Nyheter

A Political Ploy or A Strategic Reserve Asset

• Bitcoin: A Political Ploy or a Strategic Reserve Asset?

• Surviving Bitcoin’s Headwinds Amid Improving Macroeconomics

• The Approval of Ethereum ETFs and its Impact

• The Spotlight on DeFi: A Transformative Era

Surviving Bitcoin’s Headwinds Amid Improving Macroeconomics

The macroeconomic results that came out in July indicate improvements, still not enough to cut rates in the U.S., but there may be more than meets the eye. Increasing at an annual rate of 2.8% in the second quarter, the Gross Domestic Product (GDP) significantly exceeded expectations. With interest rates reaching the highest since the dot-com bubble, net interest payment is projected to reach the highest level as a percentage of GDP in over two decades. While the Fed’s collective sentiment over rate cuts is still uncertain, easing pressure on debt repayment could become increasingly important during the election season.

On the other hand, Wall Street had the worst month since October 2022. Disappointing second-quarter earnings from tech companies wiped out ~$985B off Nasdaq’s market cap on July 24. The stock market picked up on July 26 after a positive indicator boosted optimism about inflation. In line with expectations, the Federal Reserve’s favorite gauge of inflation, Personal Consumption Expenditures (PCE), rose by 2.5% from a year ago, 0.1% from last month. The PCE reading sparked optimism that the Fed might start cutting rates in September as the market predicted, which would bode well for Bitcoin and the longer tail of cryptoassets since lower borrowing costs will encourage bigger risk-on appetite. Some are even hoping Fed officials would hint at the prospect in the upcoming meeting on July 31.

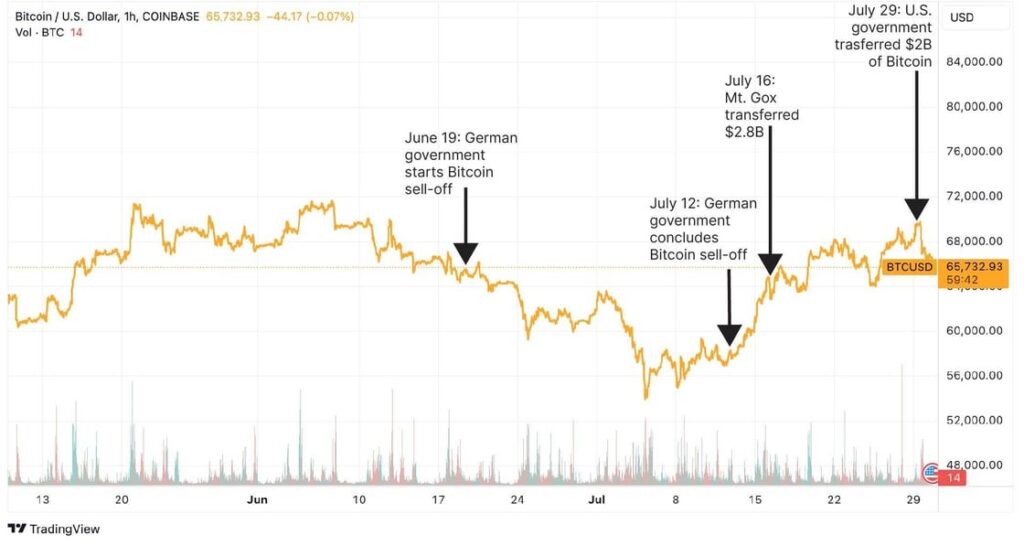

Figure 1 – Bitcoin’s Price Movement Against Headwinds

Source: 21Shares

Enjoying some political attention, Bitcoin held strong amid the tech dip, but it still had other headwinds to worry about.

• Between June 19 and July 12, the German government sold $2.88B worth of Bitcoin, seized from movie piracy website, Movie2k, earlier this year. Bitcoin fell by 10.7% over that period.

• In preparation for the repayment plan that began in July, Mt. Gox transferred $2.8B on July 16 from its cold wallet to a deposit address tied to Bitstamp, one of the five exchanges that have 60 days to distribute the tokens to Mt. Gox’s creditors. Bitcoin fell by just 1.6% on that day. Mt. Gox currently has $5.35B left in its holdings and originally $9B in total to return to creditors.

• On July 29, the U.S. government transferred $2B worth of confiscated Bitcoin to an unidentified wallet, pulling the price from $69.9K to as low as $66.6K in a few hours.

