Nyheter

Are Cross-Chain Solutions the Key to Crypto’s Future Success?

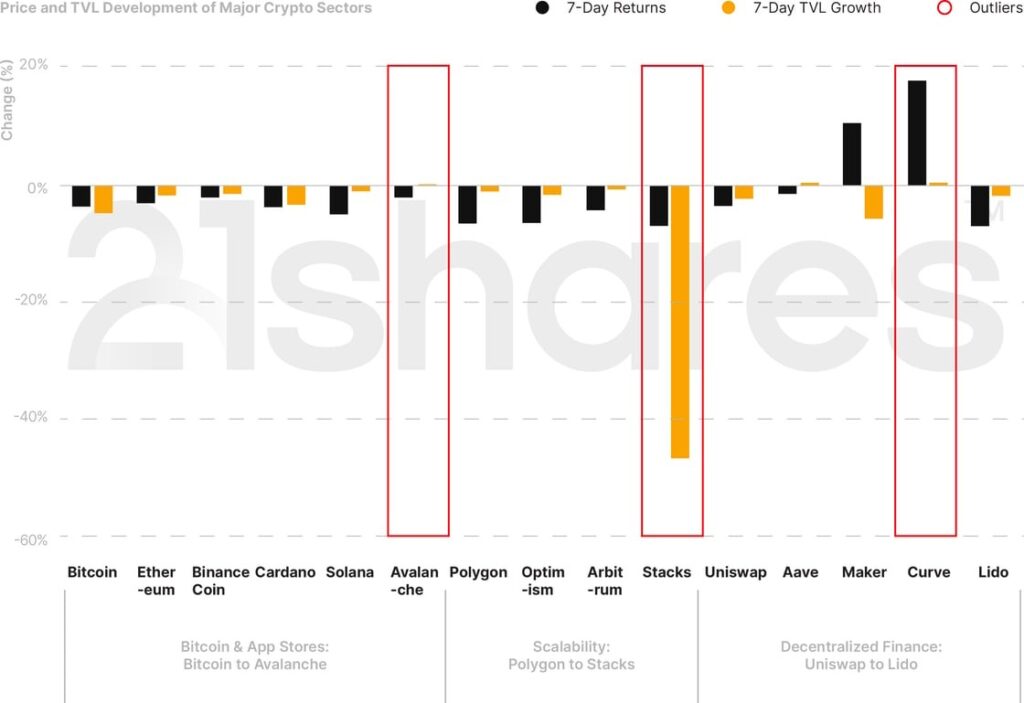

With interest rates unchanged this month, and in anticipation of the final one before the year ends, markets reacted mildly negatively to the Federal Reserve’s higher-for-longer sentiment, echoed by Jerome Powell. Bitcoin and Ethereum are still moving sideways, dipping by 3.73% and 3.12% over the past week, respectively. Avalanche was the only Layer 1 to accrue millions of dollars (~$4M) over the past week, slightly jumping by 0.27% in assets. Scalability solutions have struggled over the past week, especially with Stacks, sinking by 46.7%. In DeFi, Curve was the biggest winner (17.62%).

Figure 1: Weekly Price and TVL Developments of Cryptoassets in Major Sectors

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of September 26, 2023.

5 Things to Remember in Markets this Week

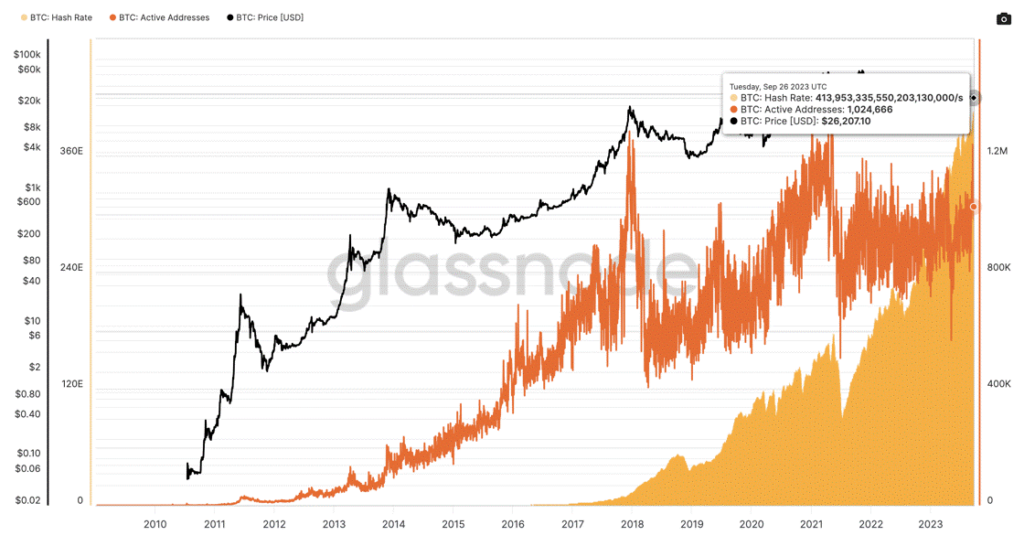

• Bitcoin Is More Robust Than Ever

A rising hash rate indicates strengthened security for the Bitcoin network. Bitcoin miners seem to be mining at a discounted threshold, as the estimated production cost per block is at $24.3K, according to data collected from Glassnode, almost $2K below the current price of BTC. Active addresses also increased to an average of 1,064,854 per day over the past week, a nearly 40% increase year-over-year.

Figure 2: Bitcoin Hashrate

Source: Glassnode

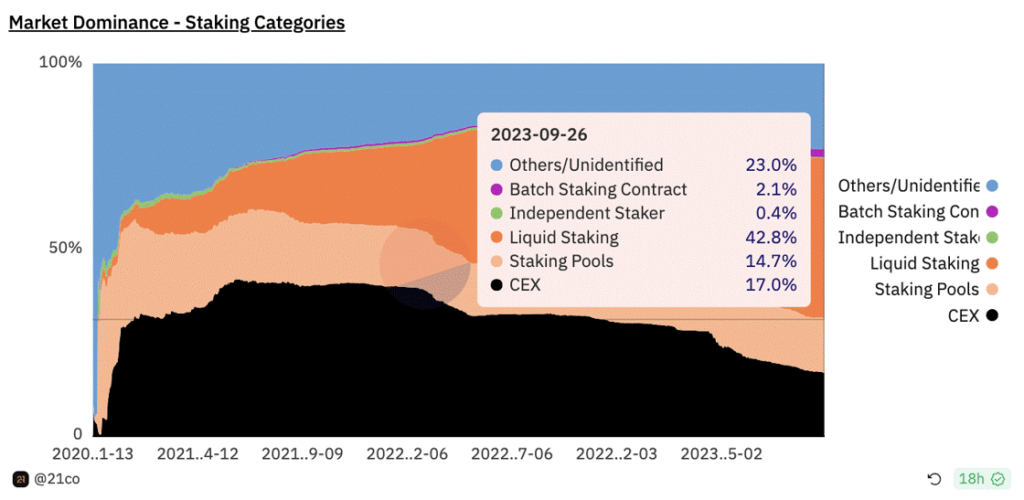

• Ethereum’s staking to undergo further decentralization

SSV, a technology company, launched a novel software to combat centralization from staking on Ethereum. The protocol leverages Distributed Validator Technology (DVT). This technology distributes key management and signing duties to multiple parties to eliminate a single point of failure, enhancing Ethereum’s security and decentralization. The approach allows multiple node operators to run a single validator, reducing risks of compromise and slashing penalties associated with a single validator, as operators can go offline without affecting the underlying software. Finally, this solution is vital for centralized platforms like crypto exchanges and non-custodial providers like Lido, potentially expanding its validator list beyond 31, although their V2 roadmap will enable validators to join without relying on SSV. Despite its promise, caution remains regarding unforeseen risks in this novel implementation.

Figure 3: The Concentration of Staking amongst the Different Key Categories

Source: 21co On Dune Analytics

Finally, despite Ethereum’s positive progress, challenges loom ahead as the Dencun upgrade could likely be delayed until Q1 2024. The decision is contingent on developers deploying a testnet version of the network’s next major upgrade before November’s DevCon, which would give them ample time to validate the new features and enable a robust implementation.

• Interconnected Execution Environment Spanning Across 3 Networks

Injective protocol, the Cosmos-based application chain, announced a new tool linking Ethereum to the Cosmos and Solana networks. Dubbed “inEVM,” the custom scaling solution will come in the form of an L2 that allows ETH developers to expand their toolings towards the alternative ecosystems without necessitating structural code change, analogous to Windows applications working on top of MacOS. The integration, expected to go live at the end of Q4, also promises expedited transaction processing, instantaneous finality, enhanced composability, and shared liquidity. Although inEVM showcases a potential solution to the fragile cross-chain bridging infrastructure, its acceptance remains to be seen, particularly in light of earlier launches like “NeonEVM” and “Cascade”. Both initiatives facilitated multi-layered execution environments spanning between Ethereum and Near, and later Solana and Cosmos, yet lacked significant traction so far. Finally, worth noting that despite “NeonEVM” raising $40M in late 2021, the protocol just went live in early August of 2023. Thus, it’s challenging to use it as a benchmark to predict the level of adoption across the comparable “inEVM”.

• New Era for Scaling Ethereum

Eclipse, the customizable rollup provider, has unveiled its innovative modular scaling solution. Unlike monolithic blockchains, where a single network handles execution, settlement, consensus, and data availability, Eclipse employs a modular approach, separating these functions across different blockchains. In the context of Eclipse, the L2 architecture will use Ethereum for settlement while leveraging Solana for execution on the back of its parallel processing capabilities for high performance. Further, Eclipse will utilize Celestia to store transaction data on its blockchain and offload Ethereum’s costly storage costs while employing RISC to prove the validity of transactions settled on Ethereum via ZK proofs. This announcement signifies a significant shift in scaling approaches, aligning with our belief in a multi-chain future where diverse smart-contract platforms collaborate for a scalable blockchain landscape, challenging the winner-takes-all scenario.

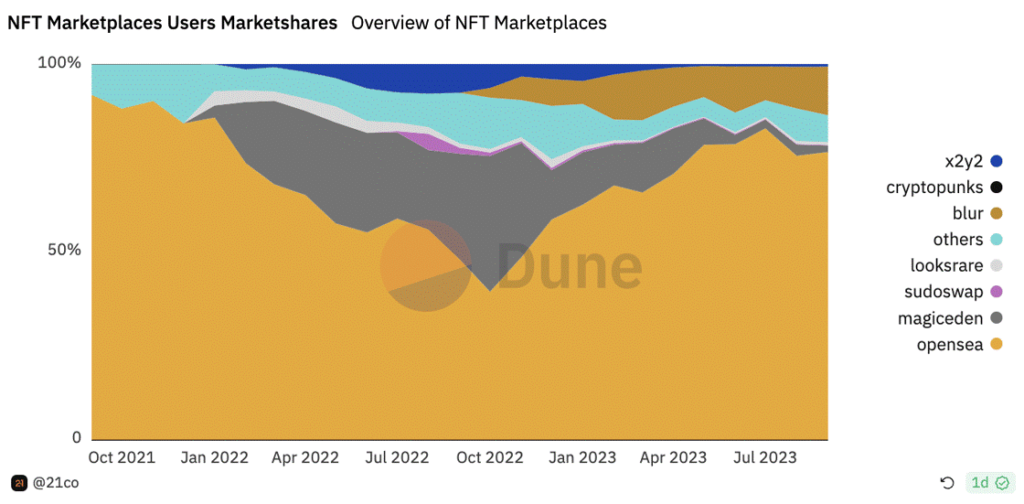

• Momentum on Polygon and Solana Outpace Ethereum in NFTs

Polygon and Solana’s NFT sales volume increased by 20% and 33%, respectively, over the past week. In comparison, Ethereum’s total NFT sales declined by almost 17% over the same period. However, Ethereum’s sales are still almost double those of Polygon and Solana-based NFTs combined. Back in July, Solana introduced compressed NFTs: a cost-effective way for creators to produce digital collectibles, by drastically reducing the storage cost for NFTs, storing their metadata within the ledger rather than in a typical Solana account. On September 15, Magic Eden adopted the solution, allowing its 9.32K daily unique active users on its marketplace to mint a million compressed NFTs for $113 as opposed to $33M on Ethereum, according to Solana. The competition is on since the market leader, OpenSea, announced on September 19 that they’re rolling out the “Creator Studio” to allow artists to launch, drop, and mint NFTs without using any code. The new feature also comes with a better intro page of creators, allowing a better user experience for existing artists to expand their work using NFTs and gain better exposure.

NFT marketplaces, across chains, are still grappling with the formula required to attract more loyal users. The question is: Will the cost-efficiency of Solana’s compressed NFTs cost OpenSea its creators, or will the no-code Creator Studio make the game even?

Figure 4: Overview of NFT Marketplaces by Userbase

Source: 21co on Dune Analytics

What You Should Pay Attention To

Crypto Deepening Integration with TradFi

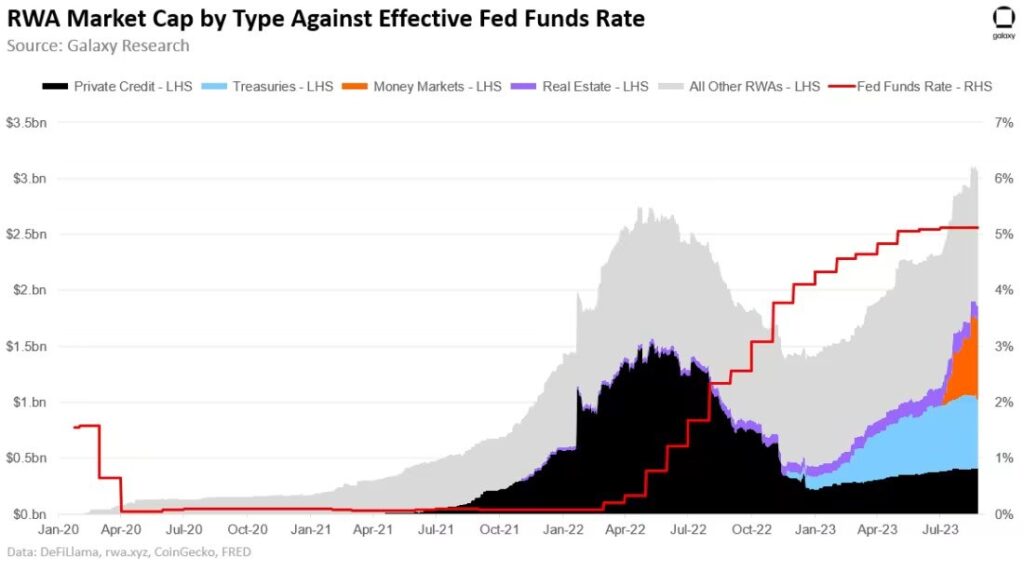

In the face of persistent inflation and anticipated prolonged high interest rates, several DeFi blue-chip entities are establishing synergies with TradFi to stimulate growth. Maker, as an early adopter, strategically leveraged the prevailing high interest rate environment in the US, being the first protocol to invest in US treasury bonds since October 2022. This strategic initiative has resulted in an accrued annualized revenue of approximately $190M for Maker DAO.

That said, Frax and Aave are now following Maker’s suit by integrating real-world assets (RWA) into their treasuries to boost growth and hedge against crypto’s volatility. Frax partnered with FinresPBC for RWA management, to invest in US treasury bonds and distribute yields back to FRAX holders via Frax bonds, while Aave collaborated with Centrifuge to establish a legal framework for supporting RWAs to diversify collateral supporting their GHO stablecoin. We foresee this trend gaining traction in the near term, representing an effective strategy to stimulate growth and diversify against crypto-related risks.

Figure 5: Growth of Real World Assets plotted against FED Funds Rate

Source: Galaxy Research

On a larger scale, the discernible surge in tokenizing traditional financial assets is underscored by the FED’s report, highlighting initiatives fostering access to historically illiquid markets, unlike US bonds. Finally, as tokenization demonstrates its potential as a groundbreaking use case for crypto, leveraging instant settlement and cost-effectiveness, it’s important to closely observe the protocols embracing this innovation. These protocols are likely to play a significant role in accelerating the adoption of blockchain technology.

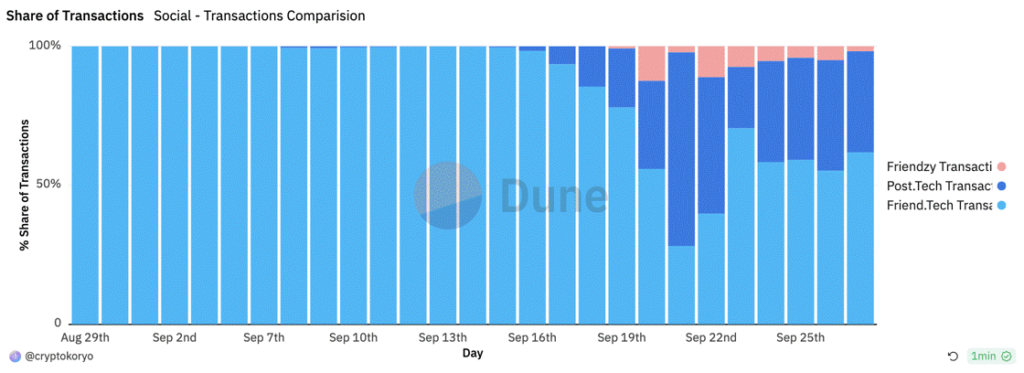

The Quest to Find A Better Social Media

In the past few weeks, we’ve seen Friend.tech launch on Base, generating nearly $29M in transaction fees from around 270K users since they started in August. As it is customary when a project creates hype, many developers raced to fork it or build on its concept. Post.tech is one of them, a new social media platform on Arbitrum, mimicking the interface of Twitter (now X). With a whitepaper still in the works, Post.tech is a SocialFi protocol represented by POST, an ERC-20 token with a total supply of 1B and whose utility revolves around rewards and governance.

With the saturation of Web 2 social media, we believe that the SocialFi movement will do to social media what DeFi is doing to traditional finance. Everyone on the internet seems to agree that user data mining is a real threat to social media users. This is where SocialFi steps in, upholding users’ ownership of their data just like the distributed ledger of blockchains protects users’ ownership of their funds, as opposed to banks. Another threat that is especially prominent on X (formerly Twitter) is spamming. SocialFi protocols have the advantage of starting a platform on a clean slate by providing adequate parameters to protect its users from unwarranted advertisements, let alone fraudulent users. Post.tech promised to tackle this problem with artificial intelligence to filter out spam messages and keep a score on users’ posts. However, SocialFi is not immune to threats, including security loopholes and social dilemmas that the community needs to solve for this space to launch successfully into the mainstream in a healthy manner.

Figure 6: Share of Transactions Between Rising SocialFi Platforms

Source: Crypto Koryo on Dune Analytics

Bookmarks

• Our Dune Dashboard tracking the holdings of cybercrime North Korean unit Lazarus Group got featured on Cointelegraph.

• This Thursday, Research Associate Tom Wan will join as a panelist in a webinar hosted by Coindesk in partnership with Flipside about Important Trends in Scaling Web3: New Data and Growth Areas.

• Check out our State of Crypto on Web 3.

• Stay tuned for our analyst call on Wednesday!

Next Week’s Calendar

These are the top events we’re monitoring for next week.

• Oversight of the Securities and Exchange Commission (SEC): The House Committee for Financial Services will examine regulatory developments, rulemakings, and activities that the SEC has undertaken since October 5, 2021.

• Fed Chair Jerome Powell will speak at the town hall with educators on September 28, which will also be a webcast live, and he will take questions from the audience.

Source: House.gov, Forex Factory

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

CEB3 ETF satsar på japanska aktier och valutasäkrar dem i Euro

UBS utökar sitt Core ETF-sortiment med räntebärande fonder

WEXF ETF investerar i hela världen utom USA

Virtune lanserar Virtune Coinbase 50 Index ETP på Nasdaq Helsinki

A slice of Bitcoin gives a big portfolio boost

De bästa ETFer som investerar i europeiska utdelningsaktier

Nordea Asset Management lanserar nya ETFer på Xetra

Svenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

De bästa ETFerna med fokus på momentum

Hetaste investeringstemat i juni 2025

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa ETFer som investerar i europeiska utdelningsaktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanNordea Asset Management lanserar nya ETFer på Xetra

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSvenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDe bästa ETFerna med fokus på momentum

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHetaste investeringstemat i juni 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan12 000 artiklar om börshandlade fonder

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanPrimer: Injective, infrastructure for global finance

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanREX Shares lanserar tre nya covered call ETFer i Europa