Nyheter

Insolvency Issues, Bitcoin Wholecoiners Surge, and More!

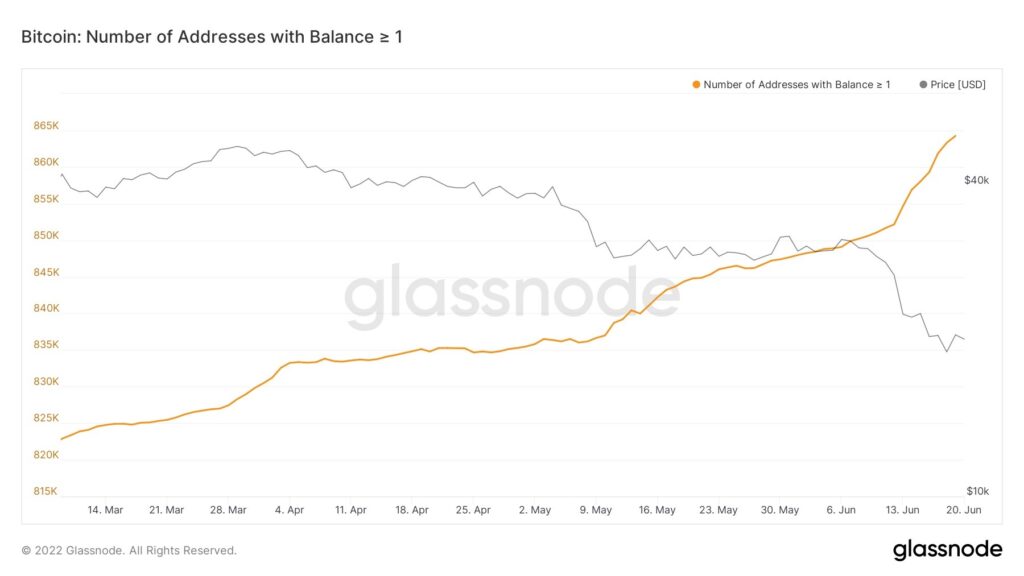

Soaring inflation and insolvency in some projects on DeFi sent Bitcoin briefly dipping below $18K over the weekend and Ethereum below $900. Jumping back to above the $20K and $1000 marks boosted some confidence in the market, with more than 13K wallets most likely “buying the dip” in the past week.

Figure 1: The Increase of Wallet Addresses Holding 1 BTC or More

Source: Glassnode

US President Joe Biden blamed the waging financial crisis on the fact that nine foreign-owned shipping companies have been raising prices since the pandemic, making profits seven times higher than the year before. On June 15, the Federal Reserve raised interest rates by 75 basis points; the biggest rate hike in 28 years. A day after, Biden signed the “Ocean Shipping Reform Act of 2022” to crack down on industry fees and reduce inflation, at least marginally.

Key Takeaways

• Celsius is under investigation in some US states

• Positive signals for Bitcoin’s correction

• Circle unveils euro-backed stablecoin

• The metaverse may generate up to $5T by 2030

• Ethereum delays difficulty bomb, a stepping stone to the Merge

Macro, Regulations; Spot, and Derivatives Markets

Illicit crypto activities between 2021 and the first quarter of 2022 have dropped from 0.6% to 0.1%, according to data gathered by a blockchain forensics company powered by Mastercard. CipherTrace estimates that in 2020, illicit activity was between 0.62% and 0.65% of overall crypto activity, and it has now fallen to between 0.10% and 0.15% of overall activity in 2021.

Regulators in the US were also quite active last week, running investigations and taking crypto companies to court. Here’s what happened:

• The Securities and Exchanges Commission (SEC) is reportedly investigating how major crypto exchanges are working to prevent insider trading on exchanges.

• Elon Musk, SpaceX, and Tesla were sued for an alleged Ponzi scheme to loot $258B in Dogecoin. The plaintiff is a Dogecoin investor seeking a class-action lawsuit in the Southern District of New York against Musk and his companies for at least $86B in damages.

• Texas, Alabama, and New Jersey are investigating Celsius Network’s decision to halt customer withdrawals, signalling the lending protocol’s probable insolvency.

On-chain Indicators

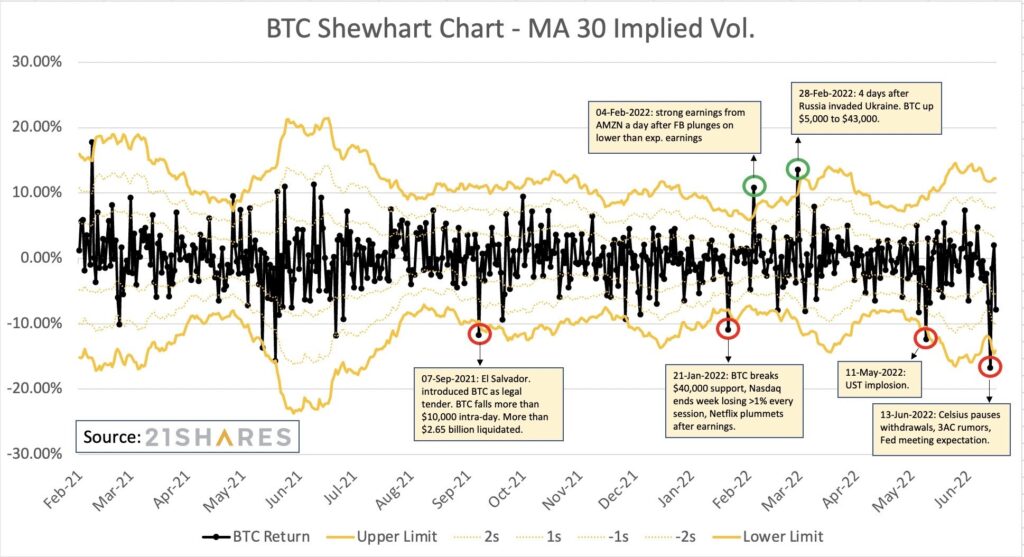

Figure 2: BTC Shewhart Chart – MA 30 Implied Volatility

Source: 21Shares

With lots of fear, uncertainty, and doubt going on about the dramatic downside of Bitcoin, our team put together a simple analysis using implied volatility (DVOL) and realized volatility to estimate the movement of BTC for the next 24 hours.

The incentive here is using the max DVOL level during major risk events in the last several weeks to estimate the probability of different movement levels. As tail risk is hard to quantify to the price level, this could give us some guidance on the movement.

Figure 3: Bitcoin’s Market Value to Realized Value Ratio

Source: Glassnode

As shown in Figure 3, the Market Value to Realized Value Ratio (MVRV) suggests that while Bitcoin may still experience price drops, it is more likely that the worst has passed. Over the past four years, Bitcoin’s MVRV ratio was above 1, with the exception of March 2020 when the MVRV ratio was 0.85 for seven days, in addition to the period between 2018 to 2019 which saw the MVRV ratio stay at 0.69 for 133 days. As shown, the current MVRV stands at 0.97.

DeFi

The Ethereum network will be undergoing an upgrade, dubbed the Gray Glacier, at block 15,050,000, which is expected to occur around June 29. The Gray Glacier will change the parameters of the Ice Age/Difficulty Bomb, pushing it back by 700,000 blocks, or roughly 100 days. More developments on the Ethereum ecosystem in the past week include:

• Former New York Stock Exchange president joined Uniswap Labs as an advisor.

• Inverse Finance suffered from a flash loan attack with $1.2M loss.

• Maker temporarily disabled Aave’s DAI Direct Deposit Module due to Celsius’ liquidity crisis.

• Bancor pauses Impermanent Loss Protection, to “give room for the protocol to breathe and recover.”

• Lido introduces dual governance, fearing Ethereum’s centralization after the Merge.

On the stablecoin hemisphere, Circle introduced an ERC-20 euro-backed stablecoin, EUROC. The Euro Coin will be backed by euro-denominated reserves held by regulated financial institutions in the US. The Euro Coin will be joining EURt, issued by Circle’s rival, Tether, which aims to decrease commercial paper backing of USDT to zero without any incurrences of losses. “All commercial papers are expiring and will be rolled into US Treasuries with a short maturity,” Tether’s announcement reads. Moreover, Tron DAO received 500M USDC to back its algorithmic stablecoin, USDD, which started to lose its peg to the dollar on June 13.

In a DeFi’s first, a lending protocol built on the Solana blockchain named Solend tried to gain control of a “whale” account which it said was putting the protocol at risk. Solend passed a proposal granting it emergency powers to take over the whale account, which had deposited 5.7M SOL tokens into Solend, accounting for more than 95% of deposits. Against that, the account was borrowing $108M in USDC and ETH. The measure would allow Solend to liquidate the whale’s assets via “over-the-counter” transactions — as opposed to on-exchanges trades — to avoid a possible cascade of liquidations. After a backlash on Twitter, questioning Solend’s decentralization, the lending protocol asked its users to vote on a new proposal to overturn the earlier vote, 99.8% voted yes.

NFTs, Metaverse, and DAOs

Amid the market crash, the top 8 NFT collections recorded at least 115% in the 24-hour trading volume. In a recent report, Mckinsey and Company predicted that the metaverse could reach $5 trillion by 2030.

In terms of developments on the metaverse, this is what we’ve seen last week:

• Merit Circle buys out the seed fund from YGG with $1.75M.

• Opensea is migrating to Seaport, which can reduce gascostst by 35%.

• IOTA announced the establishment of a DAO, with a community treasury of about $18.5M.

Hong Kong has emerged to be one of the popular regions for institutions including Meta and Yahoo to test out metaverse experiences. The potential catalyst is Animoca Brand, the mother company of the largest metaverse project Sandbox, which is incorporated in Hong Kong. We have seen many companies in Hong Kong entering Sandbox such as HSBC, Standard Chartered, SCMP, MTR, PCCW, among others.

More corporate NFT adoption include:

• YSL Beauty will launch social tokens and NFTs.

• Swiss luxury watchmaker TAG Heuer introduced an NFT-enabled smartwatch.

• Lacoste will launch an NFT collection.

Crypto Infrastructure

In the realm of crypto infrastructure layers, the L1 BNB Beacon Chain announced it’s going open-source, allowing developers to build on it. The network will also open its validator set, inviting external parties to become validators and play an important role in governance. Users interested in contributing as delegators will also have an avenue to contribute through staking. As the BNB Beacon Chain is rolled out, different components will be reviewed to identify opportunities for more prospective validators and delegators to contribute and play an active role.

The L2 zkSync will have a major version 2 update on testnet, featuring “forward-looking structural changes that necessitate a regenesis.” Immutable X is also launching Arch version 1.0, an NFT bridging protocol between L1 Ethereum and L2 StarkNet. Immutable is also launching a $500M fund to accelerate the adoption of Web 3 games and projects.

After a $400M liquidation by top-tier lenders on crypto trading and venture capital firm, Three Arrows Capital (3AC), it is speculated that 3AC is the next in line to be facing insolvency issues. With BlockFi and Deribit in its portfolio, 3AC has hired legal and financial advisers to help reclaim its position with lenders and other parties.

Moonbeam, a major destination for multi-chain applications on Polkadot, has integrated Chainlink Price Feeds into its smart contract platform. The availability of Chainlink’s price feeds helps enable builders to reliably source aggregated price information from many exchanges, helping ensure price accuracy. With the integration, developers can build even more sophisticated dApps to launch on the Moonbeam network.

One story we’re following in the realm of data storage is Filecoin Green’s $1 million grants program. It aims to support Regenerative Finance (ReFi) projects aiming to bring the economic system into a healthier alignment with the natural world.

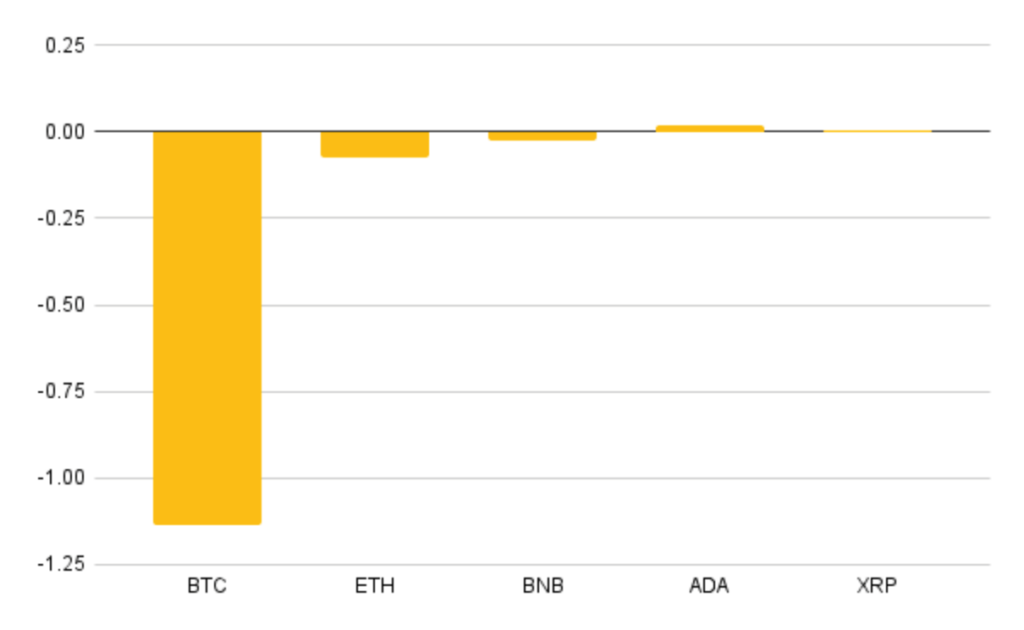

Weekly Returns

The returns of the top five cryptoassets over the last week were as follows — BTC (-1.14%), ETH (-0.07%), BNB (-0.03%), ADA (0.02%), XRP (0.003%)

Media Coverage

Ophelia Snyder was featured in Financial Times to quote her for some of her contributions on stage as a part of her participation in the ETF Conference. “Ophelia Snyder, co-founder and president of 21 Shares, the Swiss-based crypto funds group, believes acceptance of digital assets has already come a long way,” the article reads. Our newsletter has also been published on the MorningStar.

Our very own Tom Wan was featured on the Amun Podcast with Crian Padayachee to discuss the Terra Luna debacle. You can listen to the episode here.

News

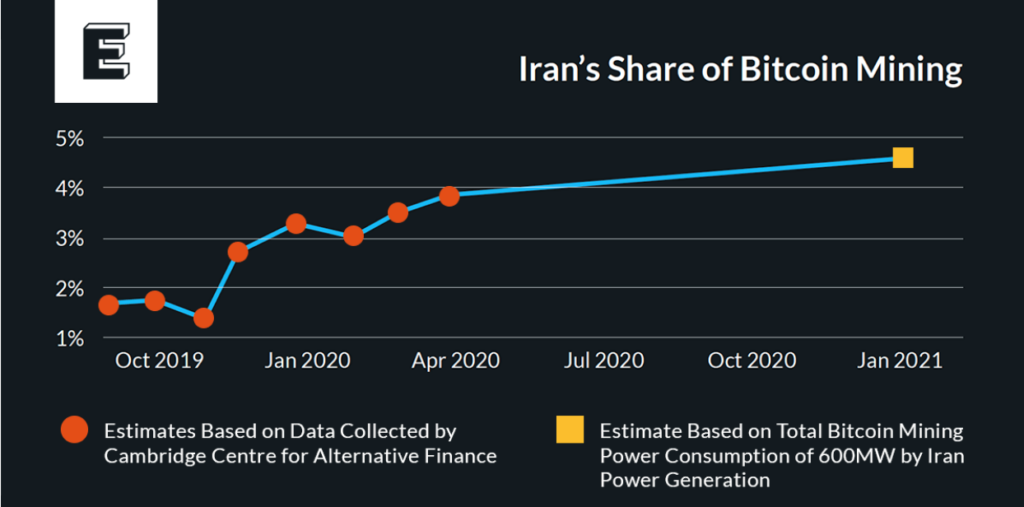

Iran Pulls the Plug on Bitcoin Miners this Week

What happened?

On the crypto mining front, 118 authorized cryptocurrency mining units in Iran will have to cut off their electricity supply from the national grid as of Wednesday, June 22. This is due to reaching a record of 62,500 megawatts during peak consumption, and it is expected that this week’s consumption will exceed 63,000 megawatts.

Why does it matter?

In December it was reported that Iran accounts for 4.5-7% of the global Bitcoin hashrate. Iran regulators officially recognized the crypto mining industry and began issuing licenses to miners, which are required to pay higher electricity rates and sell their mined Bitcoins to Iran’s central bank. However, the power infrastructure of the country couldn’t take it due to global warming.

In the coming months, we might see miners migrating to countries with abundant electric power resources, such as India, especially since the prices of new and used GPUs dropped in parallel with Bitcoin’s price developments over the past week.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

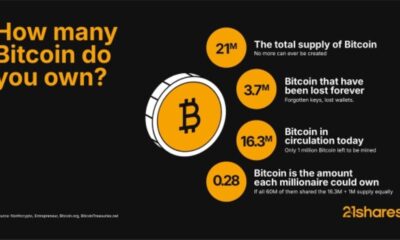

Even buying Bitcoin at its yearly peak since 2020 would still have doubled your investment, proving the power of long-term growth versus trying to time the market.

Why Solana matters: Exploring its use cases and growing adoption

Solana’s surge isn’t just market speculation; it’s driven by real-world adoption. From payments and DeFi to tokenization, the blockchain is seeing record engagement, reflected in its all-time high total value locked (TVL).

How Raydium and Jupiter are powering Solana DeFi

Raydium and Jupiter are the pillars of Solana’s DeFi ecosystem, delivering deep liquidity, seamless trading, and efficient execution that keep the network thriving. They make crypto markets faster, cheaper, and more accessible for everyone.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Time in Bitcoin beats timing Bitcoin

WMMV ETF en lågvolatilitetsfond som handlas i euro och pund

UBS AM lanserar UBS Treasury Yield Plus ETFer

COINUNI ETP spårar kryptovalutan Uniswap

ETF- och ETP-noteringar den 16 september 2025: nytt på Xetra och Börse Frankfurt

Utdelningar och försvarsfonder lockade i augusti

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

ADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

Septembers utdelning i XACT Norden Högutdelande

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSeptembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV augusti 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf kommenterar mötet mellan Kina, Ryssland och Nordkorea vid militärparad

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanAICT ETF investerar i obligationer utgivna av företag från tillväxtmarknader