Nyheter

How are investors using gold?

![36% of 800 professional investors surveyed by WisdomTree noted ‘diversification’ as their primary reason for holding gold[1]. Our analysis shows that gold has a low correlation with both equities and bonds and, thus, should contribute strongly to a diversification effort.](https://media.etfmarknaden.se/2025/01/Wisdomtree.jpg)

36% of 800 professional investors surveyed by WisdomTree noted ‘diversification’ as their primary reason for holding gold[1]. Our analysis shows that gold has a low correlation with both equities and bonds and, thus, should contribute strongly to a diversification effort.

Figure 1: Correlations between assets

| Commodity | MSCI World All Country | S&P 500 | Global Aggregate Bond | Gold | |

| Commodity | 1.00 | ||||

| MSCI World All Country | 0.43 | 1.00 | |||

| S&P 500 | 0.33 | 0.94 | 1.00 | ||

| Global Aggregate Bond | 0.24 | 0.36 | 0.27 | 1.00 | |

| Gold | 0.37 | 0.12 | 0.02 | 0.41 | 1.00 |

Source: Bloomberg, WisdomTree, Monthly data from November 1990 to November 2024. Commodity is Bloomberg Commodity Index, MSCI World All Country is a equity index, S&P 500 is a US equity index, Global Aggregate Bond is the Bloomberg GlobalAgg Index covering government, corporate and securitized fixed income, Gold is spot gold prices. Historical performance is not an indication of future performance and any investments may go down in value.

Gold behaves very differently to other assets. On the one hand, it is a defensive asset, often competing with bonds as a safe harbour against broader market volatility. On the other hand, it has cyclical traits because it rises in times of inflation, which is often generated in periods of strong economic growth. This duality of gold helps explain its low correlation with traditional assets.

Our survey respondents flagged ‘inflation hedge’ as the second most popular reason to hold gold (35%), followed by ‘financial market volatility hedge’ (31%) and ‘geopolitical volatility hedge’ (27%)[2].

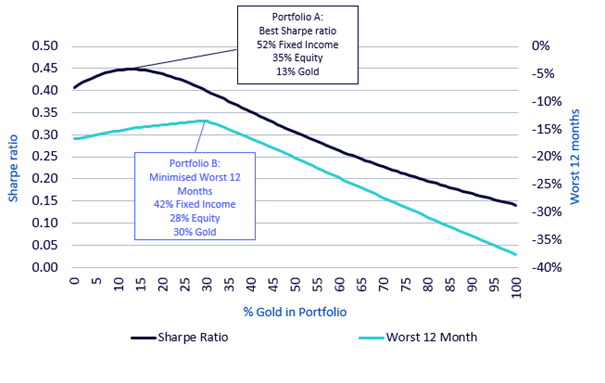

Optimal holding of gold in a portfolio

Putting gold into a portfolio of other assets can increase a portfolio’s Sharpe ratio[3] and reduce worst 12-month performances[4]. We illustrate with an example based on data from 1973 to 2024.

- We start with a portfolio of bonds (60%) and equities (40%) and no gold: that is the 0 point on the horizontal axis. The Sharpe ratio of this portfolio is 0.41 and the worst 12-month performance is -17%.

- As we move along the horizontal axis we introduce some gold to the portfolio. The remainder of the portfolio maintains a 60/40 ratio of bonds to equities.

- As we increase gold holdings, Sharpe ratios rise and worst 12-month performances decline, up to a point (before they deteriorate again).

- The maximum Sharpe ratio (portfolio A) is achieved with 13% gold (where the remainder of the portfolio is 52% bonds and 35% equities). The Sharpe ratio is 0.45 in this portfolio.

- The minimum worst 12-month performance (portfolio B) is achieved with 30% gold (where the remainder of the portfolio is 42% bonds and 28% equities). The worst 12-month performance is -13% in this portfolio.

Figure 2: Optimal gold holdings

Source: WisdomTree, Bloomberg. Period January 1973 to September 2024. Calculations are based on monthly returns in USD. The portfolio is rebalanced semi-annually. Equities are proxied by the MSCI World Gross Total Return Index and Fixed Income is proxied by the Bloomberg Barclays US Treasury Total Return Index. You cannot invest directly in an index. Above numbers include backtested data. Historical performance is not an indication of future performance and any investments may go down in value.

Our survey indicates that the mean average holding of gold is only 5.42%[5], well below the optimal to maximise the Sharpe ratio. In fact, less than 14% of investors surveyed[6] hold enough gold to maximise their Sharpe ratio (assuming equities and bonds are the mainstay of their portfolio).

