Nyheter

Geopolitical risks drove ETP flows last week

Nyheter

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

Nyheter18 timmar sedan

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

Nyheter19 timmar sedan

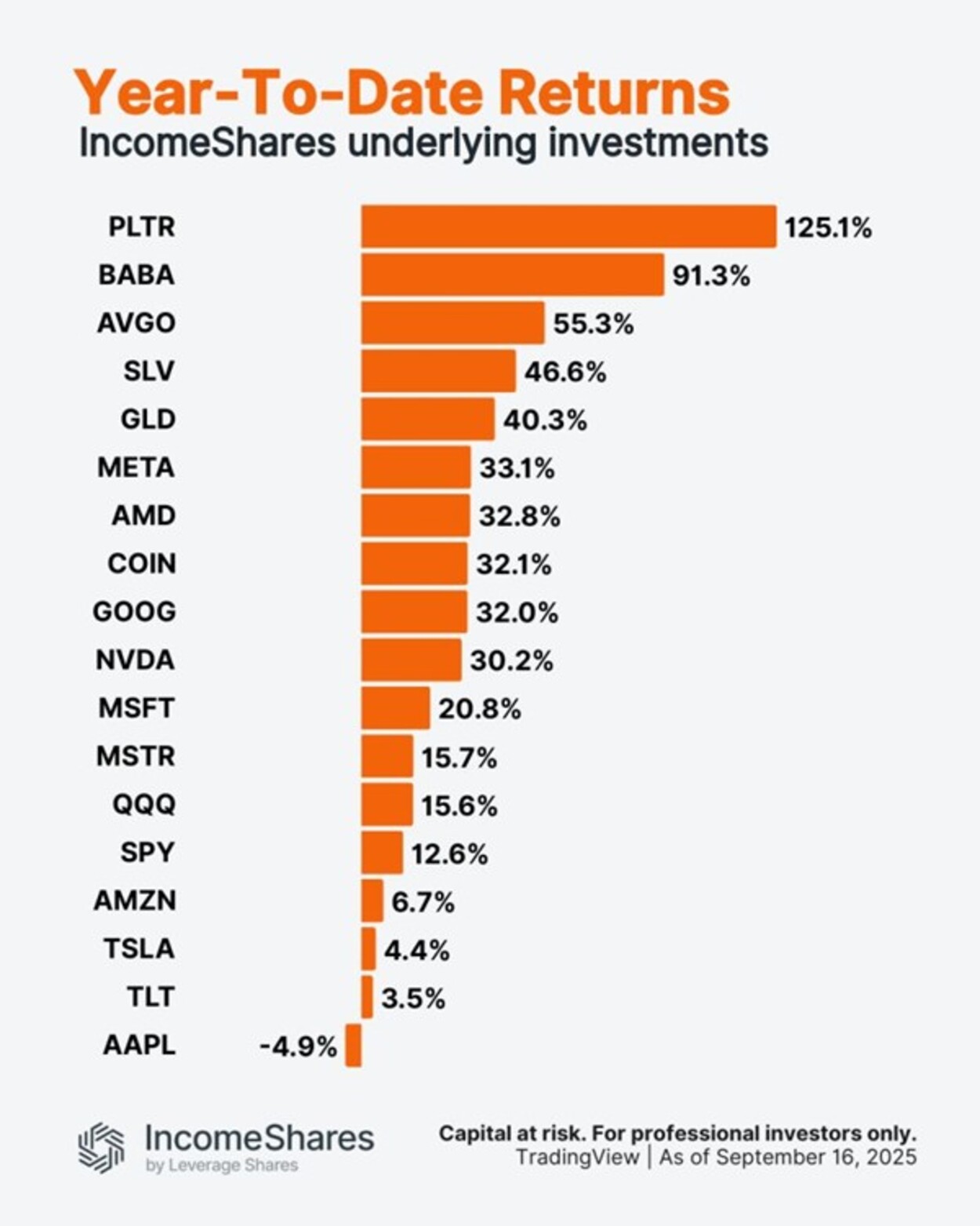

Palantir är upp 125 % i år. Apple är ner 5 %.

Nyheter20 timmar sedan

Utforska framtiden för AI och DeFi

Nyheter21 timmar sedan

ONCC ETP spårar den schweiziska dagslåneräntan

Nyheter22 timmar sedan

HANetf kommenterar kopparuppgången

Nyheter3 veckor sedan

Utdelningar och försvarsfonder lockade i augusti

Nyheter4 veckor sedan

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

Nyheter4 veckor sedan

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

Nyheter4 veckor sedan

ADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

Nyheter2 veckor sedan

Septembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSeptembers utdelning i XACT Norden Högutdelande

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV augusti 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf kommenterar mötet mellan Kina, Ryssland och Nordkorea vid militärparad

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAICT ETF investerar i obligationer utgivna av företag från tillväxtmarknader