Nyheter

Can mining strikes offset currency headwinds?

Platinum and the Rand: Can mining strikes offset currency headwinds? Platinum prices have rebounded by over 20% during 2016, as the South African Rand (ZAR) has strengthened 4%. A stronger ZAR should constrain supply by narrowing already stretched mining company margins. Opposing forces are likely to keep price volatility elevated in coming months as a potentially weaker ZAR balances the threat of output cuts from strike action.

Economic conditions are challenging to say the least. South African growth is expected to be just 0.6% in 2016 according to the IMF, from 1.3% in 2015, the lowest in over six years. Rising social tensions are a result of burgeoning unemployment. Unemployment is at the highest level since records began in 2008, at nearly 27% of the population, according to Stats SA.

Drought is impacting food prices, driving inflation higher, and at the same time the central bank is raising rates to try and keep prices in check. Raising rates to offset supply side inflation and reduce capital outflows is a sign of desperation and the local currency is unlikely to be a beneficiary of such action. Indeed, the South African Reserve Bank notes that the weaker currency could be fuelling inflationary pressures.

As a general rule of thumb, investors should be wary of those EM countries that are tightening monetary policy to stave off capital flight, especially when there is little inflationary pressure and weak growth – South Africa is a good example. With lacklustre outlook for the economy, the Rand is likely to remain weak.

Early June sees the potential for a credit rating downgrade for South Africa from S&P Global Ratings, with consensus economist expectations that the country’s rating will enter junk territory by end-2016. The IMF’s most recent mission to the country suggests that the government’s budget target ‘may be challenging’. A decrease to non-investment grade is likely to prompt further capital outflows and see the ZAR move lower against the USD.

The close correlation between the currency and platinum should see metal prices follow ZAR lower in the near term. However, later in June, and with another supply deficit forecast in 2016, the platinum price is likely to receive support from potential output reductions resulting from contract negotiation activity and possible strike action[i].

(click to enlarge)

[i] Recent strike action in South Africa in 2012 and 2014 lifted the platinum price by 17% and 0.5%, respectively.

Martin Arnold, Global FX & Commodity Strategist at ETF Securities

Martin Arnold joined ETF Securities as a research analyst in 2009 and was promoted to Global FX & Commodity Strategist in 2014. Martin has a wealth of experience in strategy and economics with his most recent role formulating an FX strategy at an independent research consultancy. Martin has a strong background in macroeconomics and financial analysis – gained both at the Reserve Bank of Australia and in the private commercial banking sector – and experience covering a range of asset classes including equities and bonds. Martin holds a Bachelor of Economics from the University of New South Wales (Australia), a Master of Commerce from the University of Wollongong (Australia) and attained a Graduate Diploma of Applied Finance and Investment from the Securities Institute of Australia.

We’re seeing increasing client interest in how crypto behaves during market stress. This week’s Hash Insider, our weekly research letter, dives into correlation dynamics.

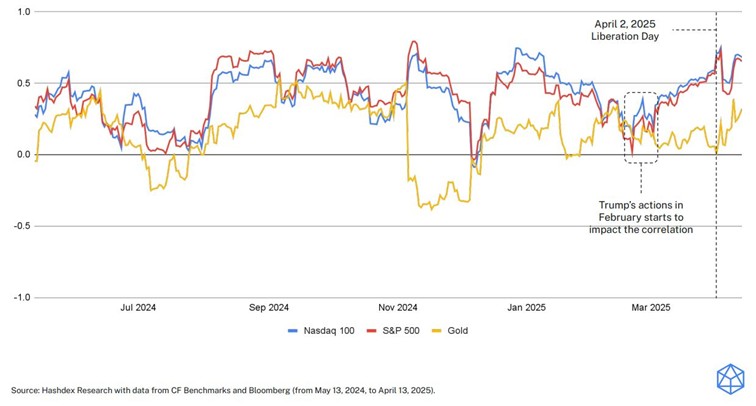

Crypto Correlations Shift Pattern

Toward the end of February, correlations between crypto and other asset classes—excluding gold—began to rise, influenced by key US policy decisions on international trade tariffs. This trend, captured in the 30-day correlation window, is typical during periods of market stress, when assets often move in tandem, reflecting a broader risk-off sentiment.

However, in the wake of “Liberation Day,” this pattern unexpectedly broke, with crypto correlations declining (except to gold). This anomaly mirrors the first week of April when digital assets outperformed traditional markets despite economic uncertainty.

Nasdaq Crypto Index correlation with traditional asset classes:

More in this week’s Hash Insider → Link to report

In addition, our team looked at market rebound past dynamics:

Bitcoin: Post-Stress Winner

Looking back at six major dislocations since 2020, Bitcoin saw sharp drawdowns in the first 10 days—but outperformed all major assets 60 days later in four of the six cases. In my view, the current environment could offer interesting entry point to build a position into the broad crypto market via the Nasdaq Crypto Index. More details about our flagship ETP replicating this index on its Product Page .

How assets performed after stress events

Source : Hashdex and Bloomberg

{kind=link}

Crypto’s stress-tested resilience

BlackRock tar iShares S&P 500 3% Capped UCITS ETF till Europa

CNFY ETF de 50 största och mest likvida kinesiska aktierna på ChiNext

Bitcoin supply on crypto exchanges hits 5-year low and that’s a good sign

WDSD ETF småbolag från hela världen

Fonder som ger exponering mot försvarsindustrin

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Warren Buffetts råd om vad man ska göra när börsen kraschar

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Svenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFonder som ger exponering mot försvarsindustrin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanWarren Buffetts råd om vad man ska göra när börsen kraschar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf lanserar Europa-fokuserad försvars-ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV mars 2025