Nyheter

Bitcoin Nears All-Time High, 26% of ETH Staked, and Uniswap Considers Staking: What Happened in Crypto This Month?

February started with short-lived outages and ended with a bull run. As a cherry on top, Gemini Earn customers were promised to be made whole, in kind, after a billion-dollar settlement! Bitcoin’s price has increased by over 250% since the termination of Gemini Earn in January 2023. While profit-taking measures may follow Gemini’s pending payback, the accumulation levels of Bitcoin short-term holders and the record-breaking flows in U.S. spot Bitcoin ETFs, as mentioned in this report, may balance out the potential sell-off. In this monthly review, we’ll discuss the following trends driving the market:

• Bitcoin Nears All-time Highs During Slowing Economy

• More ETH Staked and the Growing Narrative of Liquid Re-staking

• Staking Rewards Revisited, Uniswap Breaks Out of Its 2-Year Lows

Bitcoin Nears All-time Highs During Slowing Economy

The Federal Reserve’s favorite gauge for inflation, the Personal Consumption Expenditure (PCE) index, rose by 2.8% from a year ago, the highest increase in the last 12 months but in line with expectations. After three straight months of increases, there was a 6.1% decline in manufacturing purchase orders of durable goods, less than the forecasted -4.9% and the lowest in almost four years. Although the economy is slowing down, the pace is fast enough to dodge a recession despite rising unemployment claims exceeding expectations. While one print alone is not indicative of how the Fed will respond, it still sets the tone for potential future interest rate cuts. Lower rates usually benefit risk-on assets like tech and crypto.

Bitcoin, in the meantime, has already reached all-time highs, as flows in Bitcoin spot ETFs break the record of $673M in daily net inflows. Speculation as we near the Halving, expedited by the spot Bitcoin ETFs in the U.S., has driven BTC to grow by ~45% this month, the biggest BTC/USD candle we’ve seen before a Halving event. A case in point showing this momentum is that in less than two months, Blackrock’s ETF has accrued the same amount of flows gold’s first ETF was able to accrue in two years: $10B.

As we close the second month since the launch of spot Bitcoin ETFs in the U.S., more institutions are warming up to Bitcoin. Wells Fargo and Merrill Lynch have started providing access to spot Bitcoin ETFs to select wealth management clients. Also, Morgan Stanley is allegedly evaluating the Bitcoin funds for its brokerage platform. Estimated to hold more than $100T in assets under management, the registered investment advisory (RIA) industry and its cautious entry are anticipated to unlock even bigger capital potential for this asset class.

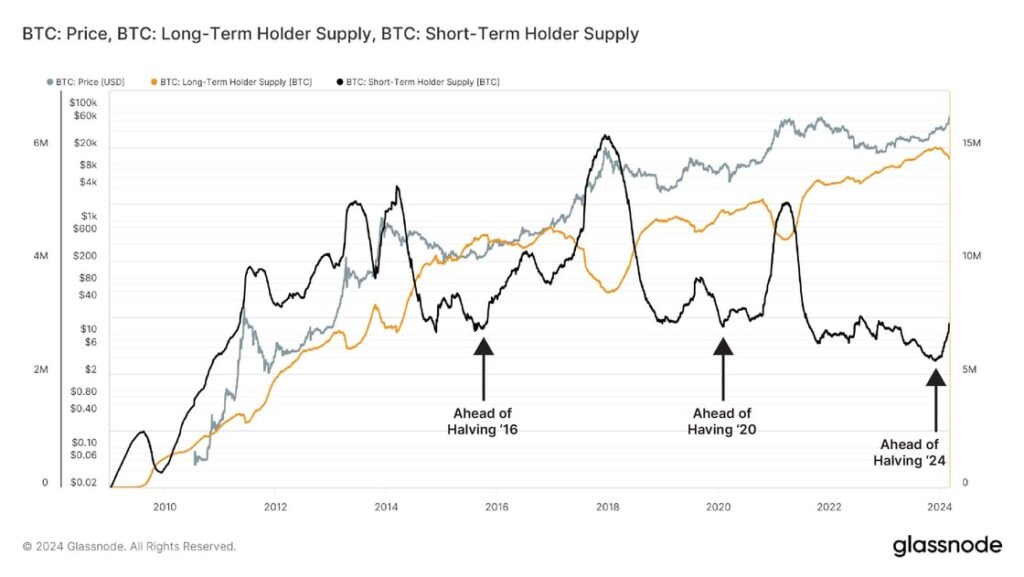

As shown in Figure 1, Bitcoin short-term holders (holding BTC for less than 155 days) have continued accumulating as is customary a few months before the asset’s halving event — the approval of the spot Bitcoin ETFs in the U.S. catalyzed buying interest. Since January 11, short-term holders have increased their BTC supply by 25%. In contrast, long-term holders reduced their holdings by 3%, which is also a trend we’ve seen in the past halving events, as depicted in the chart below. On the other hand, Bitcoin’s Futures Open Interest has spiked significantly to levels not seen since the last bull run in 2021, which investors should be aware of, as it could imply higher volatility going forward.

Figure 1 – ETF launch in the U.S. catalyzes interest for short-term holders

Source: Glassnode, 21Shares

Nevertheless, innovation on the network is still churning. Soon, Bitcoin holders will be able to earn yield by staking their idle coins (SigNet BTC) to increase the security of proof-of-stake chains in a trustless manner. This will be possible through Babylon, a new external POS protocol pioneering the new primitive for Bitcoin, which has been on the testnet since February 28.

More ETH Staked and the Growing Narrative of Liquid Re-staking

ETH jumped by ~50% this month, steadily above the $3K mark since February 25. This jump can be explained by many factors, led by the speculation around a spot ETH ETF in the U.S., as well as a new experimental token standard dubbed ERC404, still not endorsed by the Ethereum Foundation. The experimental standard integrates attributes from ERC-20 (fungible), like transferability and divisibility for its fractionalized tokens, and ERC-721 (non-fungible) standard for its unique identifier feature to track the underlying NFT. ERC404 has the potential for native fractionalizing of digital assets like collectibles and tokenized real-world assets such as funds and real estate without needing third-party solutions.

Other factors may include Bitcoin’s recent rally since ETH has been positively correlated with BTC since 2018. From a user’s perspective, Ethereum’s growing staking ratio highlights its improving fundamentals as it demonstrates more people are willing to secure the network. A little over 26% of all Ethereum has been staked by 179K unique depositing addresses. That puts the total amount of staked ETH at 31M (+$100B), with Lido dominating more than 30% of the staking market, helping to secure the network further and earning around 4-6% yield while freeing up capital that can be used across DeFi. Finally, the hype has fueled the narrative surrounding re-staking, a method enabling users to re-stake their staked ETH or liquid staking tokens (LSTs) – representing staked ETH – for additional yield (approximately 2-4% on average, added to Ethereum’s staking yield).

What is re-staking?

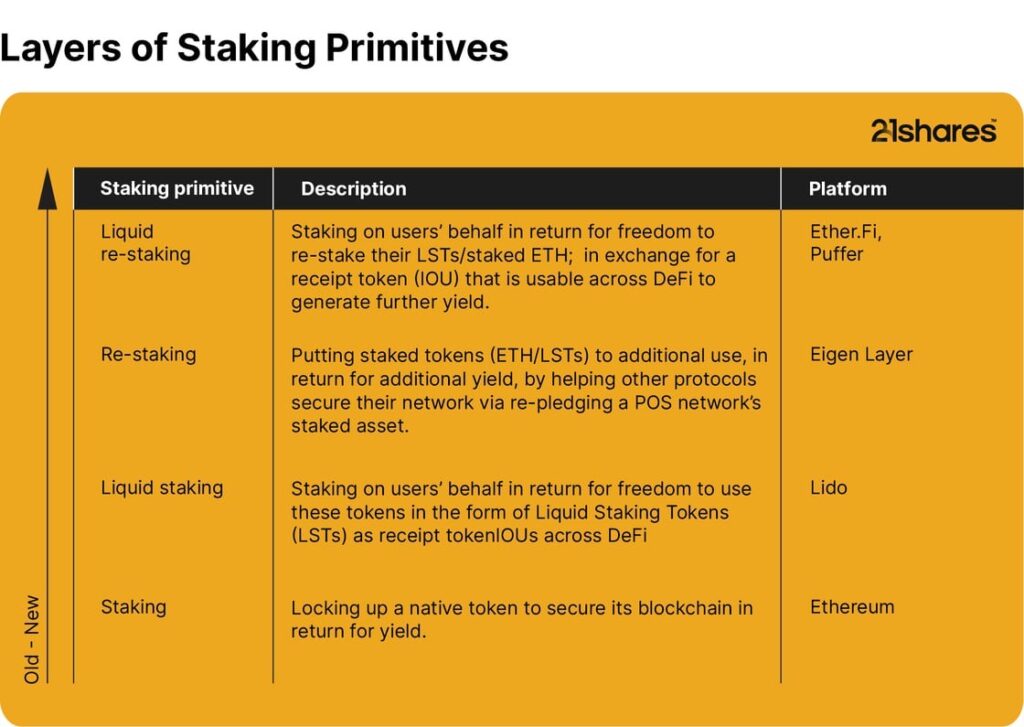

Introduced in June by EigenLayer, re-staking offers an innovative way to validate the security of external protocols by harnessing Ethereum’s proof-of-stake network. Within EigenLayer, ETH deposits can be “re-staked” across various protocols, eliminating the need to establish their own validator lists and significantly reducing the cost and time required to launch new networks. That said, liquid re-staking has emerged as a pivotal addition to the staking ecosystem, capitalizing on the growing enthusiasm for re-staking, which has put EigenLayer as the second largest protocol with $10.5B in assets under management, trailing only Lido’s liquid-staking solution with $35.2B, on Ethereum. For further clarity, please refer to Figure 2 to demystify the increasingly complex staking ecosystem.