Finally, after months of negotiation, the Commodity Futures Trading Commission (CFTC) and FTX agreed that the latter would pay up to $12.7B to its creditors, pending judge approval. However, creditors have opposed this plan, arguing that FTX should pay them in-kind rather than dollar terms. A hearing on the settlement motion is scheduled for August 6, and a vote on the plan is due on August 16. Bitcoin and Solana are at the forefront of the potential market impact, with FTX previously announcing they have around 50 million SOL tokens and over 20K BTC. However, there are some silver linings. First, the crypto industry will finally turn the page on a dark chapter of its history. Last but not least, Bitcoin is a strategic subject matter used by some of the most powerful leaders in the world; excitement around it could balance out the repercussions of FTX’s repayment plan in the coming months.

In conclusion, slow macroeconomic improvements coupled with the urgency of the looming debt crisis in the U.S. are painting a picture of easing market conditions through the summer. Nevertheless, the crypto industry must weather the headwinds mentioned above, which investors should consider.

Bitcoin: A Political Ploy or a Strategic Reserve Asset?

On July 26, a range of Democrats sent a letter to the Democratic National Committee, urging them to pivot their adversary stance against crypto, citing that “crypto is at the top of voters’ minds in swing states.” They were probably spooked by Donald Trump’s progression towards crypto since the start of his presidential campaign. Arguably the most anticipated event this quarter was the Bitcoin conference in Nashville, with this year’s iteration seasoned by the presidential elections. The main (if not the only) reason for the excitement, marked by the crypto derivatives market as explained in our previous newsletter, was Trump’s speech on July 27.

If elected as president on November 5, Trump cautiously revealed he’ll do as follows:

• Establish a crypto presidential advisory council and create a national “stockpile” of Bitcoin.

• Keep 100% of the government’s confiscated Bitcoin holdings intact.

• Adopt stablecoins, viewed as pro-dollar, and establish a regulatory framework.

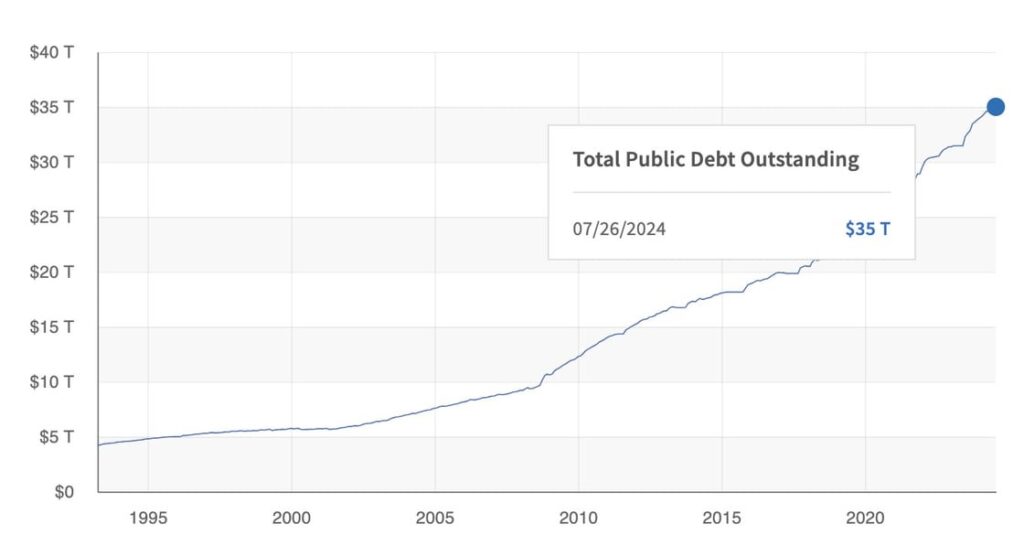

Similarly, Republican Senator Cynthia Lummis has been working on legislation requiring the Federal Reserve to hold Bitcoin as a strategic reserve asset, alongside gold and other foreign currencies, to manage the government’s monetary system. She proposes that the U.S. buys 1M BTC over the course of five years and hold it for 20 years to reduce national debt, which has soared to record highs, as shown in Figure 2. The idea also excited lawmakers elsewhere. On July 28, Johnny Ng, a Hong Kong Legislative Council member, announced that he’d be lobbying for and exploring the feasibility of including Bitcoin in financial reserves with different stakeholders in Hong Kong.

