Nyheter

Crypto Market Compass | 15 July 2024

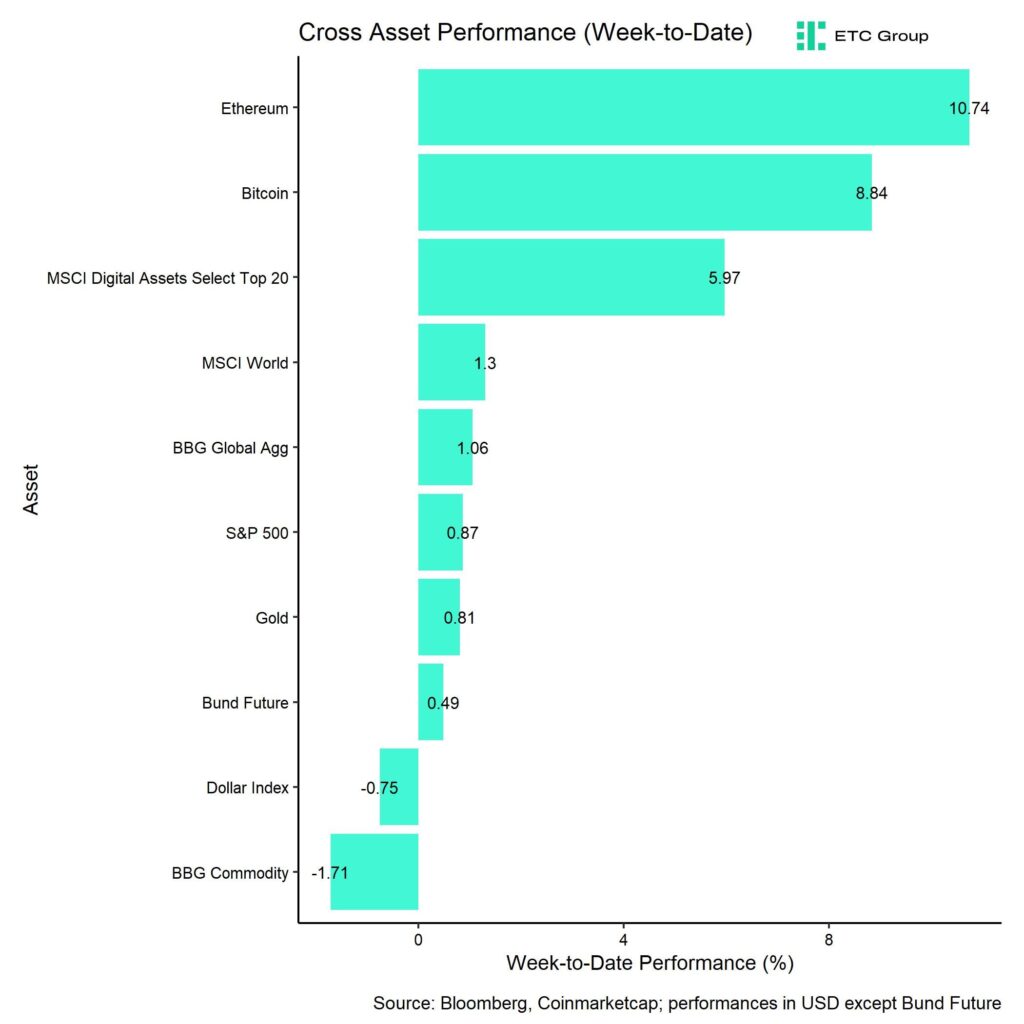

• Last week, cryptoassets outperformed significantly on account of increasing evidence of seller exhaustion and favourable tailwinds from US monetary policy and US political developments.

• Our in-house “Cryptoasset Sentiment Index” has reversed sharply and signals a slightly bullish sentiment again.

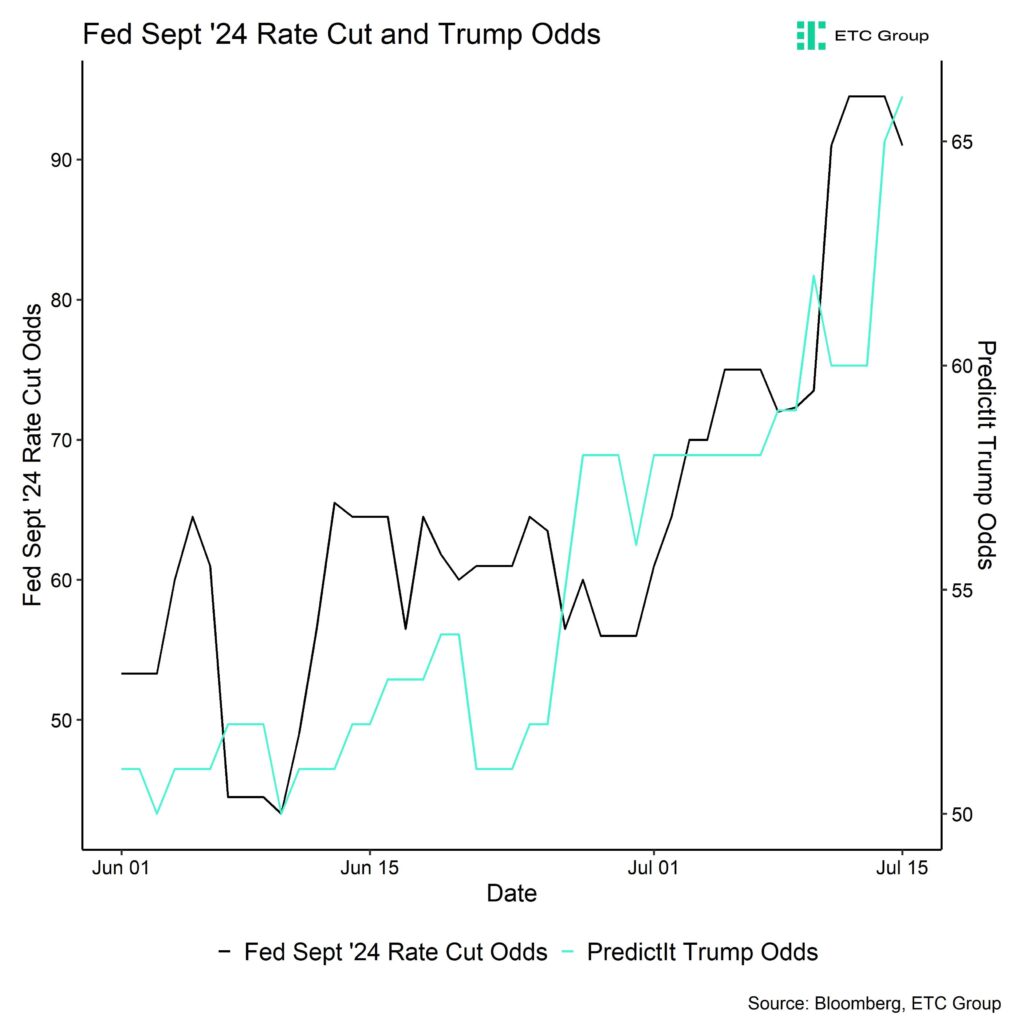

• Both increasing odds for an initial Fed rate cut in September and increasing odds of a Trump presidency have provided a significant tailwind for Bitcoin and cryptoassets more recently.

Chart of the week

Performance

Last week, cryptoassets outperformed significantly on account of increasing evidence of seller exhaustion and favourable tailwinds from US monetary policy and US political developments.

Most notably, the odds for a Fed rate cut in September have significantly increased following weaker-than-expected inflation readings in June that have paved the way for earlier rate cuts in September.

At the time of writing, Fed Funds Futures pencil in a 91% chance of a Fed rate cut in September.

In addition, Trump odds for the presidential election in 2024 have jumped to new highs following the failed assassination attempt over the weekend (Chart-of-the-Week).

Trump has reiterated his intention to speak at the Bitcoin conference in Nashville on the 27th of July despite the assassination attempt, which has buoyed market sentiment in Bitcoin.

The favourable developments were flanked by the fact that the German government entity has completed its sale of 50k BTC last week on Friday. This had been a constant source of selling pressure over the past weeks which has now subsided.

Meanwhile, we saw increasing buying interest from global crypto ETP investors as well as global hedge funds that appear to have increased their market exposure to Bitcoin as well.

Furthermore, market sentiment is currently supported by the anticipated trading launch of the US spot Ethereum ETFs which is expected to take place on the 18th of July this week, according to Bloomberg analysts.

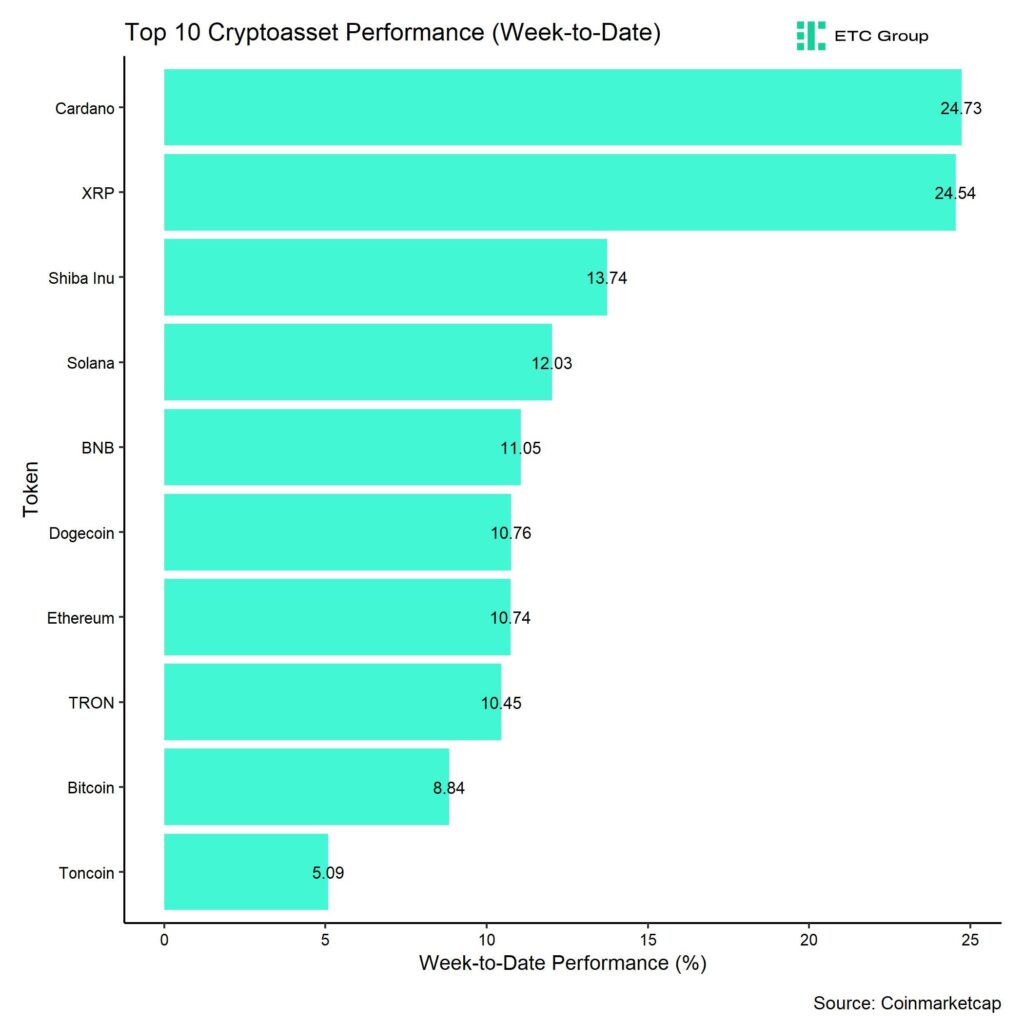

In general, among the top 10 crypto assets, Cardano, XRP, and Shiba Inu were the relative outperformers.

Overall, altcoin outperformance vis-à-vis Bitcoin has significantly increased again compared to the prior week, with 85% of our tracked altcoins managing to outperform Bitcoin on a weekly basis. Ethereum also outperformed Bitcoin on a weekly basis.

Sentiment

Our in-house “Cryptoasset Sentiment Index” has reversed sharply and signals a slightly bullish sentiment again.

At the moment, 8 out of 15 indicators are above their short-term trend.

Last week, there were significant increases in the BTC Futures Shorts Liquidation Dominance and the crypto ETP fund flows.

The Crypto Fear & Greed Index currently signals a “Neutral” level of sentiment as of this morning. It had fallen to “Extreme Fear” readings last week.

Performance dispersion among cryptoassets has increased slightly again. This means that altcoins are becoming less correlated with the performance of Bitcoin again.

Altcoin outperformance vis-à-vis Bitcoin has also significantly increased compared to the week prior, with around 85% of our tracked altcoins outperforming Bitcoin on a weekly basis, which is consistent with the fact that Ethereum also outperformed Bitcoin last week.

In general, increasing (decreasing) altcoin outperformance tends to be a sign of increasing (decreasing) risk appetite within cryptoasset markets and the latest altcoin outperformance could signal increasing appetite for risk at the moment.

Meanwhile, sentiment in traditional financial markets also continued to improve along with a significant increase in market-based monetary policy expectations, judging by our own measure of Cross Asset Risk Appetite (CARA).

Fund Flows

Fund flows into global crypto ETPs continued to be very positive and even accelerated compared to the prior week.

Global crypto ETPs saw around +1,852.5 mn USD in net inflows across all types of cryptoassets which is significantly higher than the +695.9 mn USD in net inflows recorded the prior week.

Global Bitcoin ETPs saw net inflows of +1,749.9 mn USD last week, of which +1,047.7 mn USD in net inflows were related to US spot Bitcoin ETFs alone.

Last week also saw significant inflows into Hong Kong Bitcoin ETFs once again with +451.9 mn USD in net inflows.

Outflows from the ETC Group Physical Bitcoin ETP (BTCE) decelerated last week with net outflows equivalent to -15.0 mn USD while the ETC Group Core Bitcoin ETP (BTC1) saw positive net inflows of +0.9 mn USD.

The Grayscale Bitcoin Trust (GBTC) continued to see minor net outflows, with around -35.2 mn USD last week.

Meanwhile, global Ethereum ETPs also saw an acceleration in flows last week compared to the week prior with positive net inflows totalling +83.5 mn USD. Hong Kong Ethereum ETFs also attracted some capital last week (+4.2 mn USD).

The ETC Group Physical Ethereum ETP (ZETH) saw sticky AuM last week and the ETC Group Ethereum Staking ETP (ET32) showed slight net outflows last week (-0.7 mn USD in net outflows).

Altcoin ETPs ex Ethereum continued to attract capital of around +14.4 mn USD which was slightly lower than last week.

Thematic & basket crypto ETPs also continued to see positive net inflows of +4.7 mn USD, based on our calculations. The ETC Group MSCI Digital Assets Select 20 ETP (DA20) also an increase in net inflows last week (+0.5 mn USD).

Meanwhile, global crypto hedge funds have continued to increase their market exposure even further. The 20-days rolling beta of global crypto hedge funds’ performance increased to around 0.72 (up from 0.66) per yesterday’s close.

On-Chain Data

Bitcoin on-chain data paint a picture of increasing seller exhaustion and accelerating buying interest.

Most notably, the German government entity has finished its sales of its 50k BTC last week on Friday, when its combined holdings reached 0 BTC according to data provided by Arkham. These sales had been a constant source of selling pressure previously which has now subsided.

Other major holders such as the US government or the Mt Gox trustee have not sold any bitcoins over the past week. That being said, any potential distribution from these entities still remains a risk for the market.

Both entities still control around 207k BTC and 139k BTC, respectively.

In our last report we wrote:

“On a positive note, this high degree of selling implies that sellers could become exhausted relatively soon, which would lead to a stabilization in prices.”

In fact, over the past week, we saw that net buying volumes on Bitcoin spot exchanges continue to gradually increase from oversold levels as selling pressure subsided and buying interest gradually accelerated as well. More specifically, net buying volumes on Bitcoin spot exchanges has increased to +353 mn USD over the past 7 days which is the highest level in 2 months.

Whale exchange transfers had reached the highest level since May 2023 last week in an increasing sign of whale capitulation and overall seller exhaustion. Whales are defined as entities that control at least 1,000 BTC.

In fact, whales realized the highest number of losses in USD-terms last week on Friday since July 2023. Whales are mostly comprised of short-term holders with a holding period of less than 155 days.

We think that this developments is particularly bullish and also adds to the evidence that a tactical bottom is likely as stated here.

Meanwhile, the Bitcoin mining hash rate has continued to stabilize since its low reached on the 28th of June and has increased by almost 50 EH/s since then. This is a sign of decreasing economic pressure on Bitcoin miners and decreases the risk of significant distributions.

In fact, the percentage of mined supply sold has decreased to the lowest level in 2024 to 95% over the past 30 days. This means that bitcoin miners have started to hold more than they mine on a daily basis. This has also decreased selling pressure on the market.

Futures, Options & Perpetuals

Last week, both BTC futures and perpetual open interest increased significantly in a sign of a return in risk appetite. More specifically, BTC futures and perpetual open interest increased by approximately +22k BTC and +17k BTC, respectively. This happened amid a spike in short futures liquidations to the highest level since mid-April 2024.

Perpetual funding rates remained positive throughout last week. When the funding rate is positive (negative), long (short) positions periodically pay short (long) positions. A positive funding rate tends to be a sign of bullish sentiment in perpetual futures markets.

The 3-months annualized BTC futures basis rate increased sharply from its recent lows to around 11.9% p.a.

BTC options’ open interest increased only slightly last week. Mostly driven by an increase in BTC call option demand as evidenced by the sharp drop in put-call open interest ratio.

This is consistent with the fact that the 1-month 25-delta option skew also declined significantly signalling a drop in relative demand for put options.

BTC option implied volatilities have generally declined over the past week. Implied volatilities of 1-month ATM Bitcoin options are currently at around 47.9% p.a.

Nonetheless, the term structure of volatility is still slightly inverted now, with short-dated options trading at significantly higher implied volatilities than options expiring in October. This could have something to do with the anticipated trading launch of Ethereum spot ETFs this week. The term structure of implied volatilities for Ethereum options shows a similar pattern, although less pronounced.

Bottom Line

• Last week, cryptoassets outperformed significantly on account of increasing evidence of seller exhaustion and favourable tailwinds from US monetary policy and US political developments.

• Our in-house “Cryptoasset Sentiment Index” has reversed sharply and signals a slightly bullish sentiment again.

• Both increasing odds for an initial Fed rate cut in September and increasing odds of a Trump presidency have provided a significant tailwind for Bitcoin and cryptoassets more recently.

To read our Crypto Market Compass in full, please click the button below:

This is not investment advice. Capital at risk. Read the full disclaimer

© ETC Group 2019-2024 | All rights reserved