Figure 2 – Layers of Staking Primitives

Source: 21Shares

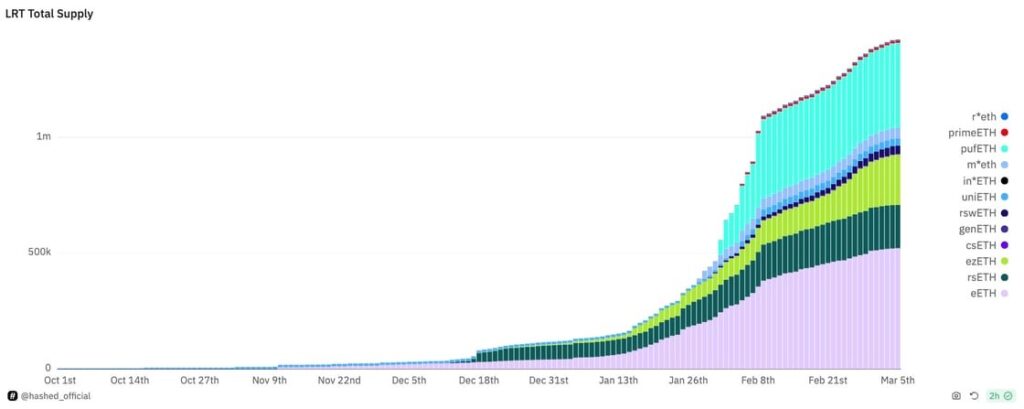

Like liquid staking, liquid re-staking simplifies the process of restaking, enabling users to maintain their capital while contributing to the security validation of the external networks integrated with EigenLayer. However, this new primitive is not without its critics, as it introduces additional slashing risks to ETH validators, who are now subject to the slashing rules of multiple networks. Moreover, Liquid Restaking Tokens (LRTs) have drawn comparisons to Collateralized Debt Obligations (CDOs) from 2008, where investment products were layered with levels of complexity that ordinary users struggled to comprehend. Of course, blockchain’s transparency sets it apart from the traditional financial system structure. Nevertheless, re-staking has been one of the fastest growing industries in 2024, as it increased by tenfold, from less than $500M at the beginning of January to more than $5B, as it continues to push the boundaries of Ethereum’s staking capabilities, as it can be observed in Figure 3 below.

Figure 3 – Growth of Liquid Restaking Tokens built on top of EigenLayer

Source: Hashed on Dune

Meanwhile, throughout February, the Dencun upgrade was successfully tested and is now scheduled for March 13. The biggest beneficiary of this upgrade will be Ethereum’s scaling solutions, such as Polygon, Optimism, and Arbitrum, whose gas fees are anticipated to decrease by around 90% once the upgrade is deployed.

Staking Rewards Revisited, Uniswap Breaks Out of Its 2-Year Lows

Uniswap is the largest decentralized exchange (DEX) by assets under management, with $5.7B in total assets locked. Before October 2023, Uniswap Labs received no fees and, therefore, no revenue; 11 investors, including Polychain and Paradigm, had solely funded the DEX. As of October 17, traders on Uniswap started paying 0.15% on their swaps only if they swapped directly on the DEX’s interface or wallet. This move added the first layer of revenue stream to fund the sustainable development of the DEX without relying on VC; Uniswap has collected $5.8M in fees since. However, the fee accrual did not benefit holders of the DEX’s native token, UNI, which remained an unproductive governance token below the $10 mark for two uninterrupted years following its all-time high of ~$45 in May 2021.

Not for long. Community members had proposed staking rewards earlier in May 2023. Almost a year later, on February 23, the Uniswap Foundation itself proposed enriching the fee mechanism to reward UNI holders who have staked and delegated their tokens. The upgrade is estimated to collectively bring between $62M and $156M to UNI holders in annual dividends. Based on that potential, UNI went on a 92% rally in February (jumping by 53% overnight after the proposal) to pass the $11 mark and increase its market capitalization by 87%. Depending on the fate of this proposal, which will be voted on starting March 8, we could see more applications follow suit as more value creation can be realized on the application layer, evident by protocols like Frax who’s already expected to unveil a revenue sharing mechanism at the end of this week. That said, caution should be exercised as enabling revenue sharing has historically been feared of triggering regulatory scrutiny; it could classify certain assets as a security due to potentially meeting the prongs of the Howey test.

Next Month’s Calendar

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

6PSE ETF ger exponering mot amerikanska aktier

iShares noterar fond för flyg- och försvarssektorn på Xetra

8RMY ETF köper bara aktier i europeiska försvarsföretag

Are Gold Mining Equities Regaining Attention Amid Rising Gold Prices?

Fem spanska fonder som har ökat med +12% under 2025

Crypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

Montrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

Svenskarna har en ny favorit-ETF

MONTLEV, Sveriges första globala ETF med hävstång

Sju börshandlade fonder som investerar i försvarssektorn

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCrypto Market Risks & Opportunities: Insights on Bybit Hack, Bitcoin, and Institutional Adoption

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMontrose storsatsning på ETFer fortsätter – lanserar Sveriges första globala ETF med hävstång

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSvenskarna har en ny favorit-ETF

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMONTLEV, Sveriges första globala ETF med hävstång

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEuropeisk försvarsutgiftsboom: Viktiga investeringsmöjligheter mitt i globala förändringar

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa