do so by tapping into its own IMF reserves account was a cause for concern. With its cash wearing so thin, the risk of an accident now is very high. Weaker-than-expected German Q1 GDP data, a downgrade of UK GDP forecast from the Bank of England and a string of poor Chinese data point to monetary easing from the world’s major central banks continuing for the foreseeable future. Gold responded decisively, jumping 3.2% on the week, while silver riding its coat-tail gained 6.4%.

Gold ETPs see three consecutive weeks of inflows. The recent rally in gold prices and rising market anxiety about Greece and European growth rates has driven heightened interest in gold. Last week we saw US$11.1mn of inflows into gold ETPs, adding to the US$62.3mn of cumulative inflows from the previous two weeks. World Gold Council data released last week showed only modest decline in gold demand in Q1 2015 relative to same period last year, with investment demand posting gains led by the ETP inflows.

Third consecutive week of inflows for industrial metals, led by ETFS Copper (COPA). COPA received US$4.8mn after the copper price has risen 7.6% in the past month as supply forecasts were revised down. The International Copper Study Group has for the past few years forecast supply surplus, when in reality the market has ended the year in a supply deficit. ICSG tend not to factor in the disruption to output from miner strikes, accidents and port closures. They have forecast a surplus in 2015 once again, but the recent flooding in Chile has already been a setback to global output.

ETFS Wheat (WEAT) sees fifth consecutive week of inflows. After wheat prices hit a five-year low two weeks ago, they bounced 7.7% last week. Investors have been steady building positions in wheat ETPs, bargain hunting as underlying prices remain depressed. Last week WEAT received US$3.7mn. With US farmers expecting to plant less of the grain this year, we expect supply to tighten. The near-perfect weather conditions we saw last year are unlikely to be repeated this year. In fact the Australian Bureau of Meteorology last week declared that we are currently in an El Niño weather event, which could be quite substantial in strength. El Niño weather events typically make countries like Australia and India more warm and dry than usual, potentially hurting their wheat crops.

Profit-taking in oil ETPs for the eighth consecutive week. Both Brent and WTI benchmarks rose 1.6% last week. Unsurprisingly, some ETP investors chose to take profit, seeing US$8.6mn of outflows. With OPEC announcing last week that it increased daily production by 18,000 barrel per day in April and the International Energy Agency claiming that OPEC’s battle for market share is ‘only just beginning’ the prospects for a correction in the 40% price rally since March seem high. Meanwhile, investors also took profit on a US natural gas ETPs after a 10% price rally last week. Natural gas surged following expectations of warmer US weather that would boost demand for the commodity to generate power for air-conditioning.

Key events to watch this week. US, Euro area and UK inflation numbers will be closely viewed to see if deflationary trends are abating. Continued price weakness should keep a central bank easing bias, which has been historically positive for gold.

Video Presentation

Nitesh Shah, Research Analyst at ETF Securities provides an analysis of last week’s performance, flow and trading activity in commodity exchange traded products and a look at the week ahead.

Important Information

This communication has been provided by ETF Securities (UK) Limited (”ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority.

- Trump’s crypto ally now leads the SEC, signaling the potential for a pro-crypto agenda

- Bitcoin isn’t just for HODLing anymore, thanks to Babylon

- The Dogecoin story: The emerging “intrinsic value”

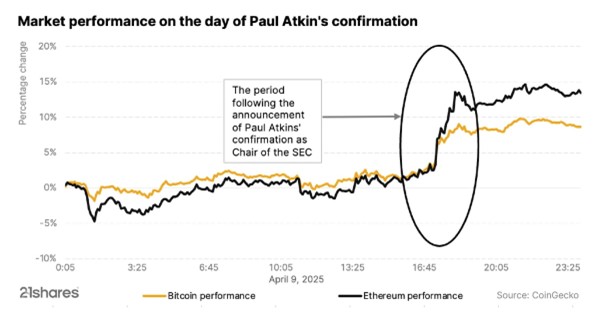

Trump’s crypto ally now leads the SEC, signaling the potential for a pro-crypto agenda

Paul Atkins’ appointment as SEC Chair marks a significant turning point for cryptocurrency regulation in the United States. The cryptocurrency market embraced him, with both Bitcoin and Ethereum rallying up to 9% and 14% respectively in the immediate aftermath. Given Atkins’ background in the crypto space, the industry has welcomed his confirmation and anticipates that he may expedite the approval of several pending projects.

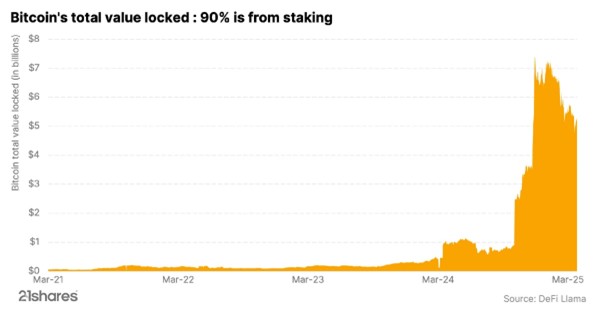

Bitcoin isn’t just for HODLing anymore, thanks to Babylon

Bitcoin is known for being one of the most secure blockchains out there. Now, a new project called Babylon is making waves by tapping into Bitcoin’s rock-solid security and bringing the staking feature to the Bitcoin world. Learn more about Bitcoin staking and its importance.

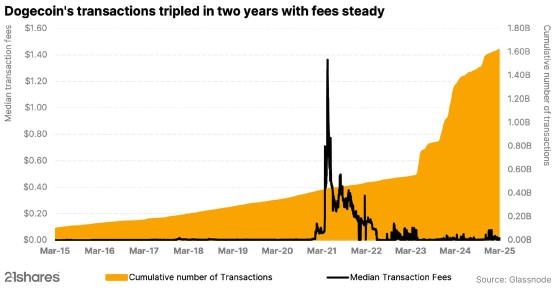

The Dogecoin story: The emerging “intrinsic value”

Dogecoin may have started as a meme, but it’s now a serious player in digital payments, offering fast, low-cost transactions to a passionate community driving real-world impact and innovation. The chart below underscores that real-world usage: it shows that cumulative transactions on the Dogecoin blockchain have surged over the past two years, effectively tripling in volume, all while transaction costs have remained remarkably low.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

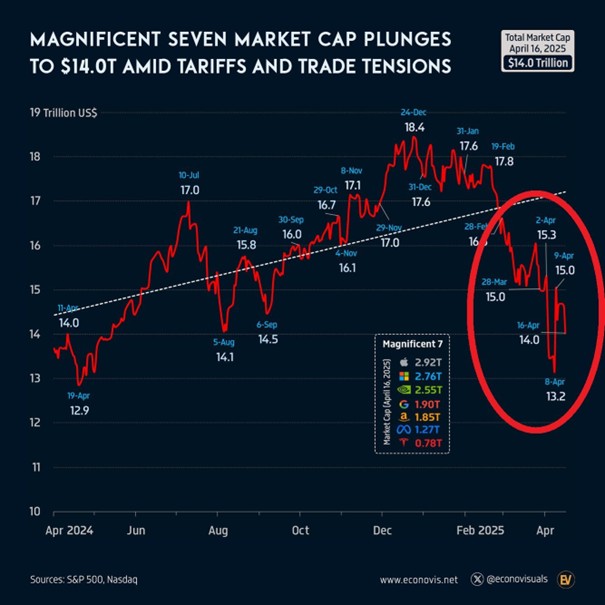

De amerikanska aktier som kollektivt går under namnet Mag7, också kända som Magnificent 7 aktierna har förlorat 4,4 biljoner dollar i marknadsvärde sedan toppen i december.

Detta är nästan dubbelt så mycket som värdet på den tyska aktiemarknaden. Dessa aktier återspeglar ~29 % av S&P 500-börsvärdet, en minskning från rekordhöga 34 %.

Vi skrev nyligen en artikel om tyska utdelningsaktier som du finner här

För den som letar efter investeringar i Tyskland klicka här

Källa: Global Markets Investor @GlobalMktObserv

A pro-crypto agenda is underway

SPFS ETF investerar i globala hälsovårdsföretag

Slakten av Magnificent 7 aktierna

RMPH ETC Ansvarsfullt fysiskt guld med GBP-säkring

Gold’s rally may signal what’s ahead for BTC

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Warren Buffetts råd om vad man ska göra när börsen kraschar

Svenskarna har en ny favorit-ETF

MONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV mars 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris