Nyheter

Flat Inflation and Decentralizing Ethereum’s Layer 2

• The Road Towards Decentralizing Ethereum’s Scaling Solutions

• Flat Inflation, Flat Bitcoin

• TON’s Meteoric Rise Powered by Telegram

Flat Inflation, Flat Bitcoin

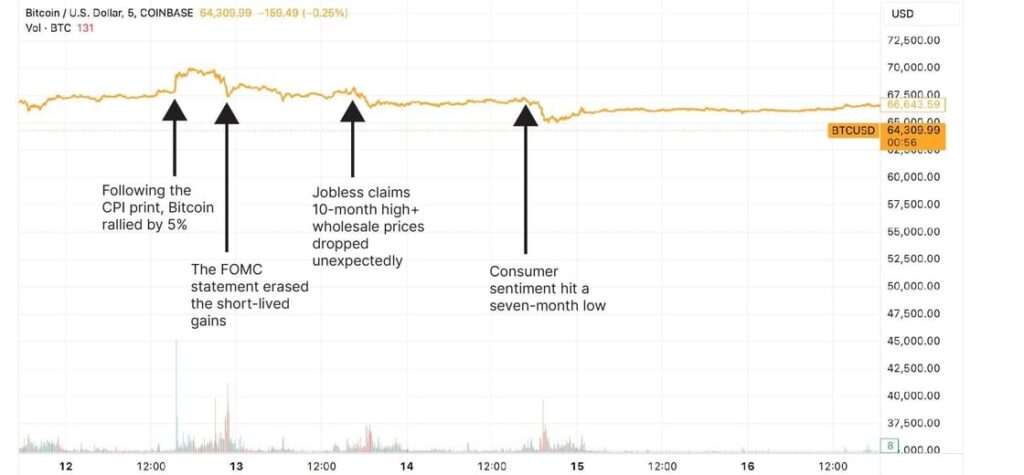

Inflation in the U.S. slowed in May but not enough to prompt the Fed to cut rates. The Consumer Price Index (CPI) was unchanged month-over-month, rising 3.3% over the year, slightly below expectations of 3.4%. Following the CPI release, Bitcoin briefly surged 5% to near $70K before erasing gains after a hawkish Federal Open Market Committee (FOMC) statement.

The Producer Price Index (PPI) dropped by 0.2% in May, the largest decline since October 2023. Unemployment claims rose to a 10-month high, increasing from 229K to 242K, against an expected decline. These indicators suggest cooling inflation, even though there is more work to be done to reach the Fed’s 2% target. Bitcoin has mostly traded sideways over the past three months. Despite recent news and its rejection from the $70K level, investors should remember that its fundamentals remain strong. Institutional adoption, regulatory shifts, and its emerging role as a store of value, particularly in struggling economies, underscore its potential long-term trajectory.

Figure 1 – How Bitcoin Reacted to Last Week’s U.S. Macroeconomic Indicators

Source: TradingView, 21Shares

TON’s Meteoric Rise Powered by Telegram

The Open Network (TON) blockchain was initially developed by the Durov brothers of Telegram. Despite the regulatory hurdles leading Telegram to step back, the TON Foundation continues to innovate, making TON one of the most user-friendly decentralized platforms. TON’s close relationship with Telegram has been pivotal and a testament to the power of integrating social media with blockchain technology.

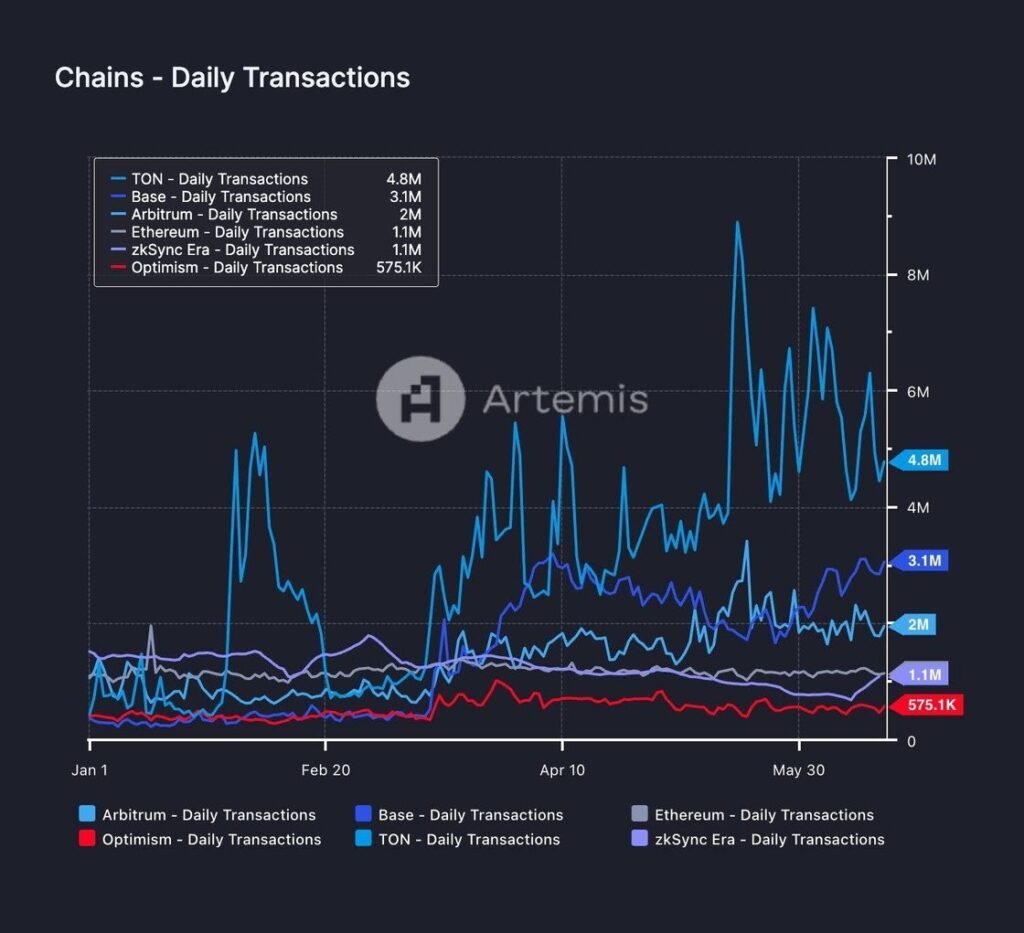

2024 has been a landmark year for TON, witnessing unprecedented growth and achieving multiple all-time highs, reaching just above $8 on June 14 and currently up 238% year-to-date. On top of that, TON has grown by over 4000% in total value locked this year to over $550M. TON’s growing dominance is further highlighted by TON surpassing Ethereum mainnet in daily active users, currently housing over 440K, almost 50K more than the smart contract platform giant. Even more impressively, TON currently processes almost 5M daily transactions, more than Ethereum and any of its scaling solutions!

Figure 2: The Growth of TON’s Daily Number of Transactions

Source: Artemis

The integration with Telegram, which boasts almost a billion users, has been a key driver of this success, offering its existing network a user-friendly interface to interact with the Web3 ecosystem, with several key features fueling TON’s meteoric rise. For example, Telegram Stars has played a crucial role in TON’s expansion. This initiative promotes TON-based applications directly within Telegram, allowing users to pay for digital services via in-app purchases. Furthermore, the initiative allows app developers to swap their stars for TON and subsidize their advertisements on the platform, making application development on Telegram more economically viable. Another important feature was the unveiling of a revenue-sharing system in Telegram, allowing channel owners to get 50% of revenue from ads displayed on their channel, paid out in TON, thereby bolstering user engagement and adoption.

A major driver of TON’s growth is its mini-app ecosystem within Telegram. This ecosystem includes a variety of applications designed to enhance user engagement and streamline blockchain interactions. For instance, Notcoin, a click-to-mine Web3 game, has garnered over 35 million sign-ups, demonstrating the platform’s ability to attract and retain a large user base. Additionally, the integration of Wallet, a TON-based platform with over 2.5 million users, has made managing digital assets as simple as using social media. Wallet’s seamless onboarding allows users to handle their assets directly within Telegram Messenger, and with TON Connect, it enables smooth communication between Wallet and other apps in the TON ecosystem, significantly lowering the barriers to entry.

TON’s serves as a gateway to onboard new user cohorts into the blockchain world, allowing direct interaction with Web3 systems while eliminating the need for users to navigate complex crypto infrastructures. This model echoes the success of WeChat, China’s leading super-app with over a billion active users, which integrates messaging, social media, and financial services seamlessly. Similarly, if TON onboards just half the user base of Telegram over the next few years, then it could contribute to doubling almost all crypto users, standing around 550M. Finally, the growth of TON highlights the significant impact of their approach, evidenced by TON eclipsing Ethereum in daily activity. However, it’s important to note that over 80% of Ethereum’s transactions now occur on its Layer 2 solutions, highlighting the evolving nature of its infrastructure towards a more modular framework. This dual-layer approach underscores the continuing innovation and adaptability within the blockchain space, with TON setting a new standard for accessibility and engagement.

The Road Towards Decentralizing Ethereum’s Scaling Solutions

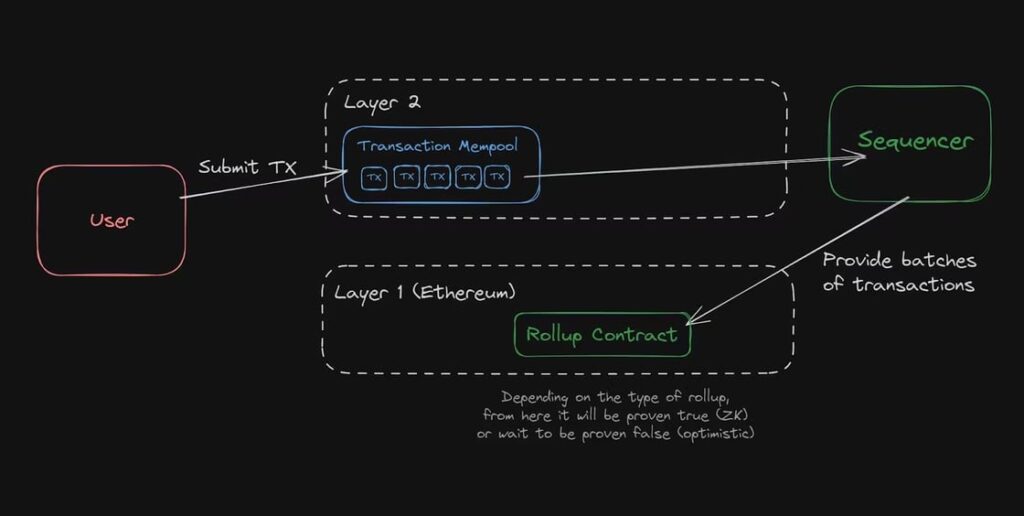

Arbitrum and Optimism, the two leading Ethereum scaling solutions, released key technical upgrades to address the lack of decentralization on the Layer 2 level. To grasp the significance of these upgrades, it is essential first to examine the fundamental differences in transaction processing between Ethereum and its scaling solutions.

Ethereum has over a million validators, which ensure that if a suspicious transaction is submitted by a dishonest operator, other validators can check for fraudulent activity by cross-checking it against their own ledger copies. If the transaction doesn’t conform to the network’s state, it’s rejected and doesn’t get included in the blockchain. This decentralized architecture makes it less likely for a single entity to control the network, increasing its resilience to attacks and censorship attempts.

In contrast, Ethereum’s scaling solutions typically rely on a single validator (sequencer) to aggregate transactions on the L2 and post them on Ethereum for settlement, thereby boosting efficiency by allowing for faster and cheaper processing. Despite their largely centralized approach, users can still dispute transactions through fraud proofs, a feature that some networks have only now started to adopt. We’ll delve deeper into this aspect next.

Figure 3: The Flow of Transaction Between L2s and Ethereum

Source: Jarrodd Watts

While this setup increases Ethereum’s throughput, it reintroduces a significant issue the industry sought to overcome: a single point of failure. This problem was starkly illustrated by the recent exploit on Linea, a prominent L2 network. The hack targeted Velocore, a leading decentralized exchange (DEX) on the network, leading the attacker to withdraw approximately $2.6M before the network’s foundation halted block production. By shutting down the sole sequencer, the network effectively censored transactions. Although the action was taken to minimize damage to Velocore’s users, the event highlighted the poor decentralization of Ethereum’s scaling solutions, which can be easily shut down by a single entity. Thus, the recent technical upgrade released by the Optimism and Arbitrum teams came at a critical time.

Namely, Optimism released the long-anticipated fraud-proof system. A dispute-resolution mechanism allowing any user to contest the validity of transactions submitted by Optimism’s foundation sole sequencer. Before this upgrade, a security council made up only of chosen respected members of the broader Ethereum ecosystem operated on a multi-signature system that had the power to approve upgrades and contest transaction validity if they thought it was fraudulent. However, anyone can now participate in contesting transactions, while the security council will remain intact and intervene in emergencies if needed for the foreseeable future. Similarly, Arbitrum proposed to launch its Bounded Liquidity Delay (BOLD) solution. This permissionless dispute resolution mechanism enables anyone to contest the validity of transactions submitted by the sequencer, similar in principle to Optimism’s fraud-proof system. The main difference for Arbitrum is that the network will no longer rely on a security council, thus effectively becoming the most decentralized L2 across the entire Ethereum scaling ecosystem.

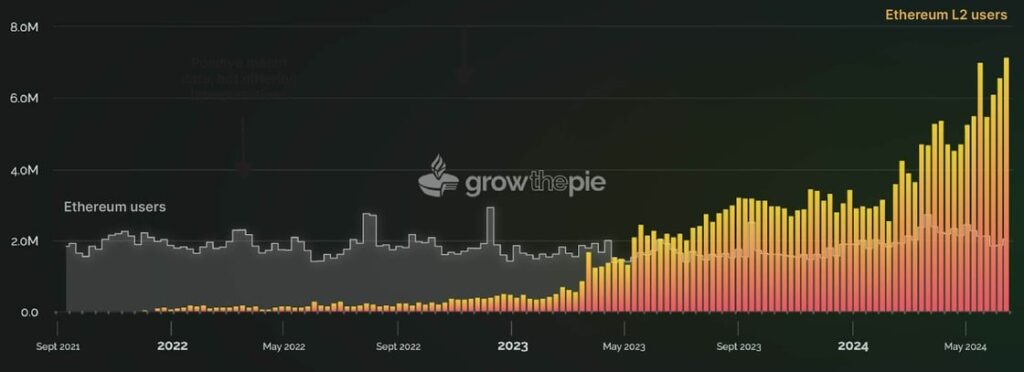

All in all, despite Linea’s hack that exposed the Achilles heel of the scaling solutions security, Layer 2 networks now account for nearly 80% of Ethereum’s transactional activity. Moreover, they have just collectively achieved a milestone of 256 TPS, underscoring the urgent need to bolster the resilience and robustness of Ethereum’s infrastructure as scaling solutions become increasingly vital to the network.

Figure 4: The Growth of Ethereum’s Ecosystem Users

Source: GrowThePie

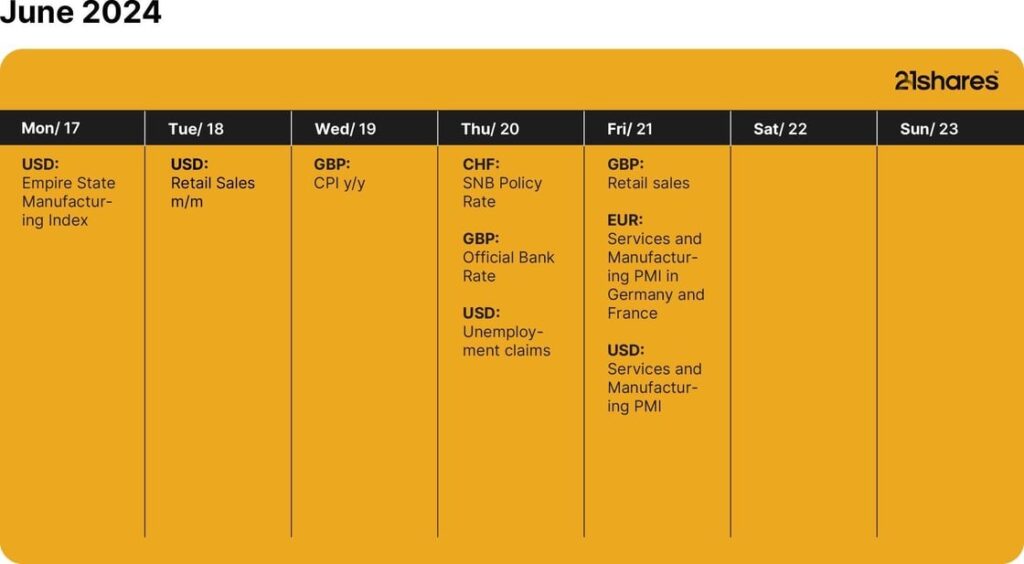

This Week’s Calendar

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Stablecoins are digital currencies tied to assets like the U.S. dollar, offering the price stability needed for payments. They maintain their peg by being backed 1:1 by their underlying fiat currency, with issuers holding equivalent amounts in cash and cash equivalents, making stablecoins a digital representation of those reserves. Their market has doubled to over $235 billion, with daily usage nearly doubling in two years.

Why are stablecoins making headlines now?

Due to their clear product-market fit and growing mainstream adoption, stablecoins have become a top priority for regulation, with both industry leaders and policymakers calling for swift action.

On April 4, the Securities and Exchange Commission’s Division of Corporation Finance finally clarified that stablecoins are not securities if backed one-for-one by USD or similar assets and used for payments or value storage. These “Covered Stablecoins” are not marketed as investments, lack profit incentives, and include protections like reserves, making securities law registration unnecessary for issuance or redemption.

The GENIUS Act, introduced in February and advanced by the U.S. Senate Banking Committee in March, marks a major step toward creating a clear legal framework for stablecoin issuance and oversight. This clarity is driving momentum as Fidelity is set to launch its own stablecoin, and Bank of America is preparing to follow it once legislation is finalized.

Globally, the European Union’s Markets in Crypto Assets (MiCA) framework has already come into effect, reinforcing a broader shift toward formal integration of stablecoins into traditional finance. These developments reflect a growing consensus that stablecoins are emerging as essential infrastructure for global payments, treasury management, and digital asset adoption.

What are the benefits of stablecoins?

Stablecoins are digital currencies designed for fast, low-cost, and stable transactions. Since their launch in 2014, they’ve become a go-to tool for online payments, especially cross-border transfers. As they’re pegged to stable assets like the U.S. dollar or euro, they avoid the wild price swings seen in other cryptocurrencies.

They’re accessible to anyone with internet, making them especially valuable in regions with high inflation or limited banking access, like Argentina or Turkey.

With some built on public blockchains, stablecoins offer transparency, letting users track transfers and supply in real time. For institutions, they also simplify treasury management by acting as efficient digital cash that can be deployed instantly.

Who are the major players in the stablecoin race?

Tether (USDT) and Circle (USDC), the two largest stablecoin issuers, collectively hold over $204 billion in U.S. Treasuries, making them the 14th largest holders globally. Their combined treasury holdings surpass those of entire nations, including Norway and Brazil.

USDT leads with $144 billion in circulation; USDC, backed by Coinbase and known for compliance, has become a trusted digital dollar across global finance.

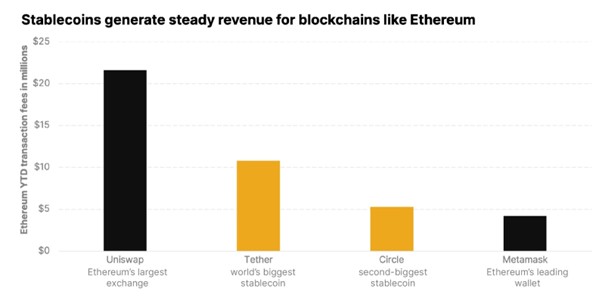

Why stablecoins matter: A revenue engine for blockchains

Stablecoins generate steady revenue for blockchains like Ethereum and Solana by driving transaction fees with each transfer. With trillions in annual volume, they help sustain network activity beyond speculation.

On Ethereum, for example, USDT and USDC transactions are major contributors to daily gas fees. Year to date, Tether ranks #3 and USDC ranks #5 in terms of total gas consumed. Tether and Circle also dominate daily transaction activity on Ethereum, averaging approximately 12 million and 6 million transactions per day, respectively, making them the top two entities on the network by daily transaction count.

Meanwhile, on Solana, stablecoin activity has surged, helping sustain validator rewards and strengthen protocol economics. In addition to the mainstream utility, stablecoins represent reliable, protocol-level cash flow, making them crypto’s killer use case.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Stablecoins: The real powerhouse of crypto

BE29 ETF är en portfölj företagsobligationer med förfall 2029

Guld-ETFer slår Bitcoin-ETFer kraftigt under första kvartalet 2025

INGH ETF är en satsning på global infrastruktur

SPFT ETF är en global satsning på teknikföretag

Fonder som ger exponering mot försvarsindustrin

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Warren Buffetts råd om vad man ska göra när börsen kraschar

Svenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV mars 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSju börshandlade fonder som investerar i försvarssektorn