Figure 2 – U.S. National Debt Soars to $35 Trillion

Source: U.S. Treasury

It is important to remember that politically induced vows (especially during elections) are more often than not just talk. Many have deemed the prospect of Bitcoin as a reserve asset in the Treasury’s balance sheets as politically unrealistic, although feasible and fitting Bitcoin’s fundamentals. Surely, the paradigm shift in sentiment from “scam” to strategic reserve asset has enticed institutions to accumulate more Bitcoin in July:

• Boasting $150M in total net assets, Cantor Fitzgerald’s CEO confirmed the company holds undisclosed amounts of Bitcoin and is launching a $2B BTC financing business, which they’ll increase by $2B increments.

• On July 26, the State of Michigan Retirement System added $6.6M in Bitcoin ETFs to its pension fund assets, which now total $143.9M.

• On July 25, the Jersey City mayor announced they’re updating paperwork to allocate a percentage of the fund to Bitcoin ETFs. In May, the Wisconsin Pension Fund allocated 2%.

In summary, even if the announcements made at the Bitcoin conference do not come to fruition, the fact that crypto’s use case is emerging in aiding a major economy like the U.S. is a significant boost for adoption. However, retail interest is still estimated to be only 25% of what it was in May 2021. As the discussion continues and more politicians get involved from both sides of the aisle, the market is poised to witness unprecedented levels of mainstream adoption.

The Approval of Ethereum ETFs and their Impact

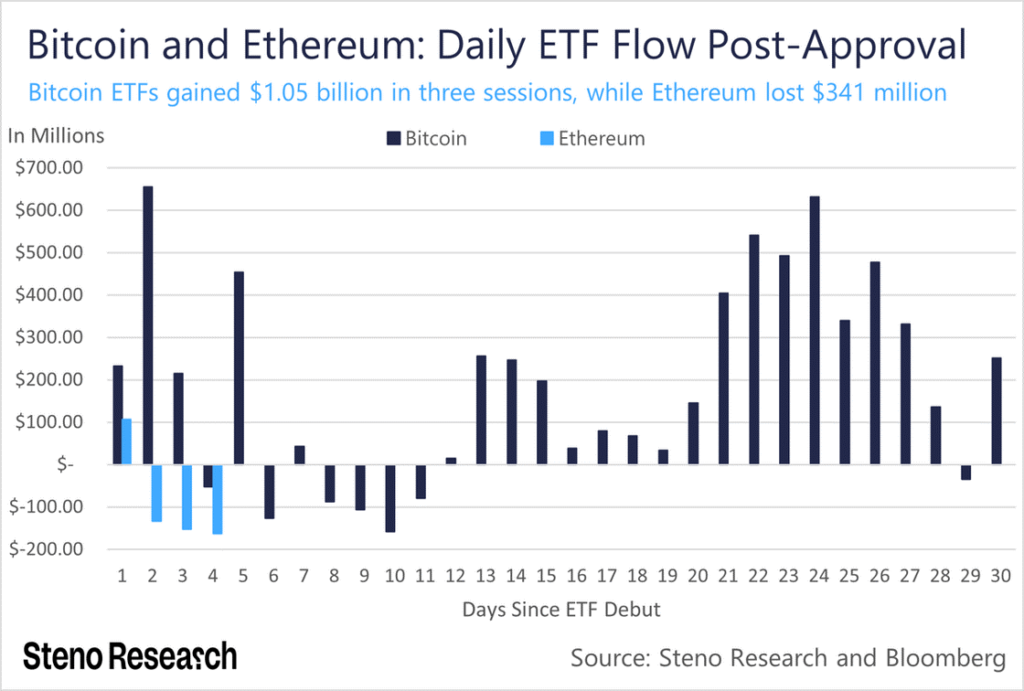

The first week of trading for Ethereum ETFs has largely met the expectations outlined in our last newsletter. The nine ETFs have generated $4.5B in total volume, approximately 15-20% of Bitcoin ETFs’ first-week volume. However, Ethereum ETFs experienced a net outflow of ~$300M, compared to Bitcoin ETFs’ $1.5B inflow during their debut week, as seen below in Figure 3.

Figure 3: Comparing BTC & ETH US Spot Net Flows

Source: Steno Research

Nevertheless, we expect that ETH will demonstrate heightened price sensitivity in the coming months. This is largely because 45% of ETH’s total supply is either locked away in staking or smart contracts or is lost. Further, ETH’s liquid supply on exchanges is lower than that of Bitcoin, with only 10% of ETH available compared to 12% for Bitcoin. Unlike Bitcoin, Ethereum does not experience significant selling pressure from miners, who typically sell an average of $5M-10M of their holdings daily to cover operational costs. Consequently, ETH is likely to react more sharply to market demand due to its limited liquidity and the lack of consistent miner offloading.

As a reminder, Ethereum and Bitcoin ETFs are complementary rather than competitive products in a portfolio, each representing distinct market segments. Bitcoin is primarily viewed as digital gold due to its scarcity and immutable monetary policy, positioning it as a potential hedge against economic instability. Further, while Bitcoin is also growing into a software-as-a-service platform, this transition is yet to fully materialize. In contrast, Ethereum serves multiple purposes, functioning as a global app store, a financial settlement layer, and a tokenization hub. While Bitcoin addresses financial system concerns, Ethereum aims to enhance the internet infrastructure and underpin the digital economy.

This differentiation suggests that both ETFs can coexist, catering to diverse investor needs and market demands. With this in mind, the approval of ETH lends legitimacy to the foundational infrastructure supporting the Web 3 ecosystem. Thus, we anticipate this recognition will cascade to a broader range of assets, with decentralized finance (DeFi) protocols likely emerging as prime beneficiaries of this increased attention.

The Spotlight on DeFi: A Transformative Era

DeFi has been having its shining moment, which is evident in the record-breaking performance of decentralized exchanges (DEXs). For the first time, DEX spot trading volume reached 14% of centralized exchange volume, marking an all-time high in the ratio between the two types of platforms. This growth is symbolic of migration towards non-custodial infrastructure that’s been in motion for the last two years, driven by users’ growing trust in crypto’s railways.

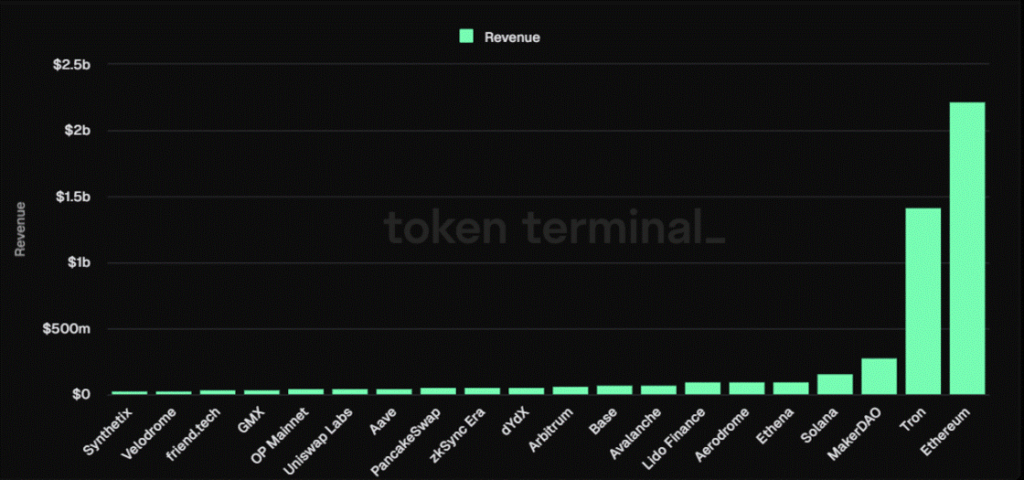

With the approval of Ethereum ETFs, we foresee a growing emphasis on consumer-facing applications within the industry. We also predict that fundamental valuation will become more significant as the industry gains credibility, favoring businesses with strong fundamentals. In this context, four of the top 15 revenue-generating Web 3 protocols are well-established DeFi platforms like Aave, MakerDAO, Lido, and Uniswap, as observed below in Figure 4. This highlights the market suitability of well-designed DeFi protocols, even as the industry evolves and attracts new participants. With this context, let’s discuss the forthcoming protocol upgrades that we believe will elevate their prominence amidst the changing landscape.

Figure 4: Revenue Performance Ranking of the Top 20 Protocols over the Last Year

Source: TokenTerminal

First is Aave. The leading decentralized lending protocol by Total Value Locked and the sixth-largest revenue-generating DeFi application is gauging community sentiment on implementing a fee switch. This proposal, spearheaded by Aave’s founder, aims to distribute the protocol’s excess revenue to token holders. Additionally, it suggests using part of the excess revenue to buy back AAVE on the secondary market, thereby ensuring consistent demand for the token. This new tokenomics model would allow stakers to earn AAVE sustainably, avoiding the drawbacks of an inflationary issuance mechanism.

That said, Aave’s temperature check should conclude by next week, followed by a snapshot vote. Thus, it’ll likely take a few weeks to fully implement the mechanism if the community approves the proposal. Worth mentioning that Aave’s proposal takes a cue from a previous initiative by Uniswap, which sought to allocate trading fees to token stakers but postponed the governance vote in June. That said, we believe the recent regulatory clarity regarding Ethereum could reignite the momentum needed for more DeFi applications to incorporate security-like features into their frameworks. Thus, this could transform their respective tokens into capital-generating assets, rendering them attractive.

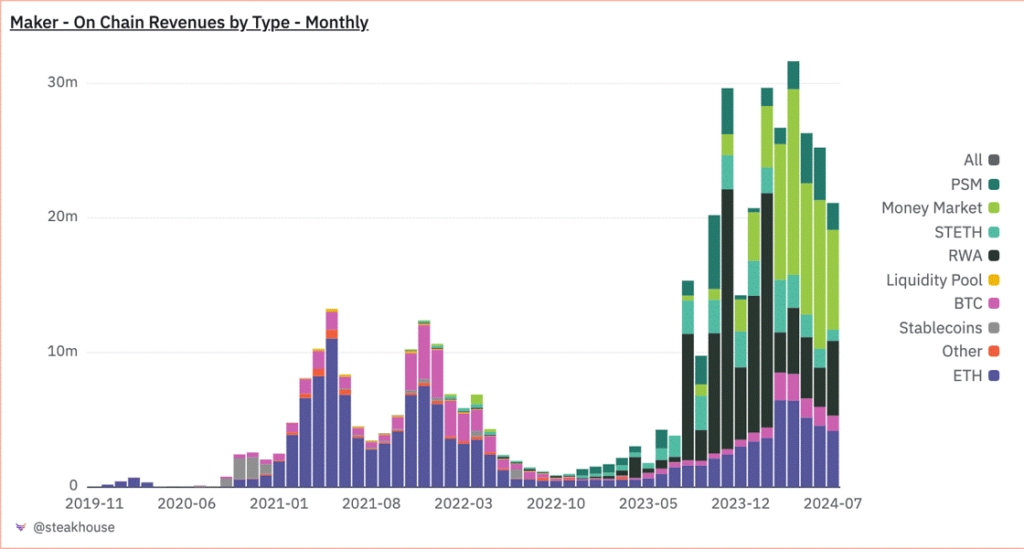

On a different note, MakerDAO referred to as Ethereum’s global reserve bank and the issuer of DAI, is fully embracing the tokenization trend. The protocol already generates more than half of its revenue from tokenized products, which include private credit and US treasury yields, as shown in Figure 5. This positions MakerDAO at the forefront of crypto protocols integrating with traditional finance. Now, MakerDAO plans to invest an additional billion dollars into tokenized treasuries. This move has prompted sector leaders like Blackrock’s Securitize BUIDL fund, Ondo Finance, and Superstate to apply for the Grand Prix competition, which begins in the second week of August. Once implemented, this initiative is expected to boost the total government securities AUM by 55%, expanding the market size to $3B. This would represent a 30-fold increase since April 2023.

Figure 5: MakerDAO’s Revenue by Type

Source: SteakHouse on Dune

This development solidifies MakerDAO’s position as a pivotal player in the tokenization landscape, while providing a robust proxy investment into crypto’s application layer. Its strength is underscored by the fact that Maker accounts for nearly 40% of Ethereum’s total DeFi profits, making it the third-largest revenue-generating protocol in the industry, as echoed above in Figure 4.

To recap, we believe the approval of Ethereum ETFs is poised to legitimize the market, boost investor confidence, and accelerate the adoption of Ethereum-based applications. As a result, established protocols with proven track records of resilience and revenue generation will likely attract significant investor attention in the coming months.

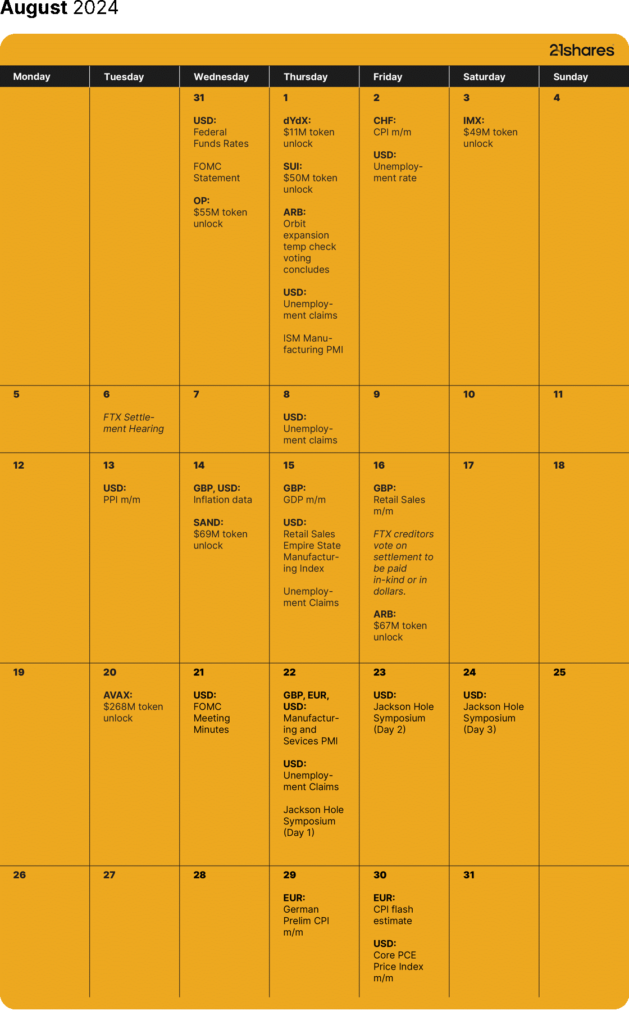

Next Month’s Calendar

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

During and after the US market close on Friday, cryptocurrency markets experienced their largest liquidation event on record, with an estimated $19 billion in leveraged positions unwound across futures and perpetual swap markets.

We expect Solana to reach beyond $330. Here’s why

Solana’s growth is underpinned by real fundamentals – measurable cash flows, rising user activity, and expanding economic metrics that rival multibillion dollar growth-tech companies. As Solana transitions from a speculative narrative to a revenue-generating powerhouse, traditional valuation tools like discounted cash flow (DCF) models are becoming increasingly relevant in assessing its long-term potential.

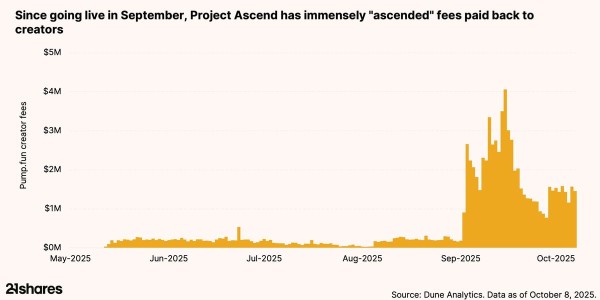

Tokenized attention: Pump.fun and the rise of Creator Capital Markets

The internet’s most valuable commodity is attention – and in 2025, that attention is becoming tokenized. Few projects embody this transformation more vividly than Pump.fun, a Solana-based platform that began as a meme-coin launchpad and has rapidly evolved beyond that use case. Launching Project Ascend in September, Pump.fun introduced Creator Capital Markets (CCM) – a suite of tools that lets streamers and influencers tokenize their audiences.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

JEYH ETF är högavkastande obligationer hedgade i euro

Record crypto liquidations amid tariff shock

VALOUR VIRTUAL SEK följer priset på VIRTUAL, Virtuals Protocols egna token

Crypto market update: record liquidations amid tariff shock

Hur investera i Blockchain med hjälp av börshandlade fonder

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

IN0A ETF spårar S&P 500 med fokus på företag med höga ESG-betyg

YSLV ETP ställer ut köpoptioner på silver för att skapa en löpande avkastning

De bästa lågvolatilitets ETFer på marknaden

PLTY ETP utfärdar optioner mot aktier i Palantir

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanIN0A ETF spårar S&P 500 med fokus på företag med höga ESG-betyg

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanYSLV ETP ställer ut köpoptioner på silver för att skapa en löpande avkastning

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanPLTY ETP utfärdar optioner mot aktier i Palantir

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanTime in Bitcoin beats timing Bitcoin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanInvestera i NEAR med en börshandlad produkt

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf kommenterar kopparuppgången