Nyheter

A stimulative environment for midcaps

With a soft landing in sight, Head of Global Index Portfolio Management Dina Ting, explains why resilient US economic growth alongside currently low valuations for midcaps can spur future gains in this underallocated market segment.

While the US Federal Reserve has yet to declare a victorious soft landing, the economy has improved markedly from just two years ago. Inflation has cooled substantially and the labor market has returned to a more sustainable path. “The risks to our goals are now balanced,” Federal Reserve Bank of San Francisco President Mary Daly said recently. “… data dependence does not mean being data reactive. It means looking forward as the information comes in and projecting how we think the economy will evolve.”

For Daly, this refers to optimal monetary policy. For investors, this can be taken as a cue to stay disciplined and diversified. And in a declining rate-cycle environment, this brings into focus the merits of the often-overlooked US midcap-stock segment. The underallocation is clear: Investments in large-cap mutual funds and exchange-traded funds (ETFs) are roughly nine times greater than those in mid-cap mutual funds and ETFs.

In recent months, however, we’ve seen a rotation away from the “magnificent” but overvalued technology darlings and toward what we consider more attractively valued midcaps, which feature lower risk profiles than small caps and yet have faster growth prospects than their larger peers.

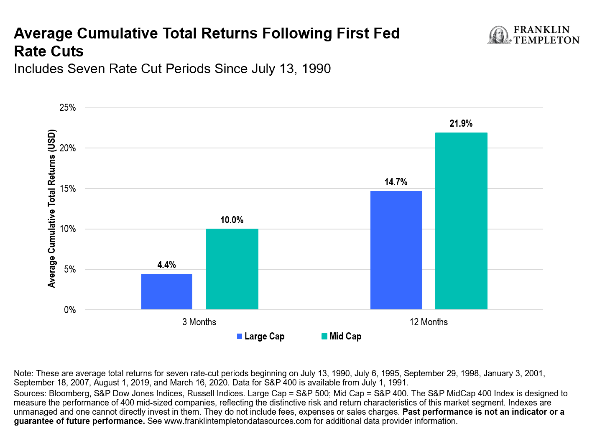

Since the end of the second quarter, US mid-cap performance (as measured by the Russell MidCap Index) has outpaced that of both large- and small-cap stocks (as measured by the Russell 1000 Index and Russell 2000 Index, respectively). Zoom out further and the asset class appears to us even more appealing for long-term investors, with mid-cap stocks (as measured by the S&P MidCap 400 Index) having outperformed their large-cap and small-cap counterparts (as measured by the S&P 500 Index and S&P Small Cap 600 Index, respectively) over the past three decades.3 In particular, it’s worth noting the average outperformance of midcaps following seven rate-cut periods since the mid 1990s as shown in the following chart.

Exhibit 1: Equity Total Returns Following First Fed Rate Cuts

A rate-cutting cycle tends to foster a stimulative environment since smaller firms tend to borrow more than larger companies. With rate cuts setting the stage for lowered debt servicing costs, we believe this could serve as a catalyst for improved mid-cap earnings, and generally view this as an opportunity for investors to plug gaps in allocation exposure given the potential for a mid-cap comeback.

For some perspective on the valuation opportunity, midcaps in late October were trading at 20.6x, a relative discount to large-cap stocks, which have been trading higher (at 24.6 times earnings) than their 20-year average (of 19.4x).

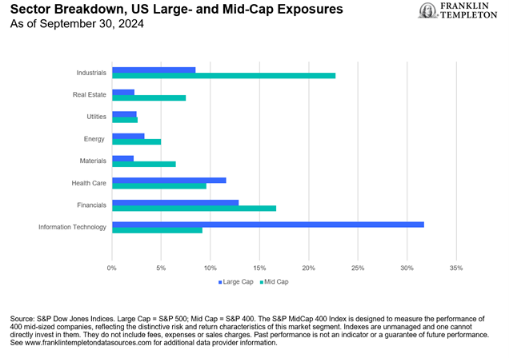

Another attractive characteristic is the relative sector diversification of midcaps to large caps. Given ongoing artificial intelligence (AI) concentration concerns, it’s worth noting that at the end of September, technology holdings comprised more than 31% of the S&P 500 Index and more than 34% of the large-cap focused Russell 1000 Index compared to just about 9% of the S&P 400 Index and 12% in the Russell MidCap Index.

And while utility companies were the best performers (+29% total returns year-to-date through October 14, 2024) for the mid-cap index, they held the lowest weighting within large-cap benchmarks. Industrials and materials sectors, which are underrepresented in the large-cap universe, may also be poised for expansion considering recent US stimulus bills aimed at building-out US manufacturing capabilities.

This is not to say AI-related firms may not still see impressive growth, but the pace of growth may decelerate and open the door for other segments of the market to shine, as smaller firms become less hampered by debt.

Exhibit 2: MidCaps Sector

Breakdown

Boosted in part by soft landing hopes, midcaps have been enjoying improved earnings guidance and we’ve seen several companies on a positive growth trajectory. According to FTSE Russell, more than two dozen constituents rose through the ranks from the Russell 2000 to join the Russell MidCap Index during this year’s portfolio reconstitution, with the highest number and weight of graduates coming from the technology industry.

To end on an optimistic note and quote from Fed President Daly: “A durable and sustained expansion allows everyone to thrive, and history tells us it is possible.”