Nyheter

Crypto’s Back in the Green; Are We Out of the Woods?

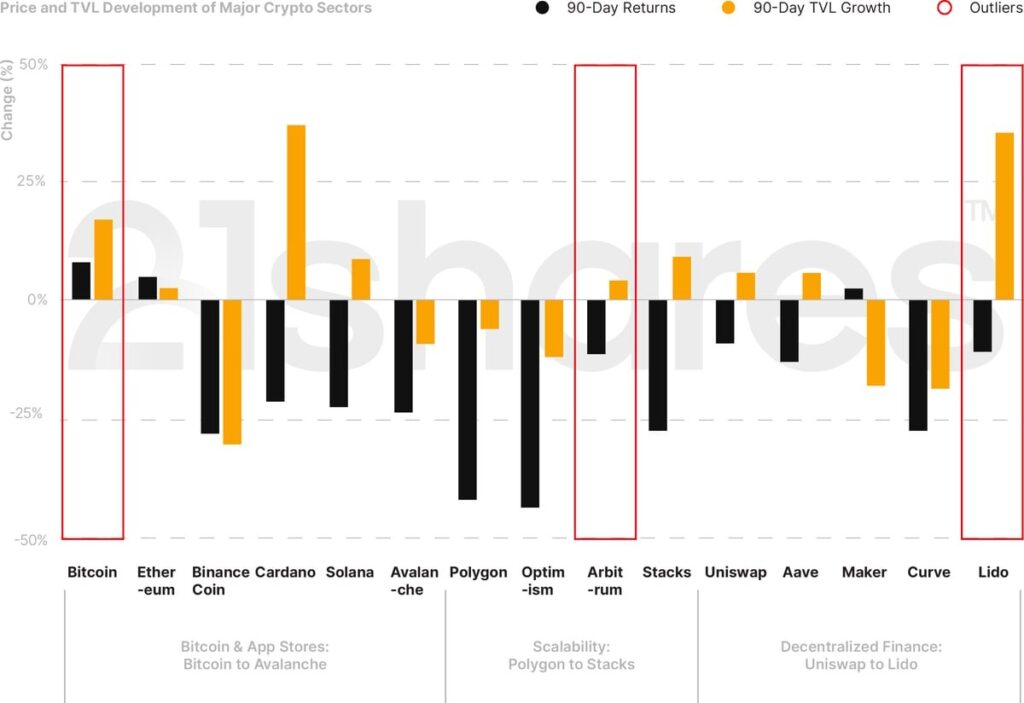

Growing institutional adoption, on the back of new Bitcoin ETF applications in the U.S., has reignited the crypto flame, pushing Bitcoin to its highest level since 2022: $31.2K. Over the past quarter, Bitcoin and Ethereum increased by around 8% and 5%, respectively. Scalability solutions suffered the most. Falling by 7%, Arbitrum came out with the least losses in Q2 in comparison with its peers, as shown in Figure 1. In the realm of DeFi, Lido was the frontrunner, soaring by 35% in TVL. This jump could be attributed to Lido’s success in executing its staked ETH withdrawals.

Figure 1: 90-Day Price and TVL Developments of Cryptoassets in Major Sectors

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of June 26, 2023.

5 Trends to Remember from Q2

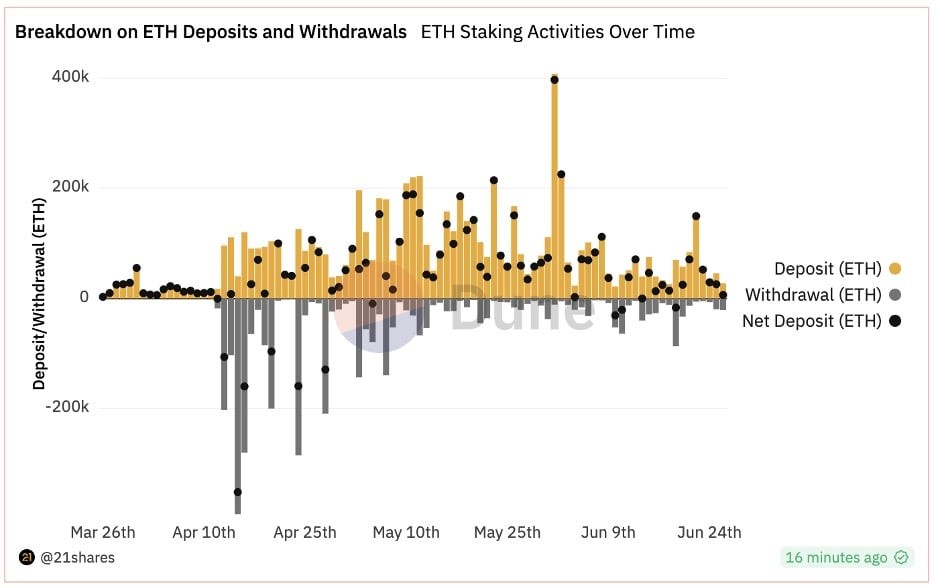

• After a long wait, investors can finally withdraw their staked Ether: Since the Ethereum staking contract launched in December 2020, investors who wanted to validate transactions and secure the network had to withstand an indefinite lockup period on their Ether (ETH). On April 12, the Shanghai upgrade was activated, closing the loop on staking liquidity by allowing investors to finally withdraw their locked ETH. Despite ~73k validators exiting the network as of June 26, Ethereum staking has seen almost 4 million ETH in net new deposits since April 12. This shows that enabling withdrawals has reduced the liquidity risk for investors, particularly institutions.

Figure 2: Breakdown of ETH deposits and Withdrawals

Source: 21shares on Dune Analytics

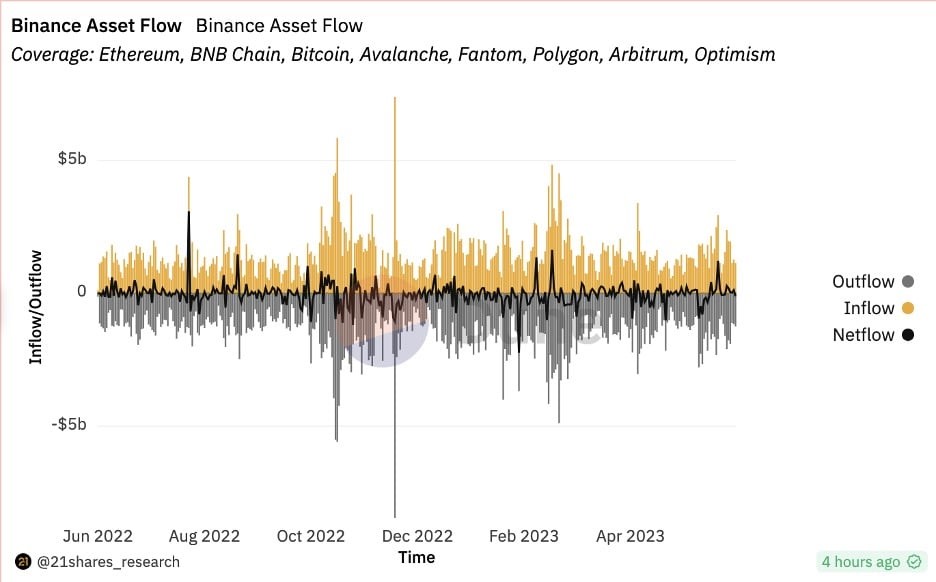

• Binance faces hurdles in the U.S. and Europe: The world’s largest crypto exchange and its founder are facing 13 charges which include operating an unregistered exchange, commingling of assets, and misrepresenting trading controls and oversight on the Binance.US platform. While the lawsuit filed by the Securities and Exchanges Commission (SEC) is still pending a verdict, Binance’s balance fell by almost 8% this quarter. Selling pressure could have also been partly influenced by some less tense trouble Binance has been facing in Europe. The exchange exited the Netherlands after failing to get regulatory approval as a virtual asset provider. France is also preliminarily investigating Binance for alleged money laundering, to which Binance’s CEO appeared relaxed, saying that they have collaborated with the French authorities and that this legal procedure is the norm in France. With the Markets in Crypto Assets (MiCA) regulatory framework going into effect by the beginning of next year, Binance has voluntarily exited other European countries, like Austria and Cyprus, to reportedly focus on complying with MiCA.

Figure 3: Asset Flow on Binance

Source: 21shares on Dune Analytics

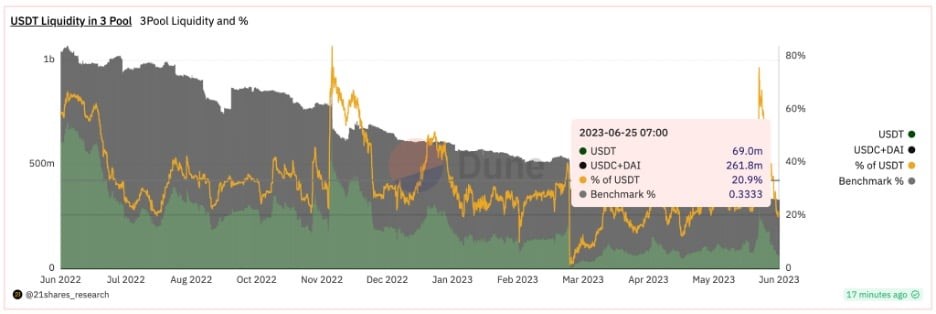

• A busy quarter for Tether: On May 17, Tether announced it would use 15% of its monthly net operating profits to buy BTC to diversify its reserve surplus. Three weeks later, Tether’s USDT circulating supply reached a new all-time high of $83.3 billion, while Circle’s USDC and Binance’s BUSD remained down ~50% and ~80% from their peak in June and November 2022, respectively. Finally, short-sellers drove USDT’s liquidity in Curve’s 3Pool to $285 million, making up over 70% of the pool at its peak and causing the stablecoin to trade 0.3% off its peg on June 15. However, USDT quickly re-pegged, and it took only seven days to get back below the pool’s 33% benchmark, suggesting that the actions were unfounded and that USDT remains the market’s preferred stablecoin.

Figure 4: USDT Liquidity in 3Pool on Curve

Source: 21Shares on Dune Analytics.

• MakerDAO strengthens its reserves, boosts its revenue: Near the end of Q2, the third largest money market application in DeFi purchased an additional $700M in Treasury bonds as part of its ongoing effort to strengthen the reserves backing its DAI stablecoin. Maker also implemented a six-month U.S. Treasury ladder strategy involving bi-weekly roll-overs to boost its revenue. This ties in with our thesis that utilizing Real World Assets (RWA) to generate revenue is a significant structural development to help create real inherent value. With the expansion of its RWA holdings, Maker could be more profitable in the quarters to come.

• Deutsche Bank applies to be a crypto custodian: On June 20, Germany’s largest bank applied for a digital asset license to operate as a custody service for cryptoassets to increase its fee income. DB’s interest in crypto custody speaks volumes of the market opportunity it wants to tap into. Not only is it a stamp of recognition of our trillion-dollar industry, but more so an indicator of the market sentiment that hadn’t died out since 2022, when the bank first hinted at its interest in crypto custody. This will make accessing and safeguarding crypto a lot easier for retail investors who are not tech savvy, not well acquainted with hardware wallets, or simply do not trust the crypto-native solutions offered at the time.

What You Should Pay Attention To

Growing institutional adoption will continue to drive the market sentiment: All eyes are on Grayscale’s lawsuit against the SEC’s rejection of its Bitcoin Trust filing. The company expects to hear a final decision from the DC District Court of Appeals in Q3 or later. On the other side of the world, HSBC Hong Kong, the largest bank in the special administrative region of China, is now allowing customers to trade Bitcoin and Ethereum ETFs listed on Hong Kong’s stock exchange. We are witnessing an unprecedented growing interest in this asset class, especially on the institutional level, which has always been considered a strong catalyst for any emerging technology looking to reach mass adoption.

The IMF finally admits the world can’t effectively ban crypto, doubles down on CBDCs: This quarter was a playground for change of hearts, namely the International Monetary Fund’s view on crypto. In its recent report on the use cases of central bank digital currencies (CBDCs) in Latin America and the Caribbeans, the IMF noted that an outright ban on cryptoassets would be ineffective in the long run. While the report is mainly advocating the advantages CBDCs have over cryptoassets, the silver lining is that cryptoassets are no longer looked at as an entirely fraudulent monetary system. In the coming quarters, we can witness leaps toward regulatory clarity across various regions.

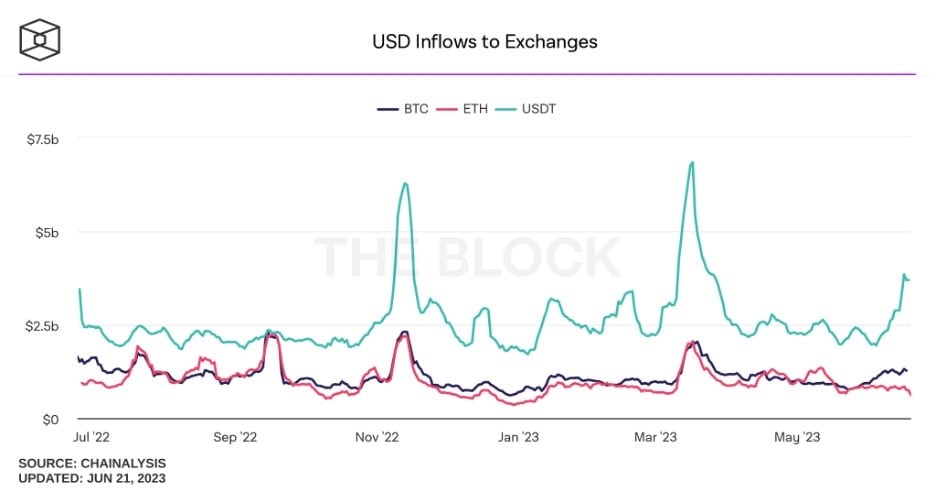

The Feds want oversight on stablecoin regulations to be discussed in late July: The House Financial Services Committee is preparing two bills aiming to give more legal clarity around cryptoassets, including stablecoins and crypto exchanges. The chair of the Federal Reserve, Jerome Powell, said that stablecoins as a form of payment need to be supervised by central banks. Chairman Patrick McHenry disagreed, saying Congress may need to examine separating supervision and regulation out of the Fed and gaining greater oversight and control. Powell also mentioned that a U.S. CBDC is a far-fetched mission, which leaves the focus on stablecoins, which has seen a noticeable rise in adoption, as shown in the figure below.

Figure 5: USDT Inflows to Exchanges

Source: Chainalysis, The Block

Liquidity is moving on-chain: The proportion of trading volume on decentralized vs. centralized exchanges reached an all-time high of 21.65% in May after steadily trending higher since the collapse of FTX in November 2022. Now, given the current regulatory climate in the U.S., with Binance and Coinbase facing pressure from the SEC, and the upcoming release of Uniswap v4, the perfect storm is forming for DEXs to continue gaining momentum over the following quarters. Uniswap v4 will introduce limit orders, time-weighted average prices (TWAPs), native support for ETH, and architectural changes like “hooks,” which would allow for potential new use cases, like MEV-capturing AMMs.

Figure 6: : DEX to CEX Spot Trade Volume

Source: Bitcoin Key Metrics, 21shares on Dune Analytics.

Next Month’s Calendar

Top 3 events we’re closely monitoring in July:

• July 5: FOMC Meeting Minutes

• July 11 onwards: Crypto bill mark-up, led by Rep. Patrick McHenry

• July 26: Federal Fund Rate

Source: Forex Factory, CoinMarketCal

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.