Hedging risks

We established that investors hold gold to hedge various risks, but what is the market’s perception of those risks today and how could they evolve?

Financial market risks

Several metrics gauge market anxiety, including the VIX[7] and MOVE[8] alongside direct investor surveys. At present, none of these measures indicate immediate concern. However, risks can escalate rapidly, as seen in August 2024, when a yen carry trade unwind sparked fears across global financial markets.

With various equity indices reaching all-time highs—and concerns that these gains are heavily concentrated—many investors are seeking ways to hedge against a potential market reversal. Gold serves as a key tool in this context.

Economic risks

The global economy has shown resilience through the past cycle, with the likelihood of a recession in the next year considered low[9]. However, policy uncertainty remains a significant concern for many investors.

In the United States, a new administration has risen to power with a strong focus on trade policies. Should President-Elect Trump impose new tariffs, rather than using them as negotiation tools, it could pose challenges to global economic growth. In this scenario, gold may become a preferred asset for hedging these risks.

Geopolitical risks

Throughout 2024, gold prices were supported by heightened geopolitical tensions. The Russia-Ukraine war and the Israel-Hamas/Hezbollah conflicts dominated investor concerns. More recently, the fall of the Assad regime in Syria has created uncertainty, particularly for Russia, a key ally of Assad. Russia’s military bases in Syria now face an uncertain future, raising concerns about potential escalations.

In November 2024, Ukraine’s use of US and UK-supplied long-range missiles prompted retaliatory strikes from Russia. Coupled with amendments to Russia’s nuclear doctrine, fears of further escalation remain.

President-Elect Trump has promised a swift resolution to the Russia-Ukraine conflict. However, achieving this without significant concessions from Ukraine and NATO seems unlikely, suggesting that geopolitical risks may persist.

Iran, another key supporter of the Assad regime, faces a similarly precarious situation. The weakening of Hamas, Hezbollah, and the Assad alliance undermines Iran’s regional influence. Additionally, the US may enforce sanctions against Iran more rigorously, which could prompt unpredictable responses from Tehran.

Despite speculative positioning in gold futures slipping slightly—from over 300,000 contracts net long in early October 2024 to just below that level today—the ongoing geopolitical tensions may drive positioning higher once again.

Conclusions

Professional investors rightly view gold as a hedge against inflation, financial market turbulence, economic stress, and geopolitical chaos. While some of these risks may not be at the forefront of investors’ concerns today, hedging against the potential escalation of tail risks remains highly valuable.

We also align with the surveyed investors’ belief that gold serves as an excellent portfolio diversifier. Our analysis confirms that incorporating gold into a portfolio enhances overall outcomes, improving returns while effectively managing risk.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

[1] WisdomTree Pan European Professional Investor Survey, June-July 2024, 800 respondents, conducted by Censuswide.

[2] Ibid.

[3] The Sharpe ratio compares the return of an investment with its risk. It’s a mathematical expression of the insight that excess returns over a period of time may signify more volatility and risk, rather than investing skill.

[4] Similar risk concept to drawdowns but rather than look at peak to trough performance, we look at fixed 12-month declines.

[5] WisdomTree Pan European Professional Investor Survey, June-July 2024, 800 respondents, conducted by Censuswide.

[6] Ibid.

[7] The Chicago Board Options Exchange’s CBOE Volatility Index (VIX) is a market-implied measure of the volatility of the US equity market.

[8] Merrill Lynch Option Volatility Estimate (MOVE) index is a market-implied measure of the volatility of the US bond market.

[9] Bloomberg’s November/December surveys of professional economists shows the following (average) recession probabilities: US 25%; Euro Area 30%; China 10%; Japan 30%; UK 30%.

![WisdomTree, en global finansiell innovatör, meddelade idag att deras europeiska ETF[3] och ETP-sortiment har nått 50 miljarder dollar i förvaltat kapital, vilket markerar en viktig milstolpe i deras tillväxtbana. Prestationen understryker styrkan i WisdomTrees UCITS-plattform, deras ledarskap inom guld och råvaror, och deras position som en pionjär inom krypto-ETPer. Globalt förvaltar WisdomTree över 140 miljarder dollar, över olika tillgångsslag, för investerares räkning.](https://media.etfmarknaden.se/2025/10/50-400x240.jpg)

![WisdomTree, en global finansiell innovatör, meddelade idag att deras europeiska ETF[3] och ETP-sortiment har nått 50 miljarder dollar i förvaltat kapital, vilket markerar en viktig milstolpe i deras tillväxtbana. Prestationen understryker styrkan i WisdomTrees UCITS-plattform, deras ledarskap inom guld och råvaror, och deras position som en pionjär inom krypto-ETPer. Globalt förvaltar WisdomTree över 140 miljarder dollar, över olika tillgångsslag, för investerares räkning.](https://media.etfmarknaden.se/2025/10/50-80x80.jpg)

Nyheter

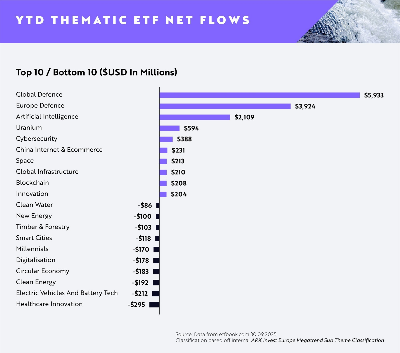

AI minskar gapet mot försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

Flödena av europeiska tematiska UCITS-ETFer fortsätter att öka uppåt i takt med att investerare dras mot högt övertygande megatrender, med AI (Artificiell Intelligens), försvar, energi (specifikt uran) och Kinas internet och e-handel alla i ledande positioner.

Viktiga punkter

- AI minskar gapet på försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

- Försvaret fortsätter att dominera under första till tredje kvartalet (+9,86 miljarder dollar)

- AI toppar nettoinflödena för augusti och september

Globala försvars-ETFer fortsätter att leda flödena hittills i år (YTD) med +5,93 miljarder dollar i nettoflöden, med europeiska försvars-ETFer på andra plats med +3,92 miljarder dollar i nettoflöden.

Emellertid har ETFer inom artificiell intelligens sett en anmärkningsvärd ökning i efterfrågan sedan slutet av första halvåret 2025, med dominerande inflöden under augusti och september för att nå nästan +2,11 miljarder dollar i nettoflöden hittills i dag. Detta motsvarar en ökning med cirka 133 % i nettoflöden sedan slutet av första halvåret jämfört med Global Defence på +23 % och European Defence på 29 %.

Investerarnas aptit för försvar är fortsatt stark då geopolitiska risker och moderna krigföringskrav driver strukturella medvindar för sektorn. Försvarsentreprenörer i framkant inom avancerad flyg- och rymdteknik, cybersäkerhet och drönarteknik tar en växande andel av de globala upphandlingsbudgetarna.

I Europa är allokeringarna fortfarande höga då regeringar över hela kontinenten reagerar på nya säkerhetsrealiteter med ökade utgiftsåtaganden. Investerare verkar fokuserade på lokala ledare med exponering mot underrättelsesystem, försvarselektronik och strategisk tillverkning.

Den ökade efterfrågan på ETFer inom artificiell intelligens visar att innovationstakten inom generativa modeller och företags-AI fortfarande är en viktig magnet för kapital. Investerare föredrar plattformar med skalbar AI-infrastruktur och exponering mot verkliga applikationer inom programvara, halvledare och robotteknik.

På andra håll rankades uran-ETFer på fjärde plats med +594 miljoner dollar i nettoflöden, medan cybersäkerhets-ETFer rankades på femte plats med +388 miljoner dollar. Båda teman fortsätter att attrahera kapital tack vare tydliga men hållbara drivkrafter: uran från den förnyade satsningen mot kärnkraft i övergången till ren energi och cybersäkerhet från eskalerande digitala hot och växande efterfrågan på motståndskraftig infrastruktur.

Rahul Bhushan, VD och global chef för investeringsprodukter på ARK Invest, kommenterade flödena: ”Investerare ompositionerar sig aktivt mot innovationsdrivna, strukturellt drivna teman i en föränderlig makromiljö. Med geopolitiska risker, genombrott inom generativa modeller och AI-ledd innovation uttrycker investerare starka åsikter om megatrender snarare än breda, odifferentierade exponeringar. Det är tydligt att tematiska ETFer inte längre bara är taktiska satsningar, de är centrala strategiska exponeringar.”

HANetfs Hector McNeil förklarar hur ETFer genererar hög avkastning med covered calls

JPEY ETF högavkastande företagsobligationer vautasäkrade till Euro

AI minskar gapet mot försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

XMME ETF – Levler MSCI EM by Xtrackers

34GI ETF bara eurodenominerade företagsobligationer med förfall 2024

De bästa lågvolatilitets ETFer på marknaden

Fokus mot en helt ny börshandlad produkt i september 2025

M5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

Could Bitcoin be the key to your dream house?

Börshandlade fonder för europeiska small caps

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCould Bitcoin be the key to your dream house?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanLevler noterar ytterligare fyra börshandlade fonder i Sverige

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanThe Investment Case for TLT (Long-Dated Treasury Bonds)

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMiners Find Their Mojo as Gold Consolidates